- India

- /

- Construction

- /

- NSEI:ENGINERSIN

Engineers India Limited's (NSE:ENGINERSIN) Share Price Boosted 30% But Its Business Prospects Need A Lift Too

Despite an already strong run, Engineers India Limited (NSE:ENGINERSIN) shares have been powering on, with a gain of 30% in the last thirty days. The annual gain comes to 146% following the latest surge, making investors sit up and take notice.

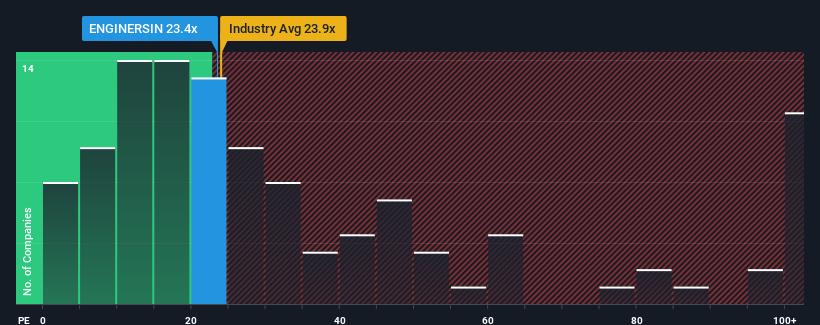

Even after such a large jump in price, given about half the companies in India have price-to-earnings ratios (or "P/E's") above 30x, you may still consider Engineers India as an attractive investment with its 23.4x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

Engineers India certainly has been doing a good job lately as it's been growing earnings more than most other companies. One possibility is that the P/E is low because investors think this strong earnings performance might be less impressive moving forward. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

See our latest analysis for Engineers India

Is There Any Growth For Engineers India?

In order to justify its P/E ratio, Engineers India would need to produce sluggish growth that's trailing the market.

Retrospectively, the last year delivered an exceptional 82% gain to the company's bottom line. The strong recent performance means it was also able to grow EPS by 45% in total over the last three years. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Looking ahead now, EPS is anticipated to slump, contracting by 3.3% each year during the coming three years according to the two analysts following the company. With the market predicted to deliver 19% growth per annum, that's a disappointing outcome.

In light of this, it's understandable that Engineers India's P/E would sit below the majority of other companies. However, shrinking earnings are unlikely to lead to a stable P/E over the longer term. There's potential for the P/E to fall to even lower levels if the company doesn't improve its profitability.

What We Can Learn From Engineers India's P/E?

Despite Engineers India's shares building up a head of steam, its P/E still lags most other companies. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that Engineers India maintains its low P/E on the weakness of its forecast for sliding earnings, as expected. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. It's hard to see the share price rising strongly in the near future under these circumstances.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 2 warning signs with Engineers India (at least 1 which doesn't sit too well with us), and understanding these should be part of your investment process.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Valuation is complex, but we're here to simplify it.

Discover if Engineers India might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:ENGINERSIN

Engineers India

An engineering consultancy company, provides design, engineering, procurement, construction, and integrated project management services for oil, gas, fertilizers, steel, railways, power, infrastructure, and petrochemical industries worldwide.

Flawless balance sheet with moderate growth potential.

Similar Companies

Market Insights

Community Narratives