David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Elecon Engineering Company Limited (NSE:ELECON) does have debt on its balance sheet. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Elecon Engineering

How Much Debt Does Elecon Engineering Carry?

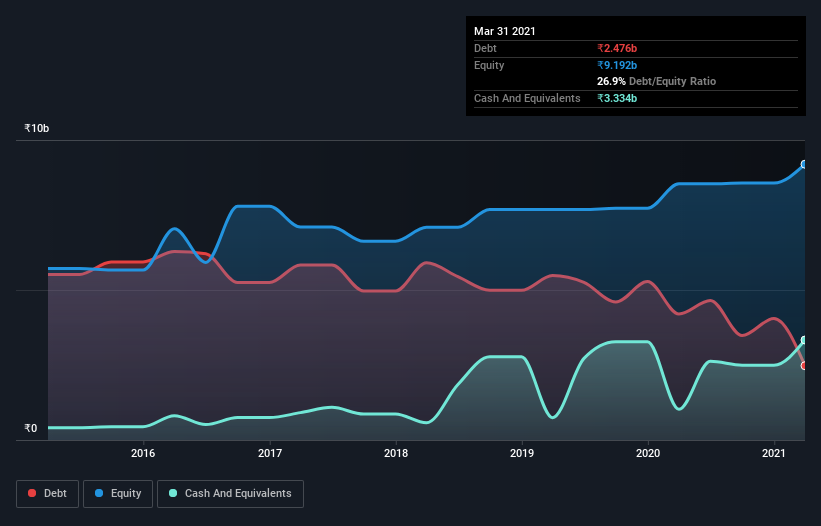

As you can see below, Elecon Engineering had ₹2.48b of debt at March 2021, down from ₹4.20b a year prior. However, its balance sheet shows it holds ₹3.33b in cash, so it actually has ₹857.8m net cash.

How Strong Is Elecon Engineering's Balance Sheet?

We can see from the most recent balance sheet that Elecon Engineering had liabilities of ₹8.39b falling due within a year, and liabilities of ₹2.35b due beyond that. On the other hand, it had cash of ₹3.33b and ₹5.50b worth of receivables due within a year. So it has liabilities totalling ₹1.90b more than its cash and near-term receivables, combined.

Given Elecon Engineering has a market capitalization of ₹14.0b, it's hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. Despite its noteworthy liabilities, Elecon Engineering boasts net cash, so it's fair to say it does not have a heavy debt load!

Importantly, Elecon Engineering grew its EBIT by 46% over the last twelve months, and that growth will make it easier to handle its debt. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Elecon Engineering will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. Elecon Engineering may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the last three years, Elecon Engineering actually produced more free cash flow than EBIT. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Summing up

While Elecon Engineering does have more liabilities than liquid assets, it also has net cash of ₹857.8m. The cherry on top was that in converted 155% of that EBIT to free cash flow, bringing in ₹2.4b. So we don't think Elecon Engineering's use of debt is risky. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Be aware that Elecon Engineering is showing 2 warning signs in our investment analysis , you should know about...

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you decide to trade Elecon Engineering, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Elecon Engineering might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:ELECON

Elecon Engineering

Manufactures and sells power transmission and material handling equipment in India and internationally.

Flawless balance sheet with proven track record.