Cummins India Limited's (NSE:CUMMINSIND) 27% Price Boost Is Out Of Tune With Earnings

Despite an already strong run, Cummins India Limited (NSE:CUMMINSIND) shares have been powering on, with a gain of 27% in the last thirty days. The annual gain comes to 132% following the latest surge, making investors sit up and take notice.

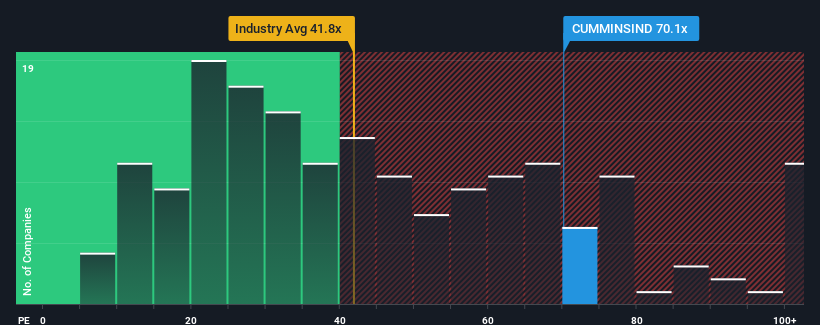

After such a large jump in price, given close to half the companies in India have price-to-earnings ratios (or "P/E's") below 31x, you may consider Cummins India as a stock to avoid entirely with its 70.1x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so lofty.

Cummins India certainly has been doing a good job lately as it's been growing earnings more than most other companies. It seems that many are expecting the strong earnings performance to persist, which has raised the P/E. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

See our latest analysis for Cummins India

What Are Growth Metrics Telling Us About The High P/E?

In order to justify its P/E ratio, Cummins India would need to produce outstanding growth well in excess of the market.

Retrospectively, the last year delivered an exceptional 40% gain to the company's bottom line. The latest three year period has also seen an excellent 140% overall rise in EPS, aided by its short-term performance. So we can start by confirming that the company has done a great job of growing earnings over that time.

Looking ahead now, EPS is anticipated to climb by 7.8% each year during the coming three years according to the analysts following the company. With the market predicted to deliver 21% growth each year, the company is positioned for a weaker earnings result.

In light of this, it's alarming that Cummins India's P/E sits above the majority of other companies. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. Only the boldest would assume these prices are sustainable as this level of earnings growth is likely to weigh heavily on the share price eventually.

The Key Takeaway

Shares in Cummins India have built up some good momentum lately, which has really inflated its P/E. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

Our examination of Cummins India's analyst forecasts revealed that its inferior earnings outlook isn't impacting its high P/E anywhere near as much as we would have predicted. Right now we are increasingly uncomfortable with the high P/E as the predicted future earnings aren't likely to support such positive sentiment for long. This places shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

Don't forget that there may be other risks. For instance, we've identified 1 warning sign for Cummins India that you should be aware of.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a low P/E.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:CUMMINSIND

Cummins India

Engages in the design, manufacture, distribution, and service of engines, generator sets, and related technologies in India, Nepal, and Bhutan.

Outstanding track record with flawless balance sheet and pays a dividend.

Market Insights

Community Narratives