Advertisement

- India

- /

- Electrical

- /

- NSEI:BHEL

Even though Bharat Heavy Electricals (NSE:BHEL) has lost ₹65b market cap in last 7 days, shareholders are still up 463% over 3 years

Investing can be hard but the potential fo an individual stock to pay off big time inspires us. Not every pick can be a winner, but when you pick the right stock, you can win big. Take, for example, the Bharat Heavy Electricals Limited (NSE:BHEL) share price, which skyrocketed 457% over three years. On top of that, the share price is up 59% in about a quarter.

In light of the stock dropping 7.9% in the past week, we want to investigate the longer term story, and see if fundamentals have been the driver of the company's positive three-year return.

Check out our latest analysis for Bharat Heavy Electricals

While Bharat Heavy Electricals made a small profit, in the last year, we think that the market is probably more focussed on the top line growth at the moment. As a general rule, we think this kind of company is more comparable to loss-making stocks, since the actual profit is so low. For shareholders to have confidence a company will grow profits significantly, it must grow revenue.

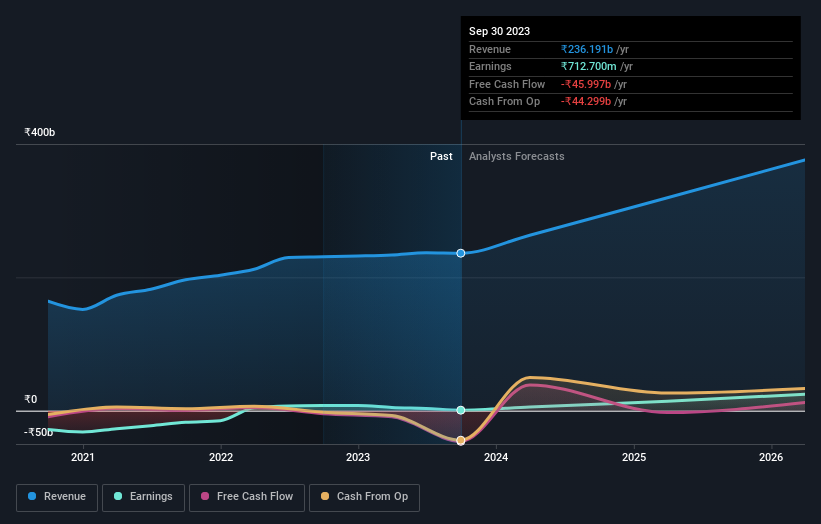

Bharat Heavy Electricals' revenue trended up 14% each year over three years. That's pretty nice growth. Arguably the very strong share price gain of 77% a year is very generous when compared to the revenue growth. After a price rise like that many will have the business, and plenty of them will be wondering whether the price moved too high, too fast.

The company's revenue and earnings (over time) are depicted in the image below (click to see the exact numbers).

Bharat Heavy Electricals is well known by investors, and plenty of clever analysts have tried to predict the future profit levels. You can see what analysts are predicting for Bharat Heavy Electricals in this interactive graph of future profit estimates.

What About Dividends?

As well as measuring the share price return, investors should also consider the total shareholder return (TSR). The TSR incorporates the value of any spin-offs or discounted capital raisings, along with any dividends, based on the assumption that the dividends are reinvested. It's fair to say that the TSR gives a more complete picture for stocks that pay a dividend. As it happens, Bharat Heavy Electricals' TSR for the last 3 years was 463%, which exceeds the share price return mentioned earlier. The dividends paid by the company have thusly boosted the total shareholder return.

A Different Perspective

It's nice to see that Bharat Heavy Electricals shareholders have received a total shareholder return of 204% over the last year. Of course, that includes the dividend. That gain is better than the annual TSR over five years, which is 30%. Therefore it seems like sentiment around the company has been positive lately. In the best case scenario, this may hint at some real business momentum, implying that now could be a great time to delve deeper. It's always interesting to track share price performance over the longer term. But to understand Bharat Heavy Electricals better, we need to consider many other factors. For instance, we've identified 2 warning signs for Bharat Heavy Electricals that you should be aware of.

We will like Bharat Heavy Electricals better if we see some big insider buys. While we wait, check out this free list of growing companies with considerable, recent, insider buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Indian exchanges.

Valuation is complex, but we're here to simplify it.

Discover if Bharat Heavy Electricals might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:BHEL

Bharat Heavy Electricals

Operates as engineering and manufacturing company in India and internationally.

High growth potential with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.6% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|28.3% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|87.8% undervalued

AG

Community Contributor