Advertisement

IDBI Bank (NSE:IDBI) Is Paying Out A Larger Dividend Than Last Year

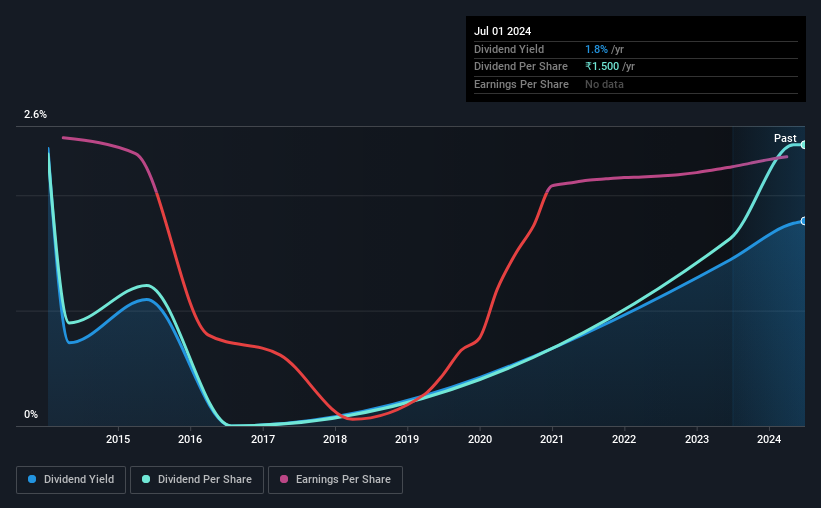

IDBI Bank Limited (NSE:IDBI) has announced that it will be increasing its dividend from last year's comparable payment on the 22nd of August to ₹1.50. This makes the dividend yield 1.8%, which is above the industry average.

See our latest analysis for IDBI Bank

IDBI Bank's Payment Expected To Have Solid Earnings Coverage

A big dividend yield for a few years doesn't mean much if it can't be sustained.

IDBI Bank has a long history of paying out dividends, with its current track record at a minimum of 10 years. Past distributions do not necessarily guarantee future ones, but IDBI Bank's payout ratio of 28% is a good sign as this means that earnings decently cover dividends.

If the trend of the last few years continues, EPS will grow by 79.3% over the next 12 months. If the dividend continues along recent trends, we estimate the future payout ratio will be 16%, which is in the range that makes us comfortable with the sustainability of the dividend.

Dividend Volatility

Although the company has a long dividend history, it has been cut at least once in the last 10 years. Since 2014, the dividend has gone from ₹1.45 total annually to ₹1.50. Its dividends have grown at less than 1% per annum over this time frame. The dividend has seen some fluctuations in the past, so even though the dividend was raised this year, we should remember that it has been cut in the past.

The Dividend Looks Likely To Grow

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. IDBI Bank has seen EPS rising for the last five years, at 79% per annum. Rapid earnings growth and a low payout ratio suggest this company has been effectively reinvesting in its business. Should that continue, this company could have a bright future.

IDBI Bank Looks Like A Great Dividend Stock

Overall, a dividend increase is always good, and we think that IDBI Bank is a strong income stock thanks to its track record and growing earnings. The company is easily earning enough to cover its dividend payments and it is great to see that these earnings are being translated into cash flow. All in all, this checks a lot of the boxes we look for when choosing an income stock.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. However, there are other things to consider for investors when analysing stock performance. As an example, we've identified 1 warning sign for IDBI Bank that you should be aware of before investing. Is IDBI Bank not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NSEI:IDBI

Adequate balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.2% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.1% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|12.7% undervalued

MA

Community Contributor