- India

- /

- Auto Components

- /

- NSEI:RANEHOLDIN

Rane Holdings' (NSE:RANEHOLDIN) Shareholders Will Receive A Bigger Dividend Than Last Year

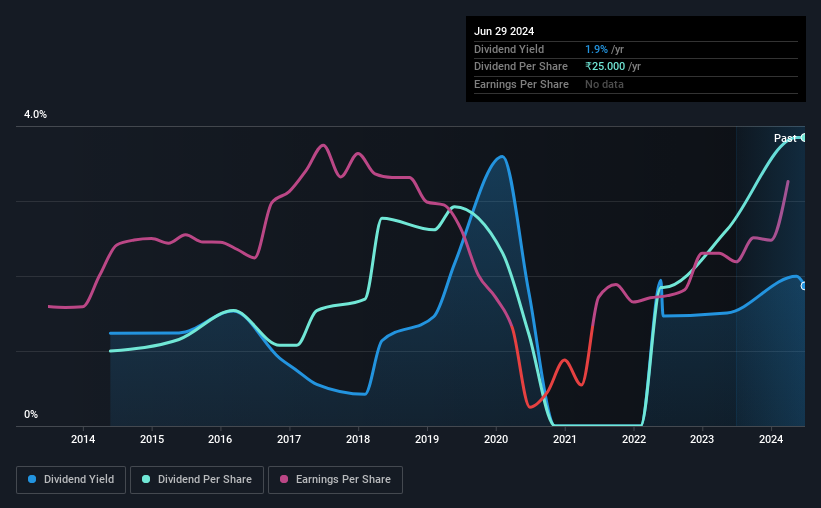

Rane Holdings Limited (NSE:RANEHOLDIN) will increase its dividend from last year's comparable payment on the 12th of August to ₹25.00. This will take the dividend yield to an attractive 1.9%, providing a nice boost to shareholder returns.

Check out our latest analysis for Rane Holdings

Rane Holdings' Earnings Easily Cover The Distributions

While it is great to have a strong dividend yield, we should also consider whether the payment is sustainable. Based on the last payment, Rane Holdings was paying only paying out a fraction of earnings, but the payment was a massive 147% of cash flows. While the business may be attempting to set a balanced dividend policy, a cash payout ratio this high might expose the dividend to being cut if the business ran into some challenges.

If the trend of the last few years continues, EPS will grow by 3.6% over the next 12 months. Assuming the dividend continues along recent trends, we think the payout ratio could be 31% by next year, which is in a pretty sustainable range.

Dividend Volatility

The company's dividend history has been marked by instability, with at least one cut in the last 10 years. Since 2014, the dividend has gone from ₹6.50 total annually to ₹25.00. This implies that the company grew its distributions at a yearly rate of about 14% over that duration. Rane Holdings has grown distributions at a rapid rate despite cutting the dividend at least once in the past. Companies that cut once often cut again, so we would be cautious about buying this stock solely for the dividend income.

Dividend Growth May Be Hard To Achieve

With a relatively unstable dividend, it's even more important to see if earnings per share is growing. Earnings per share has been crawling upwards at 3.6% per year. While EPS growth is quite low, Rane Holdings has the option to increase the payout ratio to return more cash to shareholders.

In Summary

In summary, while it's always good to see the dividend being raised, we don't think Rane Holdings' payments are rock solid. While Rane Holdings is earning enough to cover the payments, the cash flows are lacking. We would be a touch cautious of relying on this stock primarily for the dividend income.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. However, there are other things to consider for investors when analysing stock performance. To that end, Rane Holdings has 3 warning signs (and 1 which is potentially serious) we think you should know about. Is Rane Holdings not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NSEI:RANEHOLDIN

Rane Holdings

Manufactures and markets automotive components for the transportation industry in India and internationally.

Established dividend payer and good value.

Similar Companies

Market Insights

Community Narratives