The investors in JK Tyre & Industries Limited's (NSE:JKTYRE) will be rubbing their hands together with glee today, after the share price leapt 50% to ₹136 in the week following its third-quarter results. JK Tyre & Industries beat revenue forecasts by a solid 16% to hit ₹28b. Statutory earnings per share came in at ₹6.12, in line with expectations. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analysts have changed their mind on JK Tyre & Industries after the latest results.

View our latest analysis for JK Tyre & Industries

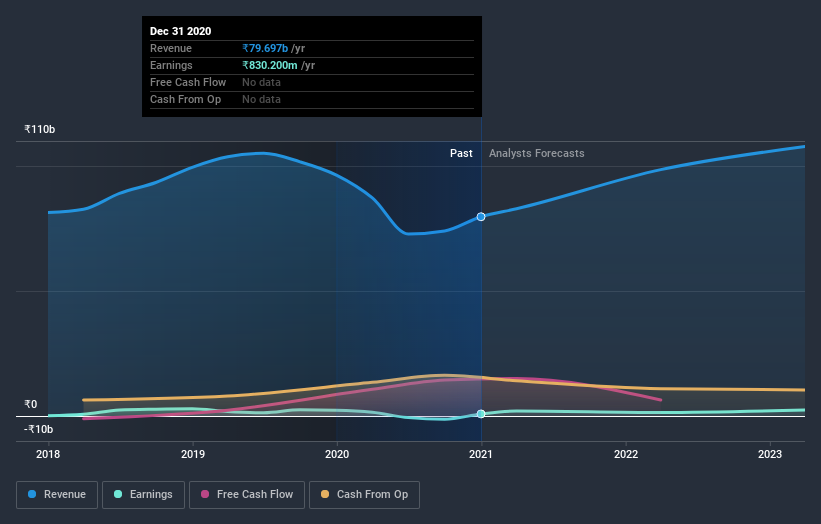

After the latest results, the dual analysts covering JK Tyre & Industries are now predicting revenues of ₹98.5b in 2022. If met, this would reflect a major 24% improvement in sales compared to the last 12 months. Statutory earnings per share are predicted to jump 122% to ₹7.50. Before this earnings report, the analysts had been forecasting revenues of ₹97.1b and earnings per share (EPS) of ₹10.15 in 2022. The analysts seem to have become more bearish following the latest results. While there were no changes to revenue forecasts, there was a large cut to EPS estimates.

The consensus price target held steady at ₹74.50, with the analysts seemingly voting that their lower forecast earnings are not expected to lead to a lower stock price in the foreseeable future.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the JK Tyre & Industries' past performance and to peers in the same industry. It's clear from the latest estimates that JK Tyre & Industries' rate of growth is expected to accelerate meaningfully, with the forecast 24% revenue growth noticeably faster than its historical growth of 4.8%p.a. over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 16% per year. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect JK Tyre & Industries to grow faster than the wider industry.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for JK Tyre & Industries. Happily, there were no major changes to revenue forecasts, with the business still expected to grow faster than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. We have analyst estimates for JK Tyre & Industries going out as far as 2023, and you can see them free on our platform here.

You still need to take note of risks, for example - JK Tyre & Industries has 4 warning signs (and 1 which shouldn't be ignored) we think you should know about.

If you decide to trade JK Tyre & Industries, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:JKTYRE

JK Tyre & Industries

Engages in the developing, manufacturing, marketing, and distribution of automotive tyres, tubes, flaps, and retreads in India, Mexico, and internationally.

Undervalued with proven track record and pays a dividend.