- India

- /

- Auto Components

- /

- NSEI:EXIDEIND

Why Exide Industries Limited (NSE:EXIDEIND) Is A Dividend Rockstar

Is Exide Industries Limited (NSE:EXIDEIND) a good dividend stock? How can we tell? Dividend paying companies with growing earnings can be highly rewarding in the long term. If you are hoping to live on your dividends, it's important to be more stringent with your investments than the average punter. Regular readers know we like to apply the same approach to each dividend stock, and we hope you'll find our analysis useful.

A slim 1.3% yield is hard to get excited about, but the long payment history is respectable. At the right price, or with strong growth opportunities, Exide Industries could have potential. Before you buy any stock for its dividend however, you should always remember Warren Buffett's two rules: 1) Don't lose money, and 2) Remember rule #1. We'll run through some checks below to help with this.

Explore this interactive chart for our latest analysis on Exide Industries!

Payout ratios

Companies (usually) pay dividends out of their earnings. If a company is paying more than it earns, the dividend might have to be cut. As a result, we should always investigate whether a company can afford its dividend, measured as a percentage of a company's net income after tax. Looking at the data, we can see that 24% of Exide Industries's profits were paid out as dividends in the last 12 months. With a low payout ratio, it looks like the dividend is comprehensively covered by earnings.

In addition to comparing dividends against profits, we should inspect whether the company generated enough cash to pay its dividend. Exide Industries's cash payout ratio last year was 14%. Cash flows are typically lumpy, but this looks like an appropriately conservative payout. It's positive to see that Exide Industries's dividend is covered by both profits and cash flow, since this is generally a sign that the dividend is sustainable, and a lower payout ratio usually suggests a greater margin of safety before the dividend gets cut.

With a strong net cash balance, Exide Industries investors may not have much to worry about in the near term from a dividend perspective.

Consider getting our latest analysis on Exide Industries's financial position here.

Dividend Volatility

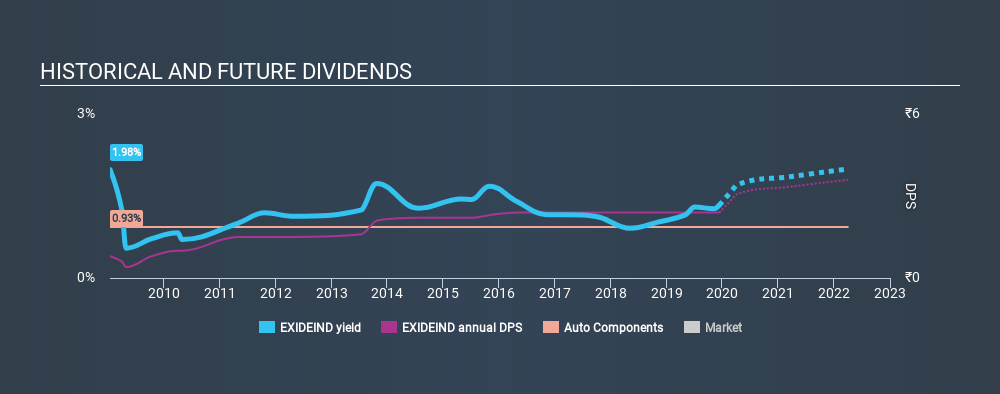

Before buying a stock for its income, we want to see if the dividends have been stable in the past, and if the company has a track record of maintaining its dividend. For the purpose of this article, we only scrutinise the last decade of Exide Industries's dividend payments. This dividend has been unstable, which we define as having fallen by at least 20% one or more times over this time. During the past ten-year period, the first annual payment was ₹0.80 in 2009, compared to ₹2.40 last year. This works out to be a compound annual growth rate (CAGR) of approximately 12% a year over that time. The growth in dividends has not been linear, but the CAGR is a decent approximation of the rate of change over this time frame.

It's not great to see that the payment has been cut in the past. We're generally more wary of companies that have cut their dividend before, as they tend to perform worse in an economic downturn.

Dividend Growth Potential

With a relatively unstable dividend, it's even more important to evaluate if earnings per share (EPS) are growing - it's not worth taking the risk on a dividend getting cut, unless you might be rewarded with larger dividends in future. Exide Industries has grown its earnings per share at 9.4% per annum over the past five years. With a decent amount of growth and a low payout ratio, we think this bodes well for Exide Industries's prospects of growing its dividend payments in the future.

Conclusion

When we look at a dividend stock, we need to form a judgement on whether the dividend will grow, if the company is able to maintain it in a wide range of economic circumstances, and if the dividend payout is sustainable. Firstly, we like that Exide Industries has low and conservative payout ratios. Next, earnings growth has been good, but unfortunately the dividend has been cut at least once in the past. Overall we think Exide Industries scores well on our analysis. It's not quite perfect, but we'd definitely be keen to take a closer look.

Companies that are growing earnings tend to be the best dividend stocks over the long term. See what the 23 analysts we track are forecasting for Exide Industries for free with public analyst estimates for the company.

Looking for more high-yielding dividend ideas? Try our curated list of dividend stocks with a yield above 3%.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NSEI:EXIDEIND

Exide Industries

Designs, manufactures, markets, and sells lead acid storage batteries in India and internationally.

Excellent balance sheet with limited growth.

Similar Companies

Market Insights

Community Narratives