Advertisement

- India

- /

- Auto Components

- /

- NSEI:BANCOINDIA

The recent ₹5.8b market cap decrease is likely to have disappointed insiders invested in Banco Products (India) Limited (NSE:BANCOINDIA)

Key Insights

- Banco Products (India)'s significant insider ownership suggests inherent interests in company's expansion

- Mehul Patel owns 56% of the company

- Past performance of a company along with ownership data serve to give a strong idea about prospects for a business

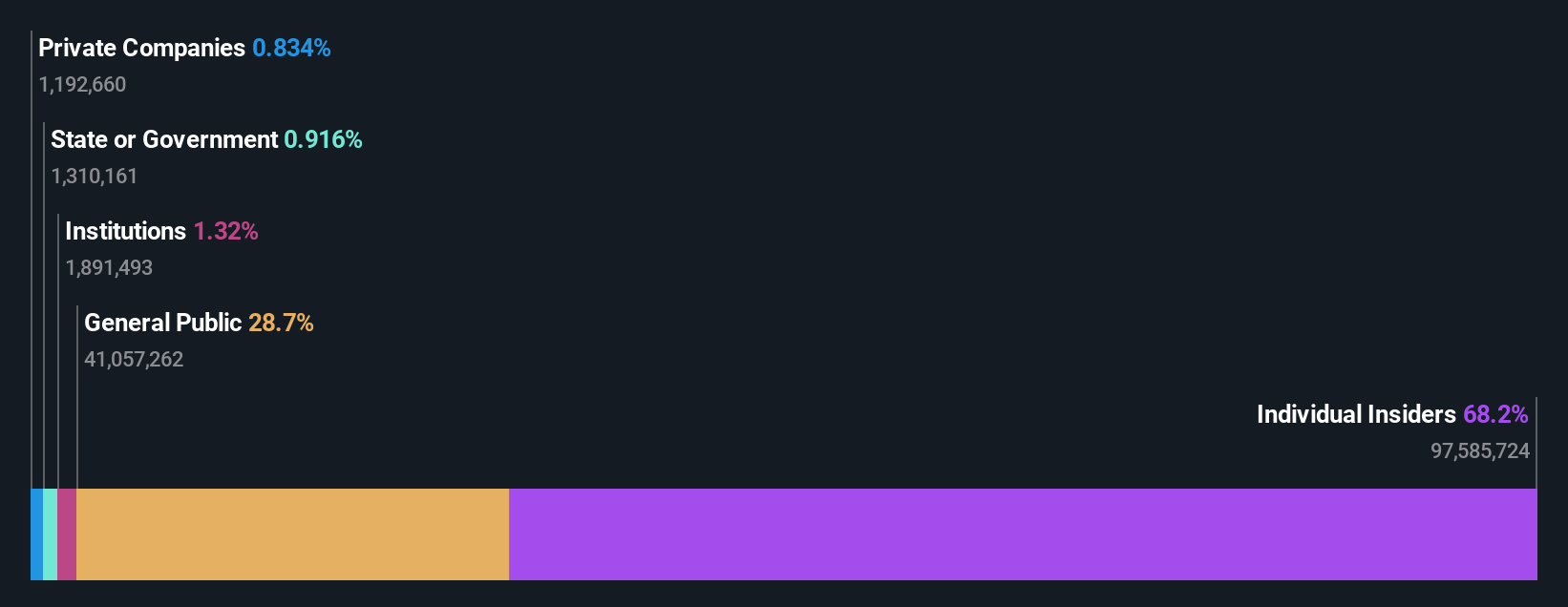

Every investor in Banco Products (India) Limited (NSE:BANCOINDIA) should be aware of the most powerful shareholder groups. The group holding the most number of shares in the company, around 68% to be precise, is individual insiders. In other words, the group stands to gain the most (or lose the most) from their investment into the company.

As a result, insiders as a group endured the highest losses after market cap fell by ₹5.8b.

Let's take a closer look to see what the different types of shareholders can tell us about Banco Products (India).

See our latest analysis for Banco Products (India)

What Does The Institutional Ownership Tell Us About Banco Products (India)?

Institutional investors commonly compare their own returns to the returns of a commonly followed index. So they generally do consider buying larger companies that are included in the relevant benchmark index.

Less than 5% of Banco Products (India) is held by institutional investors. This suggests that some funds have the company in their sights, but many have not yet bought shares in it. If the company is growing earnings, that may indicate that it is just beginning to catch the attention of these deep-pocketed investors. We sometimes see a rising share price when a few big institutions want to buy a certain stock at the same time. The history of earnings and revenue, which you can see below, could be helpful in considering if more institutional investors will want the stock. Of course, there are plenty of other factors to consider, too.

We note that hedge funds don't have a meaningful investment in Banco Products (India). Mehul Patel is currently the largest shareholder, with 56% of shares outstanding. This implies that they have majority interest control of the future of the company. Samir Patel is the second largest shareholder owning 7.0% of common stock, and Hasumati Patel holds about 2.1% of the company stock.

Researching institutional ownership is a good way to gauge and filter a stock's expected performance. The same can be achieved by studying analyst sentiments. Our information suggests that there isn't any analyst coverage of the stock, so it is probably little known.

Insider Ownership Of Banco Products (India)

The definition of an insider can differ slightly between different countries, but members of the board of directors always count. The company management answer to the board and the latter should represent the interests of shareholders. Notably, sometimes top-level managers are on the board themselves.

I generally consider insider ownership to be a good thing. However, on some occasions it makes it more difficult for other shareholders to hold the board accountable for decisions.

It seems that insiders own more than half the Banco Products (India) Limited stock. This gives them a lot of power. Insiders own ₹65b worth of shares in the ₹96b company. That's extraordinary! Most would be pleased to see the board is investing alongside them. You may wish to discover if they have been buying or selling.

General Public Ownership

The general public, who are usually individual investors, hold a 29% stake in Banco Products (India). While this size of ownership may not be enough to sway a policy decision in their favour, they can still make a collective impact on company policies.

Next Steps:

While it is well worth considering the different groups that own a company, there are other factors that are even more important. Like risks, for instance. Every company has them, and we've spotted 2 warning signs for Banco Products (India) (of which 1 shouldn't be ignored!) you should know about.

Of course this may not be the best stock to buy. So take a peek at this free free list of interesting companies.

NB: Figures in this article are calculated using data from the last twelve months, which refer to the 12-month period ending on the last date of the month the financial statement is dated. This may not be consistent with full year annual report figures.

Valuation is complex, but we're here to simplify it.

Discover if Banco Products (India) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:BANCOINDIA

Banco Products (India)

Engages in the manufacture and sale of heat exchangers/cooling systems in India and internationally.

Solid track record with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.557.6% undervalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.8% undervalued

63 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56054.5% undervalued

61 followersusers have followed this narrative

4 commentsusers have commented on this narrative

29 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2781.6% undervalued

33 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

AN

AntonioS on CAR Group ·

CAR Group. A wonderful compounding franchise at a fair-not-cheap price.

Fair Value:AU$3219.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

GA

GaryB on Palantir Technologies ·

Palantir hits 52 week low.

Fair Value:US$274.861.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

NO

North49_ on iShares - iShares MSCI South Korea ETF ·

EWY:US NYSE Arca iShares Msci South Korea ETF, an opportunity to diversify your tech investments.

Fair Value:US$273.4525.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9639.6% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

18 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7445.2% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.8% undervalued

63 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative