Advertisement

- Israel

- /

- Renewable Energy

- /

- TASE:ENRG

Energix - Renewable Energies (TLV:ENRG) Takes On Some Risk With Its Use Of Debt

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Energix - Renewable Energies Ltd. (TLV:ENRG) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Energix - Renewable Energies

What Is Energix - Renewable Energies's Net Debt?

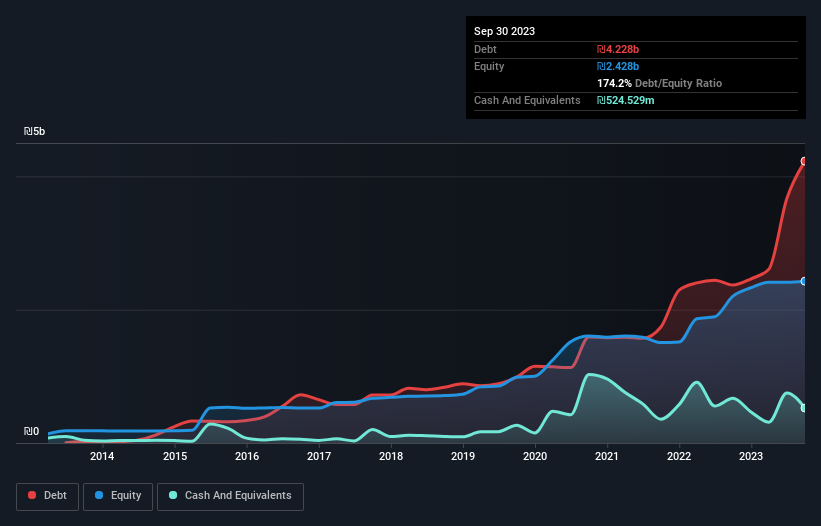

You can click the graphic below for the historical numbers, but it shows that as of September 2023 Energix - Renewable Energies had ₪4.23b of debt, an increase on ₪2.37b, over one year. On the flip side, it has ₪524.5m in cash leading to net debt of about ₪3.70b.

How Healthy Is Energix - Renewable Energies' Balance Sheet?

We can see from the most recent balance sheet that Energix - Renewable Energies had liabilities of ₪1.26b falling due within a year, and liabilities of ₪4.68b due beyond that. On the other hand, it had cash of ₪524.5m and ₪224.2m worth of receivables due within a year. So its liabilities total ₪5.20b more than the combination of its cash and short-term receivables.

This is a mountain of leverage relative to its market capitalization of ₪7.28b. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

As it happens Energix - Renewable Energies has a fairly concerning net debt to EBITDA ratio of 6.9 but very strong interest coverage of 26.6. So either it has access to very cheap long term debt or that interest expense is going to grow! Pleasingly, Energix - Renewable Energies is growing its EBIT faster than former Australian PM Bob Hawke downs a yard glass, boasting a 105% gain in the last twelve months. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Energix - Renewable Energies will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we always check how much of that EBIT is translated into free cash flow. During the last three years, Energix - Renewable Energies burned a lot of cash. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

We feel some trepidation about Energix - Renewable Energies's difficulty conversion of EBIT to free cash flow, but we've got positives to focus on, too. To wit both its interest cover and EBIT growth rate were encouraging signs. When we consider all the factors discussed, it seems to us that Energix - Renewable Energies is taking some risks with its use of debt. While that debt can boost returns, we think the company has enough leverage now. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 3 warning signs for Energix - Renewable Energies you should be aware of, and 2 of them are concerning.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Valuation is complex, but we're here to simplify it.

Discover if Energix - Renewable Energies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TASE:ENRG

Energix - Renewable Energies

Through its subsidiaries, engages in the initiation, development, financing, establishing, construction, management, and operation of facilities for the production, storage, and sale of electricity from renewable energy sources in Israel, Poland, Lithuania, and the United States.

Slight risk and overvalued.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor