Warren Buffett famously said, 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Blue Square Real Estate Ltd (TLV:BLSR) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Blue Square Real Estate

What Is Blue Square Real Estate's Debt?

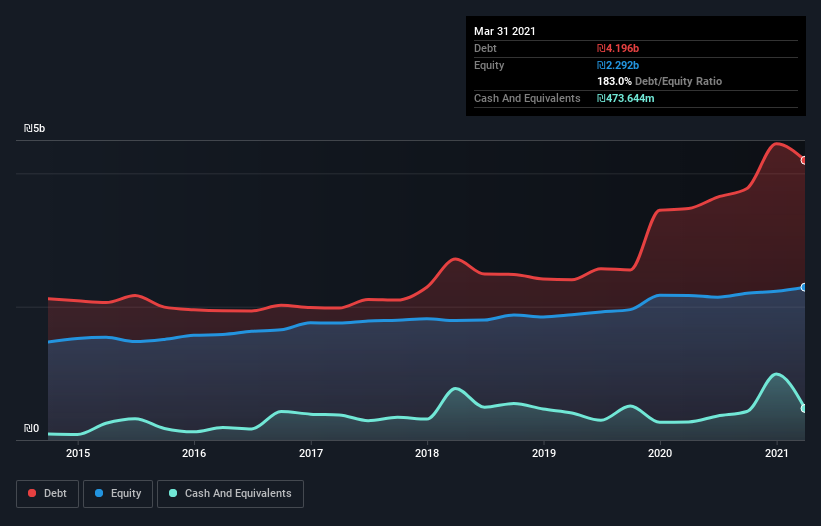

The image below, which you can click on for greater detail, shows that at March 2021 Blue Square Real Estate had debt of ₪4.20b, up from ₪3.47b in one year. On the flip side, it has ₪473.6m in cash leading to net debt of about ₪3.72b.

How Healthy Is Blue Square Real Estate's Balance Sheet?

We can see from the most recent balance sheet that Blue Square Real Estate had liabilities of ₪1.18b falling due within a year, and liabilities of ₪3.70b due beyond that. Offsetting these obligations, it had cash of ₪473.6m as well as receivables valued at ₪77.7m due within 12 months. So its liabilities total ₪4.33b more than the combination of its cash and short-term receivables.

This deficit casts a shadow over the ₪2.71b company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt. After all, Blue Square Real Estate would likely require a major re-capitalisation if it had to pay its creditors today.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Strangely Blue Square Real Estate has a sky high EBITDA ratio of 14.4, implying high debt, but a strong interest coverage of 28.9. So either it has access to very cheap long term debt or that interest expense is going to grow! It is well worth noting that Blue Square Real Estate's EBIT shot up like bamboo after rain, gaining 70% in the last twelve months. That'll make it easier to manage its debt. There's no doubt that we learn most about debt from the balance sheet. But it is Blue Square Real Estate's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it's worth checking how much of that EBIT is backed by free cash flow. Over the last three years, Blue Square Real Estate recorded free cash flow worth a fulsome 85% of its EBIT, which is stronger than we'd usually expect. That positions it well to pay down debt if desirable to do so.

Our View

Blue Square Real Estate's net debt to EBITDA was a real negative on this analysis, as was its level of total liabilities. But like a ballerina ending on a perfect pirouette, it has not trouble covering its interest expense with its EBIT. When we consider all the factors mentioned above, we do feel a bit cautious about Blue Square Real Estate's use of debt. While debt does have its upside in higher potential returns, we think shareholders should definitely consider how debt levels might make the stock more risky. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. For instance, we've identified 3 warning signs for Blue Square Real Estate (1 is concerning) you should be aware of.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

If you're looking for stocks to buy, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Blue Square Real Estate might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TASE:BLSR

Blue Square Real Estate

Develops, owns, leases, manages, and sells real estate properties in Israel.

Established dividend payer and good value.