Advertisement

- Israel

- /

- Household Products

- /

- TASE:SANO1

Assessing Sano Bruno's Enterprises (TASE:SANO1) Valuation After Profits Rose Despite Lower Quarterly Sales

Simply Wall St

Reviewed by Simply Wall St

Sano Bruno's Enterprises (TASE:SANO1) just posted third quarter results that mix slightly lower sales with higher profits, a combination that tends to catch investors' attention for what it implies about margins.

See our latest analysis for Sano Bruno's Enterprises.

The earnings beat on profitability seems to line up with the trend in the shares, with the latest share price at ₪398.5, a solid 90 day share price return of 16.01% and a robust three year total shareholder return of 80.25%. Together these figures point to momentum that has been building rather than fading.

If Sano Bruno's resilience has you thinking about what else might be quietly compounding in the background, this could be a good moment to explore fast growing stocks with high insider ownership.

With profits rising even as revenue slips and the share price already near record highs, the key question now is whether Sano Bruno's is still trading below its true value or if the market has already priced in future growth.

Price-to-Earnings of 16.9x: Is it justified?

On a price-to-earnings basis, Sano Bruno's trades at 16.9 times earnings, slightly below the broader Household Products peer group despite its recent strong share price performance.

The price to earnings multiple compares the current share price to the company’s per share earnings. It is a straightforward way to gauge how much investors are paying for each unit of profit in a relatively mature, cash generative consumer products business.

For Sano Bruno's, earnings have grown by an average of 4.6% per year over the past five years, but slipped 3.6% in the most recent year and return on equity is a modest 12.2%. This points to a solid yet unspectacular profitability profile that does not obviously demand a premium rating.

Compared with the Asian Household Products industry average price to earnings of 18 times and a peer average of 24.3 times, Sano Bruno's 16.9 times looks meaningfully cheaper. This suggests the market is willing to pay less for each shekel of its earnings than it does for comparable companies, even after the recent rally.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-earnings of 16.9x (ABOUT RIGHT)

However, softer recent earnings, modest 4.6% long term profit growth, and a slight intrinsic premium hint that enthusiasm could cool quickly.

Find out about the key risks to this Sano Bruno's Enterprises narrative.

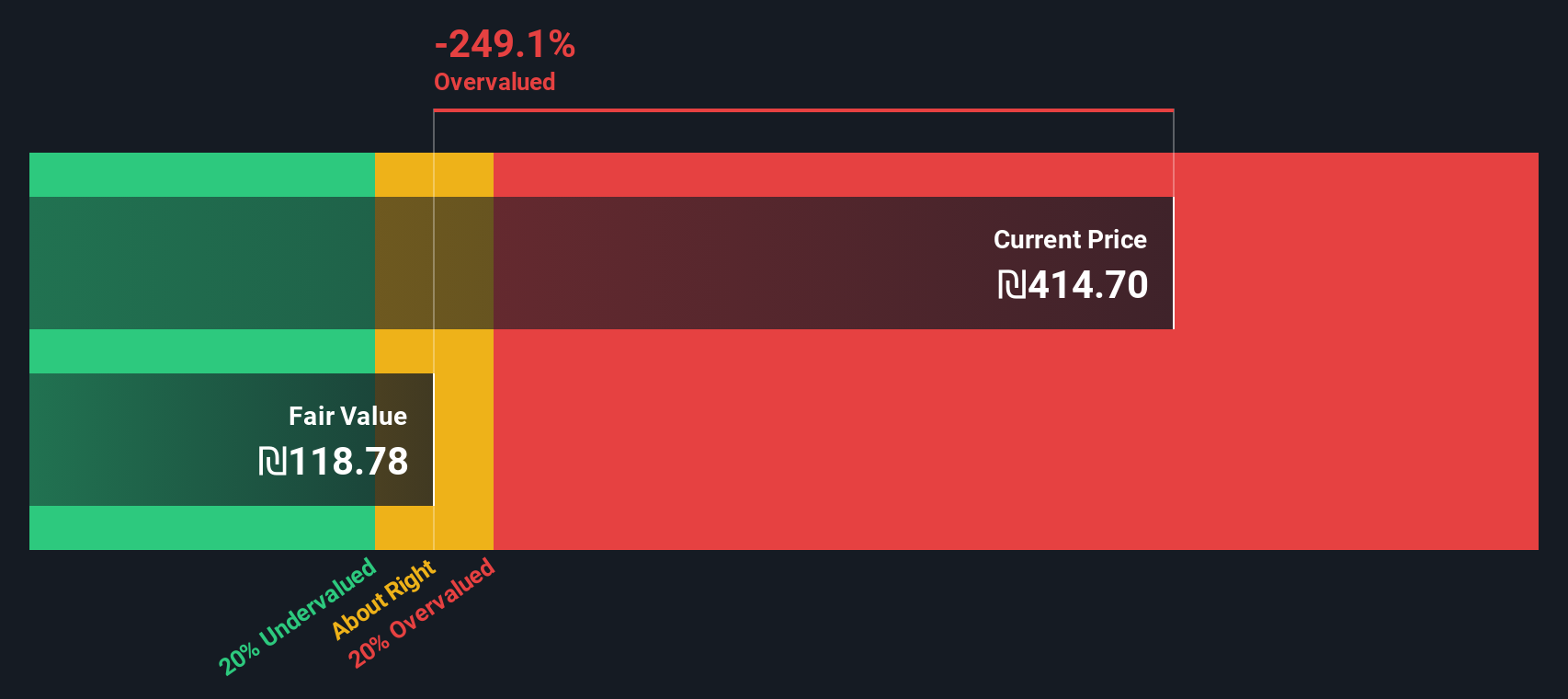

Another View: DCF Signals Overvaluation

While the earnings multiple suggests Sano Bruno's is reasonably priced, our DCF model presents a tougher picture. The stock is at ₪398.5 versus an estimated fair value of around ₪118.78, which implies it could be significantly overvalued if cash flow assumptions prove accurate.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Sano Bruno's Enterprises for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 917 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Sano Bruno's Enterprises Narrative

If this perspective does not quite align with your own or you prefer to dig into the numbers yourself, you can craft a personal view in minutes: Do it your way.

A good starting point is our analysis highlighting 1 key reward investors are optimistic about regarding Sano Bruno's Enterprises.

Ready for your next investing move?

Do not stop with one company. Use the Simply Wall St Screener to uncover fresh, data backed opportunities before everyone else rushes in.

- Capture potential mispricing by targeting companies that look cheap on fundamentals using these 917 undervalued stocks based on cash flows which is built to spotlight bargains others may overlook.

- Explore long term themes by finding innovative businesses at the intersection of medicine and machine learning through these 30 healthcare AI stocks before they attract wider attention.

- Navigate volatility by tracking digital asset enablers listed in these 81 cryptocurrency and blockchain stocks where blockchain adoption may influence long term earnings power.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TASE:SANO1

Sano Bruno's Enterprises

Engages in the development, production, marketing, distribution, and sale of non-food household and commercial consumer products in Israel and internationally.

Flawless balance sheet and slightly overvalued.

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.4% undervalued

40 followersusers have followed this narrative

6 commentsusers have commented on this narrative

11 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$123.8% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$244.5% overvalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$482.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6411.8% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on Alphabet ·

Positioned globally, partnered locally

Fair Value:US$390.1918.1% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

115 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.3% undervalued

952 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3406.0% undervalued

147 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative