- Israel

- /

- Oil and Gas

- /

- TASE:NWMD

NewMed Energy - Limited Partnership (TLV:NWMD) Seems To Use Debt Quite Sensibly

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that NewMed Energy - Limited Partnership (TLV:NWMD) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for NewMed Energy - Limited Partnership

What Is NewMed Energy - Limited Partnership's Debt?

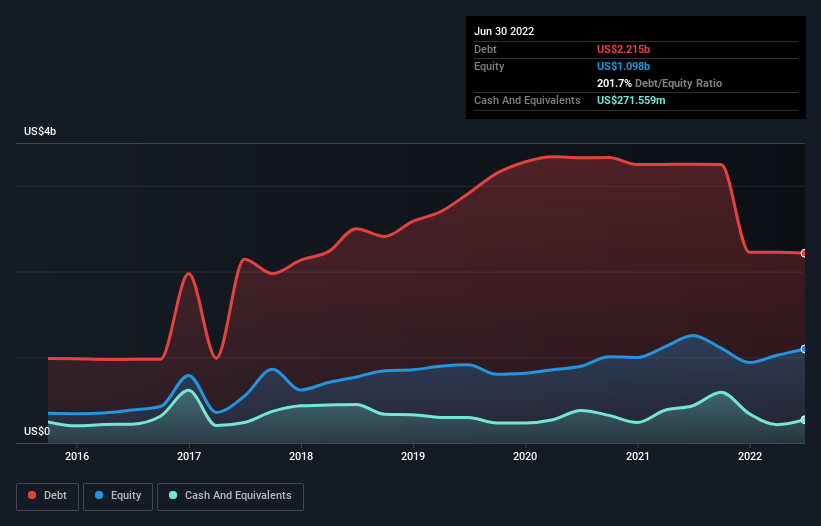

You can click the graphic below for the historical numbers, but it shows that NewMed Energy - Limited Partnership had US$2.21b of debt in June 2022, down from US$3.25b, one year before. However, because it has a cash reserve of US$271.6m, its net debt is less, at about US$1.94b.

How Healthy Is NewMed Energy - Limited Partnership's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that NewMed Energy - Limited Partnership had liabilities of US$617.1m due within 12 months and liabilities of US$2.07b due beyond that. Offsetting this, it had US$271.6m in cash and US$350.3m in receivables that were due within 12 months. So it has liabilities totalling US$2.07b more than its cash and near-term receivables, combined.

This deficit is considerable relative to its market capitalization of US$3.08b, so it does suggest shareholders should keep an eye on NewMed Energy - Limited Partnership's use of debt. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

NewMed Energy - Limited Partnership has a debt to EBITDA ratio of 2.8 and its EBIT covered its interest expense 3.1 times. Taken together this implies that, while we wouldn't want to see debt levels rise, we think it can handle its current leverage. On a lighter note, we note that NewMed Energy - Limited Partnership grew its EBIT by 28% in the last year. If it can maintain that kind of improvement, its debt load will begin to melt away like glaciers in a warming world. There's no doubt that we learn most about debt from the balance sheet. But it is NewMed Energy - Limited Partnership's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. In the last three years, NewMed Energy - Limited Partnership's free cash flow amounted to 46% of its EBIT, less than we'd expect. That weak cash conversion makes it more difficult to handle indebtedness.

Our View

When it comes to the balance sheet, the standout positive for NewMed Energy - Limited Partnership was the fact that it seems able to grow its EBIT confidently. But the other factors we noted above weren't so encouraging. For example, its interest cover makes us a little nervous about its debt. When we consider all the factors mentioned above, we do feel a bit cautious about NewMed Energy - Limited Partnership's use of debt. While we appreciate debt can enhance returns on equity, we'd suggest that shareholders keep close watch on its debt levels, lest they increase. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. For example NewMed Energy - Limited Partnership has 4 warning signs (and 2 which are a bit unpleasant) we think you should know about.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Valuation is complex, but we're here to simplify it.

Discover if NewMed Energy - Limited Partnership might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TASE:NWMD

NewMed Energy - Limited Partnership

Engages in the exploration, development, production, and sale of petroleum, natural gas, and condensate in Israel and Cyprus.

Proven track record with adequate balance sheet.

Market Insights

Community Narratives