Advertisement

- Israel

- /

- Aerospace & Defense

- /

- TASE:BSEN

The Bull Case For Bet Shemesh Engines Holdings (1997) (TASE:BSEN) Could Change Following Mixed Q3 2025 Results And Stronger Nine-Month Profitability Trends

Simply Wall St

Reviewed by Sasha Jovanovic

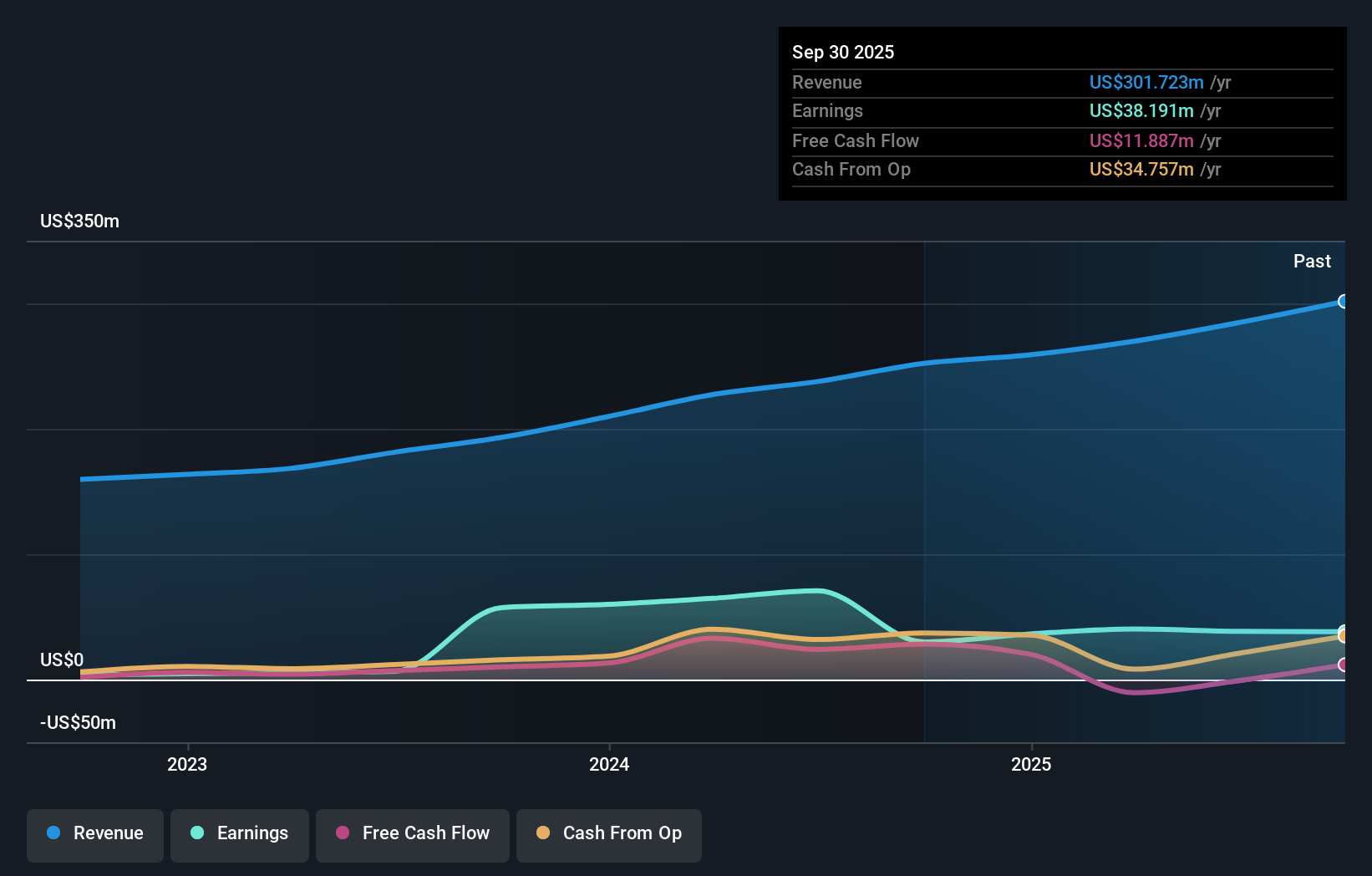

- Bet Shemesh Engines Holdings (1997) reported past third-quarter 2025 results with sales rising to US$84.67 million, while quarterly net income eased slightly to US$10.06 million and earnings per share ticked down year over year.

- Over the first nine months of 2025, the company grew sales to US$235.51 million and modestly increased net income and earnings per share, highlighting improving profitability on a year-to-date basis despite softer quarterly profit.

- We’ll now examine how the company’s stronger nine-month earnings progression shapes Bet Shemesh Engines’ investment narrative for investors.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

What Is Bet Shemesh Engines Holdings (1997)'s Investment Narrative?

To own Bet Shemesh Engines, you have to believe in its ability to turn solid aerospace demand into sustained, high quality earnings, despite some cost and margin pressure along the way. The latest Q3 2025 numbers support that broader thesis: sales continued to climb, nine‑month net income and EPS improved year on year, and profitability looks healthier on a year‑to‑date basis even though quarterly profit softened slightly. That mix suggests the immediate earnings story remains intact rather than materially altered by this release. Short term, the key catalysts still sit around order visibility, execution on existing programs and any decisions coming out of the January 2026 extraordinary shareholder meeting, while risks remain tied to rich valuation multiples, thinner dividend cover and any further squeeze on margins if costs rise faster than revenue.

However, one area in particular could catch investors off guard if conditions shift. Bet Shemesh Engines Holdings (1997)'s shares are on the way up, but could they be overextended? Uncover how much higher they are than fair value.Exploring Other Perspectives

Explore 2 other fair value estimates on Bet Shemesh Engines Holdings (1997) - why the stock might be worth as much as 40% more than the current price!

Build Your Own Bet Shemesh Engines Holdings (1997) Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Bet Shemesh Engines Holdings (1997) research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

- Our free Bet Shemesh Engines Holdings (1997) research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Bet Shemesh Engines Holdings (1997)'s overall financial health at a glance.

Searching For A Fresh Perspective?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bet Shemesh Engines Holdings (1997) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TASE:BSEN

Bet Shemesh Engines Holdings (1997)

Engages in the production of jet engine parts in Israel.

Flawless balance sheet with acceptable track record.

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.4% undervalued

41 followersusers have followed this narrative

6 commentsusers have commented on this narrative

14 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$123.8% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$244.5% overvalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

SC

scm on Text ·

TXT will see revenue grow 26% with a profit margin boost of almost 40%

Fair Value:zł8049.8% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$482.9% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6411.8% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.3% undervalued

955 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3406.0% undervalued

147 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative