Advertisement

- Hong Kong

- /

- Water Utilities

- /

- SEHK:855

China Water Affairs (SEHK:855) Net Profit Margin Drops to 8.2%, Undercutting Defensive Narrative

Simply Wall St

Reviewed by Simply Wall St

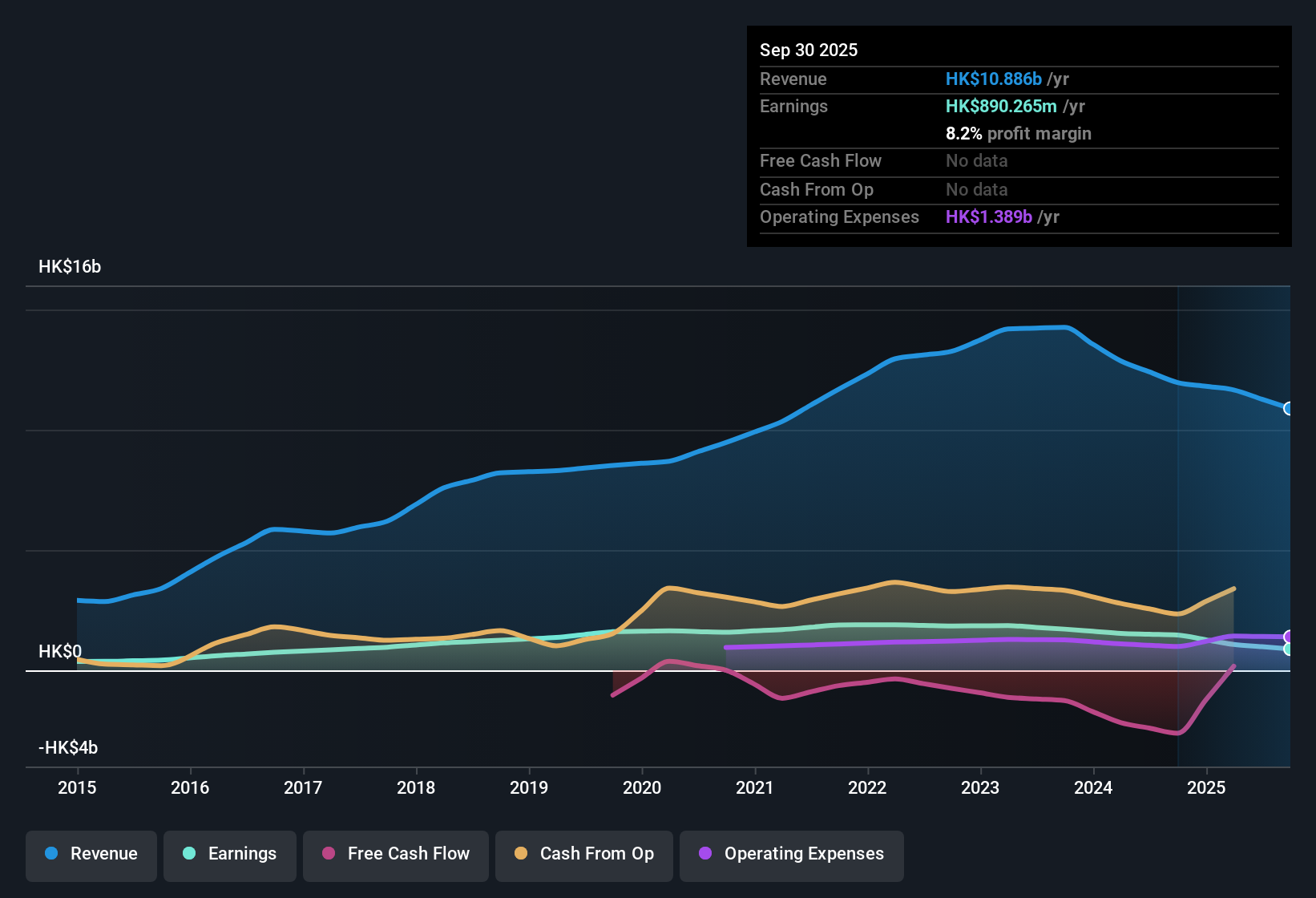

China Water Affairs Group (SEHK:855) just posted its H1 2026 financials, reporting revenue of $5.2 billion HKD and basic EPS of 0.35 HKD, with net income of $571 million HKD for the period. Looking back, the company has seen revenue trend from $5.9 billion HKD in H1 2025 to $5.7 billion HKD in H2 2025 and now $5.2 billion HKD. Basic EPS moved from 0.46 in H1 2025 to 0.19 in H2 2025 before rebounding to 0.35 this half. With margins coming under pressure, investors are sizing up these results for what they might signal about profitability in the future.

See our full analysis for China Water Affairs Group.Now comes the real challenge: it is time to see how these numbers measure up against the dominant narratives in the market, and whether the investment story still stands or gets a shake-up.

Curious how numbers become stories that shape markets? Explore Community Narratives

Margin Slide Cuts Deeper Than Revenue Fall

- Net profit margin dropped to 8.2% over the past year, down from 12.2%. This represents a steeper descent than revenue’s annualized decline of just 0.9% projected for the next three years.

- What stands out is that despite only a modest revenue dip forecast, the lower margin indicates that profitability took a more significant hit. This directly challenges the expectation that stable top-line trends would shield earnings.

- With trailing twelve-month net income at $890 million HKD on $10.9 billion HKD revenue, the margin squeeze means less of each dollar turns into earnings even if sales remain steady.

- This trend tests the view that essential utility services naturally guarantee predictable profits. It shows that cost pressures can outpace revenue resilience in this sector.

Valuation Gap Grows Despite Peers’ Premium

- The company’s price-to-earnings ratio sits at 10.7x, lower than the Asian Water Utilities average of 14.6x but still above the immediate peer average of 9x. The current share price of HK$5.87 trades 16.3% below both the DCF fair value (HK$7.01) and analyst target (HK$7.20).

- Consensus narrative highlights how China Water Affairs is valued as a “defensive” play by the broader sector, yet discounted versus intrinsic value estimates. This creates tension between perceived stability and lingering downside risk.

- The 22.7% gap to analyst target price suggests the market is cautious, potentially factoring in margin risks even as earnings are forecast to outpace the Hong Kong market at 17.7% annual growth.

- This divergence suggests that a rebound in valuation might require more tangible evidence that margin compression is bottoming out or that balance sheet risks, including debt concerns, are easing.

With shares below fair value and peer averages but profitability still under the microscope, find out how the consensus narrative explains this valuation disconnect in the full analysis. 📊 Read the full China Water Affairs Group Consensus Narrative.

Dividend Coverage Under Scrutiny as Debt Weighs

- Dividend yield stands at 4.77%, but dividends are not well covered by free cash flow and debt is flagged as not well covered by operating cash flow.

- Bears argue that high payouts look less secure when profit margins fall and debt service tightens, spotlighting a key risk for income-focused investors.

- The risk is that sustained margin pressure, coupled with shrinking cash flow buffers, could jeopardize future dividends or require balance sheet adjustments.

- This challenges the narrative that a high yield alone can offset underlying operational or financial headwinds, especially for a capital-intensive utility.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on China Water Affairs Group's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

China Water Affairs faces margin pressure and debt concerns, leaving investors questioning the reliability of its dividends and overall financial strength.

If you're looking for companies with stronger finances and more robust cash flow coverage, check out solid balance sheet and fundamentals stocks screener (1940 results) to focus on businesses better equipped for steady returns.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:855

China Water Affairs Group

An investment holding company, engages in the water supply, environmental protection, and property businesses in the People’s Republic of China.

Good value second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

138 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

931 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative