Advertisement

- Hong Kong

- /

- Renewable Energy

- /

- SEHK:686

Beijing Energy International Holding (HKG:686) Has No Shortage Of Debt

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, Beijing Energy International Holding Co., Ltd. (HKG:686) does carry debt. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Beijing Energy International Holding

What Is Beijing Energy International Holding's Debt?

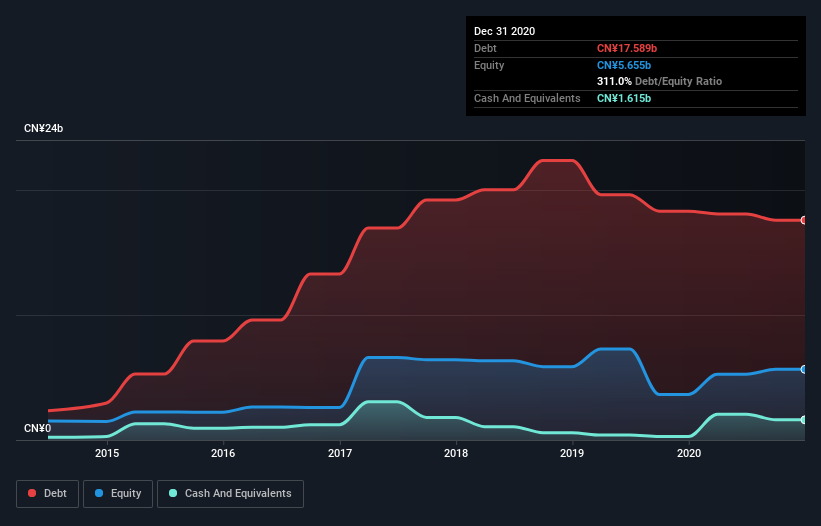

The chart below, which you can click on for greater detail, shows that Beijing Energy International Holding had CN¥17.6b in debt in December 2020; about the same as the year before. On the flip side, it has CN¥1.62b in cash leading to net debt of about CN¥16.0b.

How Healthy Is Beijing Energy International Holding's Balance Sheet?

The latest balance sheet data shows that Beijing Energy International Holding had liabilities of CN¥7.76b due within a year, and liabilities of CN¥12.7b falling due after that. Offsetting these obligations, it had cash of CN¥1.62b as well as receivables valued at CN¥6.24b due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by CN¥12.6b.

The deficiency here weighs heavily on the CN¥4.63b company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we'd watch its balance sheet closely, without a doubt. After all, Beijing Energy International Holding would likely require a major re-capitalisation if it had to pay its creditors today.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Beijing Energy International Holding shareholders face the double whammy of a high net debt to EBITDA ratio (8.6), and fairly weak interest coverage, since EBIT is just 1.3 times the interest expense. The debt burden here is substantial. Given the debt load, it's hardly ideal that Beijing Energy International Holding's EBIT was pretty flat over the last twelve months. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Beijing Energy International Holding's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So it's worth checking how much of that EBIT is backed by free cash flow. In the last three years, Beijing Energy International Holding created free cash flow amounting to 12% of its EBIT, an uninspiring performance. For us, cash conversion that low sparks a little paranoia about is ability to extinguish debt.

Our View

On the face of it, Beijing Energy International Holding's interest cover left us tentative about the stock, and its level of total liabilities was no more enticing than the one empty restaurant on the busiest night of the year. But at least its EBIT growth rate is not so bad. After considering the datapoints discussed, we think Beijing Energy International Holding has too much debt. That sort of riskiness is ok for some, but it certainly doesn't float our boat. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 1 warning sign for Beijing Energy International Holding you should be aware of.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

If you're looking for stocks to buy, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Beijing Energy International Holding might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:686

Beijing Energy International Holding

An investment holding company, engages in the investment, development, operation, and management of power plants and other clean energy projects in the People’s Republic of China, Australia, and Vietnam.

Slightly overvalued unattractive dividend payer.

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.8% undervalued

NO

Community Contributor