Advertisement

- Hong Kong

- /

- Renewable Energy

- /

- SEHK:412

Shandong Hi-Speed Holdings Group Limited (HKG:412) Looks Just Right With A 37% Price Jump

Shandong Hi-Speed Holdings Group Limited (HKG:412) shareholders have had their patience rewarded with a 37% share price jump in the last month. The last 30 days bring the annual gain to a very sharp 49%.

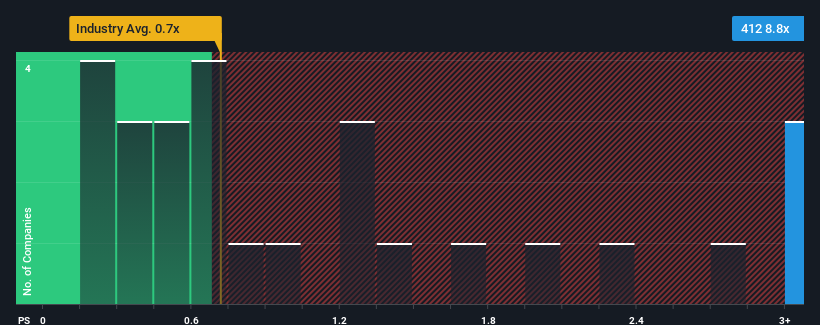

Following the firm bounce in price, when almost half of the companies in Hong Kong's Renewable Energy industry have price-to-sales ratios (or "P/S") below 0.7x, you may consider Shandong Hi-Speed Holdings Group as a stock not worth researching with its 8.8x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

See our latest analysis for Shandong Hi-Speed Holdings Group

What Does Shandong Hi-Speed Holdings Group's Recent Performance Look Like?

Revenue has risen firmly for Shandong Hi-Speed Holdings Group recently, which is pleasing to see. One possibility is that the P/S ratio is high because investors think this respectable revenue growth will be enough to outperform the broader industry in the near future. However, if this isn't the case, investors might get caught out paying too much for the stock.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Shandong Hi-Speed Holdings Group's earnings, revenue and cash flow.Do Revenue Forecasts Match The High P/S Ratio?

There's an inherent assumption that a company should far outperform the industry for P/S ratios like Shandong Hi-Speed Holdings Group's to be considered reasonable.

Retrospectively, the last year delivered a decent 12% gain to the company's revenues. While this performance is only fair, the company was still able to deliver immense revenue growth over the last three years. So we can start by confirming that the company has done a tremendous job of growing revenue over that time.

When compared to the industry's one-year growth forecast of 3.7%, the most recent medium-term revenue trajectory is noticeably more alluring

With this information, we can see why Shandong Hi-Speed Holdings Group is trading at such a high P/S compared to the industry. It seems most investors are expecting this strong growth to continue and are willing to pay more for the stock.

What We Can Learn From Shandong Hi-Speed Holdings Group's P/S?

Shares in Shandong Hi-Speed Holdings Group have seen a strong upwards swing lately, which has really helped boost its P/S figure. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

It's no surprise that Shandong Hi-Speed Holdings Group can support its high P/S given the strong revenue growth its experienced over the last three-year is superior to the current industry outlook. Right now shareholders are comfortable with the P/S as they are quite confident revenue aren't under threat. Barring any significant changes to the company's ability to make money, the share price should continue to be propped up.

Having said that, be aware Shandong Hi-Speed Holdings Group is showing 2 warning signs in our investment analysis, and 1 of those shouldn't be ignored.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:412

Shandong Hi-Speed Holdings Group

An investment holding company, operates photovoltaic and wind power plants in the People’s Republic of China.

Slight risk with questionable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.2% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|90.0% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.6% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|97.1% undervalued

AG

Community Contributor