Advertisement

- Hong Kong

- /

- Renewable Energy

- /

- SEHK:1381

Is Canvest Environmental Protection Group (HKG:1381) Using Too Much Debt?

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Canvest Environmental Protection Group Company Limited (HKG:1381) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for Canvest Environmental Protection Group

What Is Canvest Environmental Protection Group's Net Debt?

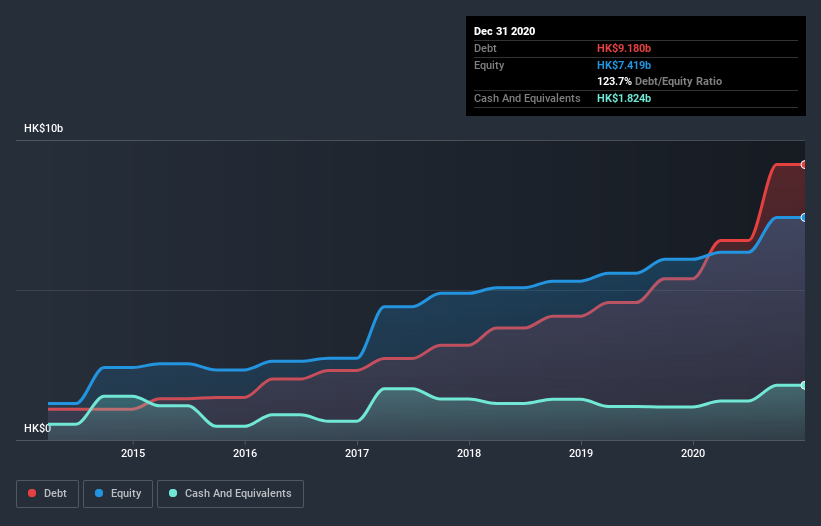

The image below, which you can click on for greater detail, shows that at December 2020 Canvest Environmental Protection Group had debt of HK$9.18b, up from HK$5.38b in one year. On the flip side, it has HK$1.82b in cash leading to net debt of about HK$7.36b.

How Strong Is Canvest Environmental Protection Group's Balance Sheet?

The latest balance sheet data shows that Canvest Environmental Protection Group had liabilities of HK$2.31b due within a year, and liabilities of HK$9.30b falling due after that. On the other hand, it had cash of HK$1.82b and HK$1.48b worth of receivables due within a year. So it has liabilities totalling HK$8.29b more than its cash and near-term receivables, combined.

This is a mountain of leverage relative to its market capitalization of HK$8.76b. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Canvest Environmental Protection Group's debt is 4.2 times its EBITDA, and its EBIT cover its interest expense 4.2 times over. Taken together this implies that, while we wouldn't want to see debt levels rise, we think it can handle its current leverage. On a lighter note, we note that Canvest Environmental Protection Group grew its EBIT by 21% in the last year. If it can maintain that kind of improvement, its debt load will begin to melt away like glaciers in a warming world. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Canvest Environmental Protection Group can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. During the last three years, Canvest Environmental Protection Group burned a lot of cash. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

Mulling over Canvest Environmental Protection Group's attempt at converting EBIT to free cash flow, we're certainly not enthusiastic. But on the bright side, its EBIT growth rate is a good sign, and makes us more optimistic. Looking at the bigger picture, it seems clear to us that Canvest Environmental Protection Group's use of debt is creating risks for the company. If all goes well, that should boost returns, but on the flip side, the risk of permanent capital loss is elevated by the debt. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should learn about the 2 warning signs we've spotted with Canvest Environmental Protection Group (including 1 which is a bit unpleasant) .

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

If you decide to trade Canvest Environmental Protection Group, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:1381

Canvest Environmental Protection Group

An investment holding company, engages in the operation and management of waste-to-energy (WTE) plants in the People’s Republic of China.

Fair value with acceptable track record.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|7.5% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.8% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|26.4% undervalued

GM

Community Contributor