- Hong Kong

- /

- Renewable Energy

- /

- SEHK:1071

Health Check: How Prudently Does Huadian Power International (HKG:1071) Use Debt?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Huadian Power International Corporation Limited (HKG:1071) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

Our analysis indicates that 1071 is potentially overvalued!

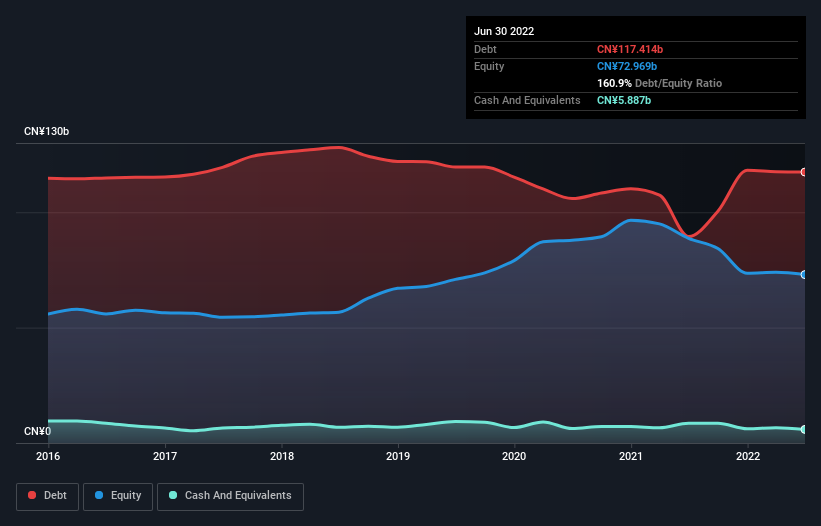

What Is Huadian Power International's Net Debt?

The image below, which you can click on for greater detail, shows that at June 2022 Huadian Power International had debt of CN¥117.4b, up from CN¥89.5b in one year. On the flip side, it has CN¥5.89b in cash leading to net debt of about CN¥111.5b.

A Look At Huadian Power International's Liabilities

Zooming in on the latest balance sheet data, we can see that Huadian Power International had liabilities of CN¥59.2b due within 12 months and liabilities of CN¥84.5b due beyond that. Offsetting these obligations, it had cash of CN¥5.89b as well as receivables valued at CN¥13.0b due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by CN¥124.8b.

The deficiency here weighs heavily on the CN¥53.5b company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we'd watch its balance sheet closely, without a doubt. After all, Huadian Power International would likely require a major re-capitalisation if it had to pay its creditors today. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Huadian Power International can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Over 12 months, Huadian Power International made a loss at the EBIT level, and saw its revenue drop to CN¥100b, which is a fall of 6.0%. We would much prefer see growth.

Caveat Emptor

Importantly, Huadian Power International had an earnings before interest and tax (EBIT) loss over the last year. Indeed, it lost a very considerable CN¥14b at the EBIT level. When we look at that alongside the significant liabilities, we're not particularly confident about the company. We'd want to see some strong near-term improvements before getting too interested in the stock. Not least because it had negative free cash flow of CN¥19b over the last twelve months. That means it's on the risky side of things. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. We've identified 2 warning signs with Huadian Power International , and understanding them should be part of your investment process.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

If you're looking to trade Huadian Power International, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Huadian Power International might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1071

Huadian Power International

Engages in the generation and sale of electricity, heat, and coal to power grid companies in the People’s Republic of China.

Undervalued with proven track record.