Tianjin Binhai Teda Logistics (Group) Corporation Limited (HKG:8348) Held Back By Insufficient Growth Even After Shares Climb 35%

Tianjin Binhai Teda Logistics (Group) Corporation Limited (HKG:8348) shares have continued their recent momentum with a 35% gain in the last month alone. The last 30 days bring the annual gain to a very sharp 29%.

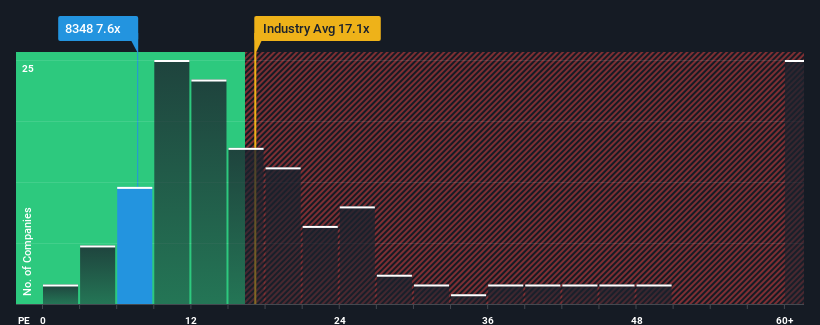

Even after such a large jump in price, Tianjin Binhai Teda Logistics (Group) may still be sending bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 7.6x, since almost half of all companies in Hong Kong have P/E ratios greater than 11x and even P/E's higher than 20x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

As an illustration, earnings have deteriorated at Tianjin Binhai Teda Logistics (Group) over the last year, which is not ideal at all. One possibility is that the P/E is low because investors think the company won't do enough to avoid underperforming the broader market in the near future. However, if this doesn't eventuate then existing shareholders may be feeling optimistic about the future direction of the share price.

See our latest analysis for Tianjin Binhai Teda Logistics (Group)

Does Growth Match The Low P/E?

In order to justify its P/E ratio, Tianjin Binhai Teda Logistics (Group) would need to produce sluggish growth that's trailing the market.

Retrospectively, the last year delivered a frustrating 7.5% decrease to the company's bottom line. At least EPS has managed not to go completely backwards from three years ago in aggregate, thanks to the earlier period of growth. So it appears to us that the company has had a mixed result in terms of growing earnings over that time.

Comparing that to the market, which is predicted to deliver 23% growth in the next 12 months, the company's momentum is weaker based on recent medium-term annualised earnings results.

In light of this, it's understandable that Tianjin Binhai Teda Logistics (Group)'s P/E sits below the majority of other companies. Apparently many shareholders weren't comfortable holding on to something they believe will continue to trail the bourse.

What We Can Learn From Tianjin Binhai Teda Logistics (Group)'s P/E?

The latest share price surge wasn't enough to lift Tianjin Binhai Teda Logistics (Group)'s P/E close to the market median. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Tianjin Binhai Teda Logistics (Group) maintains its low P/E on the weakness of its recent three-year growth being lower than the wider market forecast, as expected. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. Unless the recent medium-term conditions improve, they will continue to form a barrier for the share price around these levels.

Before you take the next step, you should know about the 4 warning signs for Tianjin Binhai Teda Logistics (Group) that we have uncovered.

You might be able to find a better investment than Tianjin Binhai Teda Logistics (Group). If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if Tianjin Binhai Teda Logistics (Group) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:8348

Tianjin Binhai Teda Logistics (Group)

Provides logistics services primarily in the People’s Republic of China.

Adequate balance sheet slight.