Advertisement

- Hong Kong

- /

- Transportation

- /

- SEHK:62

Don't Race Out To Buy Transport International Holdings Limited (HKG:62) Just Because It's Going Ex-Dividend

Transport International Holdings Limited (HKG:62) is about to trade ex-dividend in the next four days. Typically, the ex-dividend date is two business days before the record date, which is the date on which a company determines the shareholders eligible to receive a dividend. The ex-dividend date is important as the process of settlement involves at least two full business days. So if you miss that date, you would not show up on the company's books on the record date. This means that investors who purchase Transport International Holdings' shares on or after the 19th of May will not receive the dividend, which will be paid on the 26th of June.

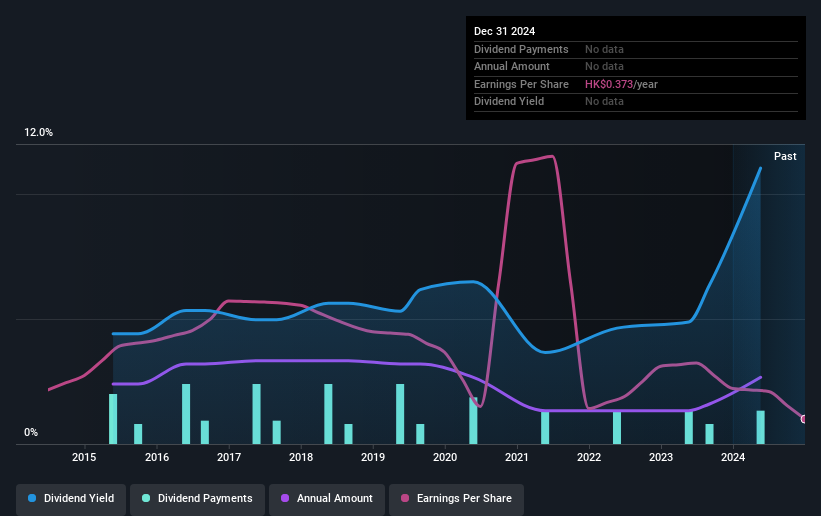

The company's upcoming dividend is HK$0.50 a share, following on from the last 12 months, when the company distributed a total of HK$0.50 per share to shareholders. Based on the last year's worth of payments, Transport International Holdings has a trailing yield of 5.4% on the current stock price of HK$9.22. If you buy this business for its dividend, you should have an idea of whether Transport International Holdings's dividend is reliable and sustainable. As a result, readers should always check whether Transport International Holdings has been able to grow its dividends, or if the dividend might be cut.

We've discovered 4 warning signs about Transport International Holdings. View them for free.Dividends are typically paid from company earnings. If a company pays more in dividends than it earned in profit, then the dividend could be unsustainable. Transport International Holdings distributed an unsustainably high 134% of its profit as dividends to shareholders last year. Without extenuating circumstances, we'd consider the dividend at risk of a cut. That said, even highly profitable companies sometimes might not generate enough cash to pay the dividend, which is why we should always check if the dividend is covered by cash flow. Luckily it paid out just 19% of its free cash flow last year.

It's disappointing to see that the dividend was not covered by profits, but cash is more important from a dividend sustainability perspective, and Transport International Holdings fortunately did generate enough cash to fund its dividend. Still, if the company repeatedly paid a dividend greater than its profits, we'd be concerned. Very few companies are able to sustainably pay dividends larger than their reported earnings.

Check out our latest analysis for Transport International Holdings

Have Earnings And Dividends Been Growing?

When earnings decline, dividend companies become much harder to analyse and own safely. If business enters a downturn and the dividend is cut, the company could see its value fall precipitously. Transport International Holdings's earnings per share have fallen at approximately 23% a year over the previous five years. When earnings per share fall, the maximum amount of dividends that can be paid also falls.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. Transport International Holdings has seen its dividend decline 5.7% per annum on average over the past 10 years, which is not great to see. It's never nice to see earnings and dividends falling, but at least management has cut the dividend rather than potentially risk the company's health in an attempt to maintain it.

Final Takeaway

From a dividend perspective, should investors buy or avoid Transport International Holdings? It's never great to see earnings per share declining, especially when a company is paying out 134% of its profit as dividends, which we feel is uncomfortably high. Yet cashflow was much stronger, which makes us wonder if there are some large timing issues in Transport International Holdings's cash flows, or perhaps the company has written down some assets aggressively, reducing its income. It's not the most attractive proposition from a dividend perspective, and we'd probably give this one a miss for now.

Having said that, if you're looking at this stock without much concern for the dividend, you should still be familiar of the risks involved with Transport International Holdings. Be aware that Transport International Holdings is showing 4 warning signs in our investment analysis, and 1 of those makes us a bit uncomfortable...

If you're in the market for strong dividend payers, we recommend checking our selection of top dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Transport International Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:62

Transport International Holdings

An investment holding company, provides franchised and non-franchised public transportation services in Hong Kong and Mainland China.

Adequate balance sheet slight.

Similar Companies

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.7% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|87.9% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|24.5% undervalued

CH

Community Contributor