Advertisement

- Hong Kong

- /

- Marine and Shipping

- /

- SEHK:3683

Great Harvest Maeta Holdings (HKG:3683) Shareholders Will Want The ROCE Trajectory To Continue

What trends should we look for it we want to identify stocks that can multiply in value over the long term? One common approach is to try and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. With that in mind, we've noticed some promising trends at Great Harvest Maeta Holdings (HKG:3683) so let's look a bit deeper.

Return On Capital Employed (ROCE): What is it?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. To calculate this metric for Great Harvest Maeta Holdings, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

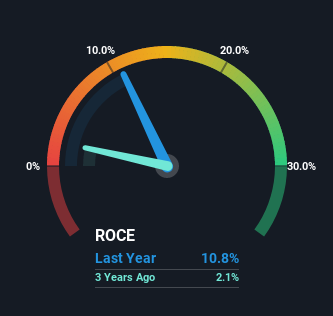

0.11 = US$7.8m ÷ (US$147m - US$74m) (Based on the trailing twelve months to March 2022).

So, Great Harvest Maeta Holdings has an ROCE of 11%. That's a relatively normal return on capital, and it's around the 12% generated by the Shipping industry.

See our latest analysis for Great Harvest Maeta Holdings

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you'd like to look at how Great Harvest Maeta Holdings has performed in the past in other metrics, you can view this free graph of past earnings, revenue and cash flow.

So How Is Great Harvest Maeta Holdings' ROCE Trending?

Shareholders will be relieved that Great Harvest Maeta Holdings has broken into profitability. The company was generating losses five years ago, but has managed to turn it around and as we saw earlier is now earning 11%, which is always encouraging. On top of that, what's interesting is that the amount of capital being employed has remained steady, so the business hasn't needed to put any additional money to work to generate these higher returns. So while we're happy that the business is more efficient, just keep in mind that could mean that going forward the business is lacking areas to invest internally for growth. After all, a company can only become a long term multi-bagger if it continually reinvests in itself at high rates of return.

On a side note, we noticed that the improvement in ROCE appears to be partly fueled by an increase in current liabilities. Essentially the business now has suppliers or short-term creditors funding about 51% of its operations, which isn't ideal. Given it's pretty high ratio, we'd remind investors that having current liabilities at those levels can bring about some risks in certain businesses.

The Key Takeaway

As discussed above, Great Harvest Maeta Holdings appears to be getting more proficient at generating returns since capital employed has remained flat but earnings (before interest and tax) are up. However the stock is down a substantial 84% in the last five years so there could be other areas of the business hurting its prospects. Still, it's worth doing some further research to see if the trends will continue into the future.

One more thing: We've identified 4 warning signs with Great Harvest Maeta Holdings (at least 2 which don't sit too well with us) , and understanding them would certainly be useful.

While Great Harvest Maeta Holdings may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:3683

Great Harvest Maeta Holdings

An investment holding company, provides dry bulk vessel chartering services worldwide.

Slightly overvalued with imperfect balance sheet.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|20.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|87.5% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|24.5% undervalued

CH

Community Contributor