Advertisement

- Hong Kong

- /

- Infrastructure

- /

- SEHK:357

Does Hainan Meilan International Airport (HKG:357) Have A Healthy Balance Sheet?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Hainan Meilan International Airport Company Limited (HKG:357) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Hainan Meilan International Airport

What Is Hainan Meilan International Airport's Debt?

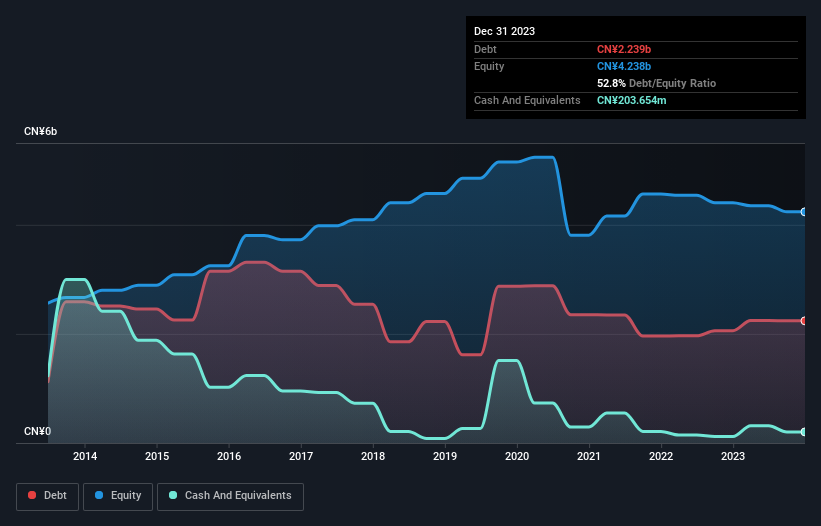

As you can see below, at the end of December 2023, Hainan Meilan International Airport had CN¥2.24b of debt, up from CN¥2.06b a year ago. Click the image for more detail. However, it also had CN¥203.7m in cash, and so its net debt is CN¥2.04b.

How Strong Is Hainan Meilan International Airport's Balance Sheet?

The latest balance sheet data shows that Hainan Meilan International Airport had liabilities of CN¥6.40b due within a year, and liabilities of CN¥724.4m falling due after that. On the other hand, it had cash of CN¥203.7m and CN¥462.5m worth of receivables due within a year. So its liabilities total CN¥6.46b more than the combination of its cash and short-term receivables.

This deficit casts a shadow over the CN¥3.78b company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. At the end of the day, Hainan Meilan International Airport would probably need a major re-capitalization if its creditors were to demand repayment. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Hainan Meilan International Airport's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Over 12 months, Hainan Meilan International Airport reported revenue of CN¥2.1b, which is a gain of 83%, although it did not report any earnings before interest and tax. With any luck the company will be able to grow its way to profitability.

Caveat Emptor

While we can certainly appreciate Hainan Meilan International Airport's revenue growth, its earnings before interest and tax (EBIT) loss is not ideal. To be specific the EBIT loss came in at CN¥71m. Considering that alongside the liabilities mentioned above make us nervous about the company. It would need to improve its operations quickly for us to be interested in it. It's fair to say the loss of CN¥136m didn't encourage us either; we'd like to see a profit. And until that time we think this is a risky stock. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. To that end, you should be aware of the 1 warning sign we've spotted with Hainan Meilan International Airport .

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Valuation is complex, but we're here to simplify it.

Discover if Hainan Meilan International Airport might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:357

Hainan Meilan International Airport

Engages in the aeronautical and non-aeronautical businesses at the Haikou Meilan Airport in the People's Republic of China.

Reasonable growth potential and fair value.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.7% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|87.9% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|24.5% undervalued

CH

Community Contributor