- Hong Kong

- /

- Infrastructure

- /

- SEHK:2880

Here's Why Liaoning PortLtd (HKG:2880) Can Manage Its Debt Responsibly

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Liaoning Port Co.,Ltd. (HKG:2880) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Liaoning PortLtd

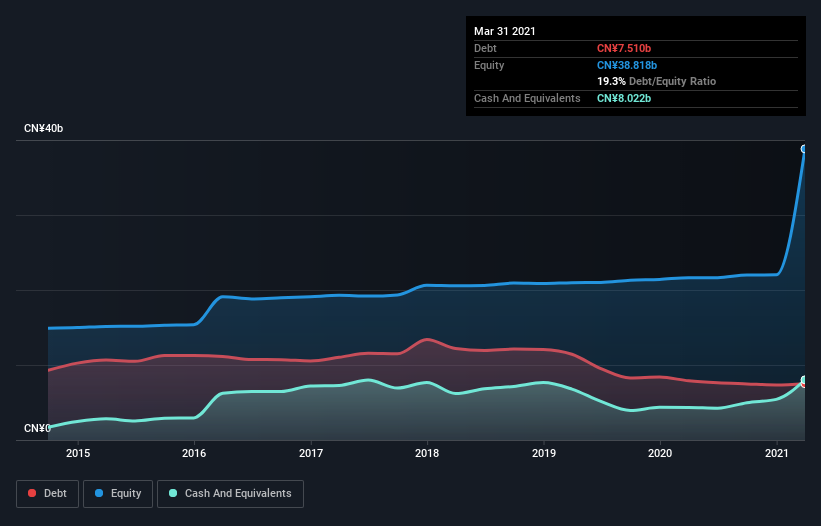

What Is Liaoning PortLtd's Debt?

As you can see below, Liaoning PortLtd had CN¥7.45b of debt at March 2021, down from CN¥7.89b a year prior. However, it does have CN¥8.02b in cash offsetting this, leading to net cash of CN¥573.3m.

How Healthy Is Liaoning PortLtd's Balance Sheet?

We can see from the most recent balance sheet that Liaoning PortLtd had liabilities of CN¥4.37b falling due within a year, and liabilities of CN¥13.1b due beyond that. Offsetting these obligations, it had cash of CN¥8.02b as well as receivables valued at CN¥3.52b due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by CN¥5.97b.

Given Liaoning PortLtd has a market capitalization of CN¥32.4b, it's hard to believe these liabilities pose much threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. Despite its noteworthy liabilities, Liaoning PortLtd boasts net cash, so it's fair to say it does not have a heavy debt load!

But the bad news is that Liaoning PortLtd has seen its EBIT plunge 14% in the last twelve months. If that rate of decline in earnings continues, the company could find itself in a tight spot. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since Liaoning PortLtd will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. While Liaoning PortLtd has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Happily for any shareholders, Liaoning PortLtd actually produced more free cash flow than EBIT over the last three years. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Summing up

Although Liaoning PortLtd's balance sheet isn't particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of CN¥573.3m. The cherry on top was that in converted 108% of that EBIT to free cash flow, bringing in CN¥1.6b. So we don't have any problem with Liaoning PortLtd's use of debt. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. Be aware that Liaoning PortLtd is showing 2 warning signs in our investment analysis , and 1 of those is potentially serious...

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

If you're looking for stocks to buy, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:2880

Excellent balance sheet second-rate dividend payer.

Market Insights

Community Narratives