After Leaping 31% JD Logistics, Inc. (HKG:2618) Shares Are Not Flying Under The Radar

The JD Logistics, Inc. (HKG:2618) share price has done very well over the last month, posting an excellent gain of 31%. Unfortunately, the gains of the last month did little to right the losses of the last year with the stock still down 23% over that time.

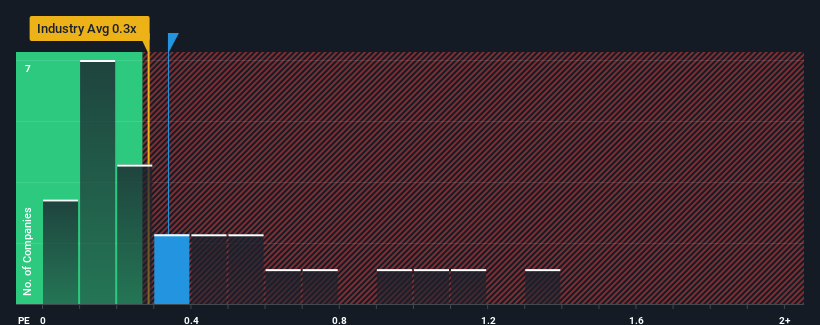

Although its price has surged higher, it's still not a stretch to say that JD Logistics' price-to-sales (or "P/S") ratio of 0.3x right now seems quite "middle-of-the-road" compared to the Logistics industry in Hong Kong, seeing as it matches the P/S ratio of the wider industry. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

View our latest analysis for JD Logistics

What Does JD Logistics' Recent Performance Look Like?

Recent times have been advantageous for JD Logistics as its revenues have been rising faster than most other companies. One possibility is that the P/S ratio is moderate because investors think this strong revenue performance might be about to tail off. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's not quite in favour.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on JD Logistics.Do Revenue Forecasts Match The P/S Ratio?

In order to justify its P/S ratio, JD Logistics would need to produce growth that's similar to the industry.

Taking a look back first, we see that the company grew revenue by an impressive 21% last year. The strong recent performance means it was also able to grow revenue by 127% in total over the last three years. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Shifting to the future, estimates from the analysts covering the company suggest revenue should grow by 9.2% per year over the next three years. That's shaping up to be similar to the 10% per year growth forecast for the broader industry.

With this in mind, it makes sense that JD Logistics' P/S is closely matching its industry peers. It seems most investors are expecting to see average future growth and are only willing to pay a moderate amount for the stock.

The Bottom Line On JD Logistics' P/S

JD Logistics appears to be back in favour with a solid price jump bringing its P/S back in line with other companies in the industry Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

A JD Logistics' P/S seems about right to us given the knowledge that analysts are forecasting a revenue outlook that is similar to the Logistics industry. At this stage investors feel the potential for an improvement or deterioration in revenue isn't great enough to push P/S in a higher or lower direction. If all things remain constant, the possibility of a drastic share price movement remains fairly remote.

It is also worth noting that we have found 1 warning sign for JD Logistics that you need to take into consideration.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:2618

JD Logistics

An investment holding company, provides integrated supply chain solutions and logistics services in the People’s Republic of China.

Flawless balance sheet and undervalued.