Advertisement

- Hong Kong

- /

- Infrastructure

- /

- SEHK:1199

These 4 Measures Indicate That COSCO SHIPPING Ports (HKG:1199) Is Using Debt Extensively

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, COSCO SHIPPING Ports Limited (HKG:1199) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for COSCO SHIPPING Ports

What Is COSCO SHIPPING Ports's Net Debt?

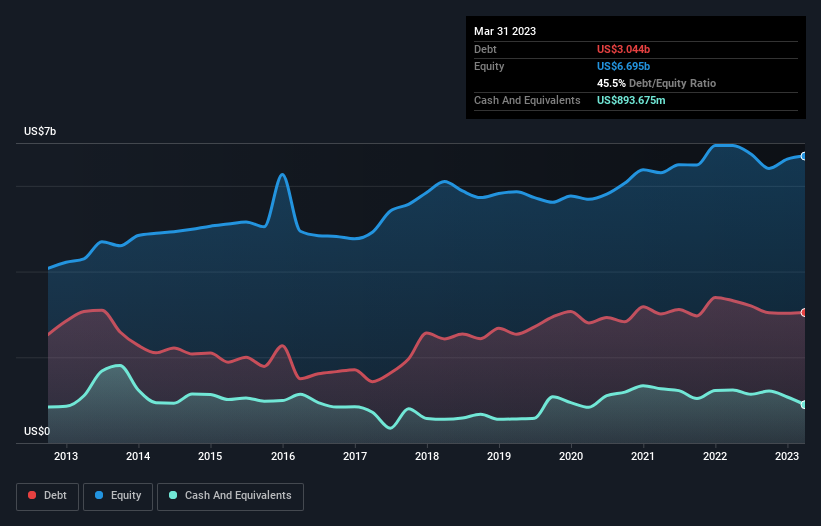

As you can see below, COSCO SHIPPING Ports had US$3.04b of debt at March 2023, down from US$3.32b a year prior. However, it does have US$893.7m in cash offsetting this, leading to net debt of about US$2.15b.

How Healthy Is COSCO SHIPPING Ports' Balance Sheet?

We can see from the most recent balance sheet that COSCO SHIPPING Ports had liabilities of US$1.32b falling due within a year, and liabilities of US$3.55b due beyond that. Offsetting this, it had US$893.7m in cash and US$302.6m in receivables that were due within 12 months. So it has liabilities totalling US$3.67b more than its cash and near-term receivables, combined.

This deficit casts a shadow over the US$2.02b company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt. At the end of the day, COSCO SHIPPING Ports would probably need a major re-capitalization if its creditors were to demand repayment.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

While COSCO SHIPPING Ports's debt to EBITDA ratio (4.5) suggests that it uses some debt, its interest cover is very weak, at 2.4, suggesting high leverage. So shareholders should probably be aware that interest expenses appear to have really impacted the business lately. On a slightly more positive note, COSCO SHIPPING Ports grew its EBIT at 18% over the last year, further increasing its ability to manage debt. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if COSCO SHIPPING Ports can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we always check how much of that EBIT is translated into free cash flow. During the last three years, COSCO SHIPPING Ports produced sturdy free cash flow equating to 56% of its EBIT, about what we'd expect. This cold hard cash means it can reduce its debt when it wants to.

Our View

We'd go so far as to say COSCO SHIPPING Ports's level of total liabilities was disappointing. But at least it's pretty decent at growing its EBIT; that's encouraging. It's also worth noting that COSCO SHIPPING Ports is in the Infrastructure industry, which is often considered to be quite defensive. Once we consider all the factors above, together, it seems to us that COSCO SHIPPING Ports's debt is making it a bit risky. Some people like that sort of risk, but we're mindful of the potential pitfalls, so we'd probably prefer it carry less debt. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. We've identified 2 warning signs with COSCO SHIPPING Ports , and understanding them should be part of your investment process.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1199

COSCO SHIPPING Ports

An investment holding company, manages and operates ports and terminals in Mainland China, Hong Kong, Europe, and internationally.

Undervalued with acceptable track record.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor