Advertisement

- Hong Kong

- /

- Infrastructure

- /

- SEHK:1199

News Flash: Analysts Just Made A Substantial Upgrade To Their COSCO SHIPPING Ports Limited (HKG:1199) Forecasts

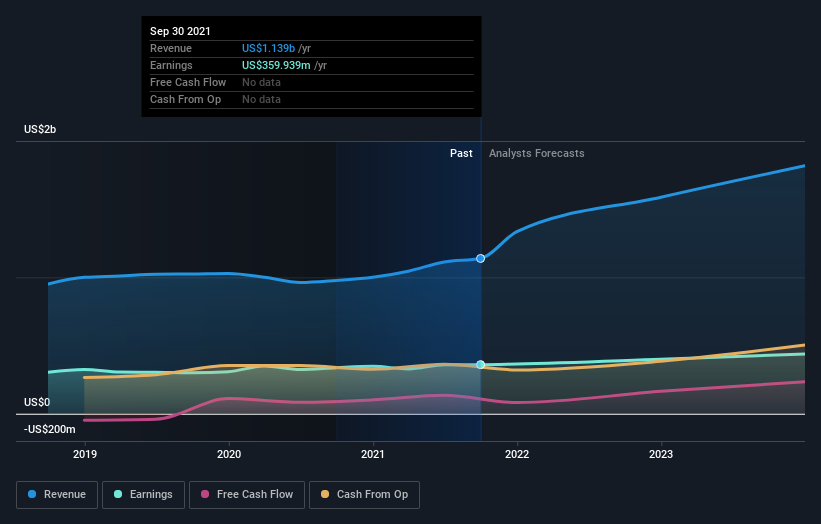

COSCO SHIPPING Ports Limited (HKG:1199) shareholders will have a reason to smile today, with the analysts making substantial upgrades to next year's forecasts. The analysts have sharply increased their revenue numbers, with a view that COSCO SHIPPING Ports will make substantially more sales than they'd previously expected. The stock price has risen 9.6% to HK$6.72 over the past week, suggesting investors are becoming more optimistic. Whether the upgrade is enough to drive the stock price higher is yet to be seen, however.

After this upgrade, COSCO SHIPPING Ports' nine analysts are now forecasting revenues of US$1.6b in 2022. This would be a sizeable 39% improvement in sales compared to the last 12 months. Before the latest update, the analysts were foreseeing US$1.3b of revenue in 2022. The consensus has definitely become more optimistic, showing a sizeable gain to revenue forecasts.

Check out our latest analysis for COSCO SHIPPING Ports

There was no particular change to the consensus price target of US$1.04, with COSCO SHIPPING Ports' latest outlook seemingly not enough to result in a change of valuation. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. The most optimistic COSCO SHIPPING Ports analyst has a price target of US$10.10 per share, while the most pessimistic values it at US$6.44. As you can see the range of estimates is wide, with the lowest valuation coming in at less than half the most bullish estimate, suggesting there are some strongly diverging views on how think this business will perform. As a result it might not be possible to derive much meaning from the consensus price target, which is after all just an average of this wide range of estimates.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. The analysts are definitely expecting COSCO SHIPPING Ports' growth to accelerate, with the forecast 30% annualised growth to the end of 2022 ranking favourably alongside historical growth of 12% per annum over the past five years. Compare this with other companies in the same industry, which are forecast to grow their revenue 6.6% annually. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect COSCO SHIPPING Ports to grow faster than the wider industry.

The Bottom Line

The highlight for us was that analysts increased their revenue forecasts for COSCO SHIPPING Ports next year. The analysts also expect revenues to grow faster than the wider market. Given that analysts appear to be expecting substantial improvement in the sales pipeline, now could be the right time to take another look at COSCO SHIPPING Ports.

Looking to learn more? We have analyst estimates for COSCO SHIPPING Ports going out to 2023, and you can see them free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1199

COSCO SHIPPING Ports

An investment holding company, manages and operates ports and terminals in Mainland China, Hong Kong, Europe, and internationally.

Undervalued with acceptable track record.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|8.8% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.3% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$384.84|18.1% undervalued

BL

Community Contributor