Advertisement

- Hong Kong

- /

- Telecom Services and Carriers

- /

- SEHK:762

China Unicom (Hong Kong) (HKG:762) Has A Pretty Healthy Balance Sheet

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that China Unicom (Hong Kong) Limited (HKG:762) does use debt in its business. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for China Unicom (Hong Kong)

What Is China Unicom (Hong Kong)'s Debt?

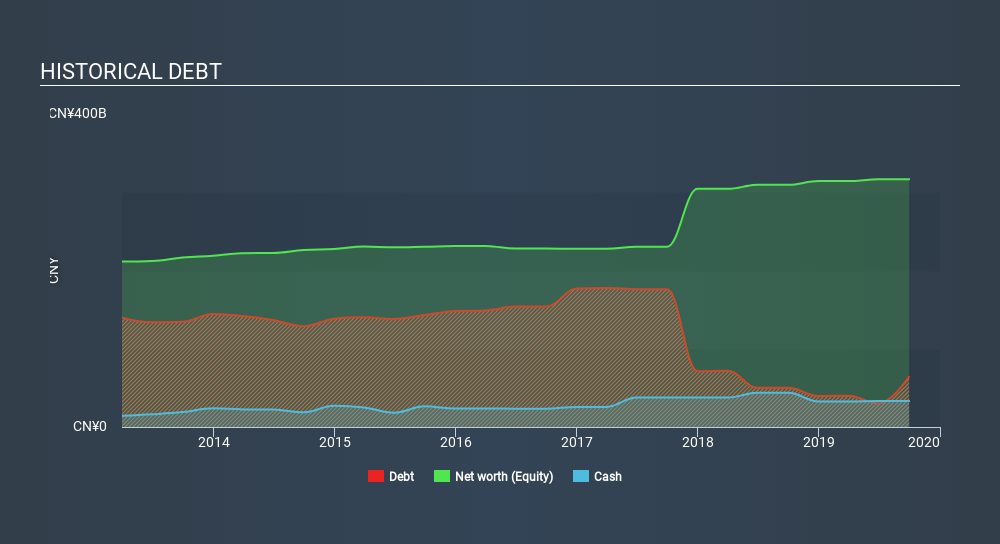

You can click the graphic below for the historical numbers, but it shows that as of June 2019 China Unicom (Hong Kong) had CN¥30.1b of debt, an increase on CN¥50.2k, over one year. But it also has CN¥33.3b in cash to offset that, meaning it has CN¥3.22b net cash.

A Look At China Unicom (Hong Kong)'s Liabilities

We can see from the most recent balance sheet that China Unicom (Hong Kong) had liabilities of CN¥211.2b falling due within a year, and liabilities of CN¥37.3b due beyond that. Offsetting these obligations, it had cash of CN¥33.3b as well as receivables valued at CN¥42.1b due within 12 months. So its liabilities total CN¥173.0b more than the combination of its cash and short-term receivables.

This deficit is considerable relative to its very significant market capitalization of CN¥193.2b, so it does suggest shareholders should keep an eye on China Unicom (Hong Kong)'s use of debt. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution. While it does have liabilities worth noting, China Unicom (Hong Kong) also has more cash than debt, so we're pretty confident it can manage its debt safely.

In addition to that, we're happy to report that China Unicom (Hong Kong) has boosted its EBIT by 70%, thus reducing the spectre of future debt repayments. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine China Unicom (Hong Kong)'s ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. While China Unicom (Hong Kong) has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the last three years, China Unicom (Hong Kong) actually produced more free cash flow than EBIT. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Summing up

Although China Unicom (Hong Kong)'s balance sheet isn't particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of CN¥3.22b. And it impressed us with free cash flow of CN¥33b, being 266% of its EBIT. So is China Unicom (Hong Kong)'s debt a risk? It doesn't seem so to us. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. For example, we've discovered 2 warning signs for China Unicom (Hong Kong) that you should be aware of before investing here.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About SEHK:762

China Unicom (Hong Kong)

An investment holding company, provides telecommunications and related value-added services in the People’s Republic of China.

Very undervalued with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor