Advertisement

Should You Be Impressed By VSTECS Holdings' (HKG:856) Returns on Capital?

What are the early trends we should look for to identify a stock that could multiply in value over the long term? Ideally, a business will show two trends; firstly a growing return on capital employed (ROCE) and secondly, an increasing amount of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. With that in mind, the ROCE of VSTECS Holdings (HKG:856) looks decent, right now, so lets see what the trend of returns can tell us.

Understanding Return On Capital Employed (ROCE)

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. Analysts use this formula to calculate it for VSTECS Holdings:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.17 = HK$1.2b ÷ (HK$23b - HK$16b) (Based on the trailing twelve months to June 2020).

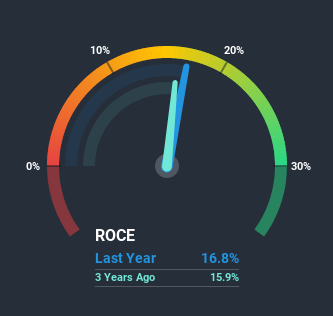

So, VSTECS Holdings has an ROCE of 17%. On its own, that's a standard return, however it's much better than the 8.1% generated by the Electronic industry.

View our latest analysis for VSTECS Holdings

Above you can see how the current ROCE for VSTECS Holdings compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like, you can check out the forecasts from the analysts covering VSTECS Holdings here for free.

What Does the ROCE Trend For VSTECS Holdings Tell Us?

The trend of ROCE doesn't stand out much, but returns on a whole are decent. The company has consistently earned 17% for the last five years, and the capital employed within the business has risen 73% in that time. Since 17% is a moderate ROCE though, it's good to see a business can continue to reinvest at these decent rates of return. Over long periods of time, returns like these might not be too exciting, but with consistency they can pay off in terms of share price returns.

On a side note, VSTECS Holdings' current liabilities are still rather high at 68% of total assets. This can bring about some risks because the company is basically operating with a rather large reliance on its suppliers or other sorts of short-term creditors. While it's not necessarily a bad thing, it can be beneficial if this ratio is lower.Our Take On VSTECS Holdings' ROCE

To sum it up, VSTECS Holdings has simply been reinvesting capital steadily, at those decent rates of return. And the stock has done incredibly well with a 283% return over the last five years, so long term investors are no doubt ecstatic with that result. So even though the stock might be more "expensive" than it was before, we think the strong fundamentals warrant this stock for further research.

One more thing to note, we've identified 3 warning signs with VSTECS Holdings and understanding these should be part of your investment process.

While VSTECS Holdings isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

When trading VSTECS Holdings or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:856

VSTECS Holdings

An investment holding company, develops information technology (IT) product channel and provides technical solution integration services in North Asia and South East Asia.

Adequate balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|17.0% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|11.8% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|81.8% undervalued

NO

Community Contributor