Advertisement

- Hong Kong

- /

- Communications

- /

- SEHK:6869

Yangtze Optical Fibre and Cable (SEHK:6869) Valuation After Governance Shake-Up at Extraordinary General Meeting

Simply Wall St

Reviewed by Simply Wall St

Yangtze Optical Fibre And Cable Limited (SEHK:6869) just pushed through a substantial governance shake up at its latest extraordinary general meeting, scrapping its supervisory board and refreshing the non executive lineup with two new directors.

See our latest analysis for Yangtze Optical Fibre And Cable Limited.

The governance reset comes after a huge run, with the share price up 188% year to date and a 214% one year total shareholder return, even though recent three month share price performance shows momentum cooling slightly.

If this shake up has you rethinking the broader tech opportunity, it could be worth scanning high growth tech and AI stocks for other potential high growth names on your radar.

With earnings growing fast and the share price already surging, the key question now is whether Yangtze Optical is still trading below its fundamentals, or if the market is already pricing in the next leg of growth?

Price-to-Earnings of 41.8x: Is it justified?

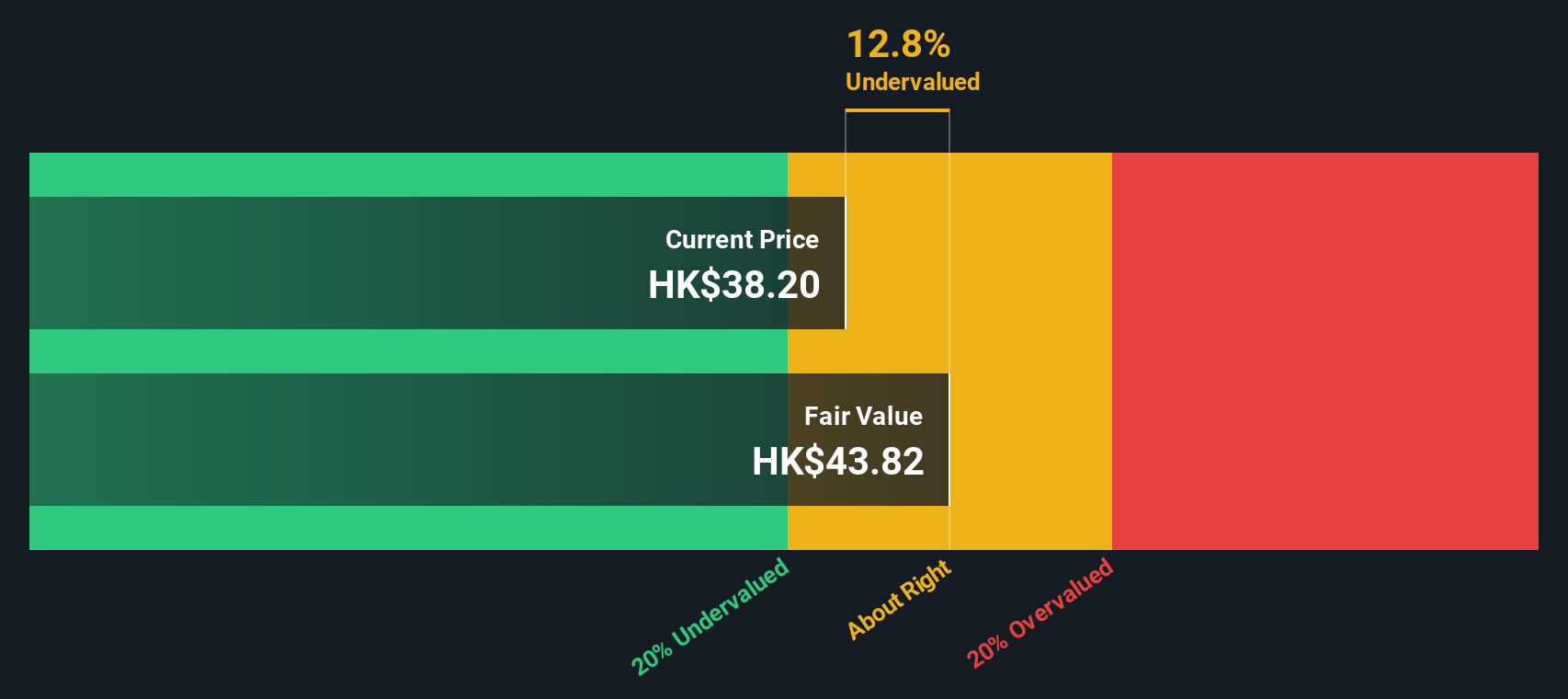

On a price-to-earnings ratio of 41.8x at the last close of HK$35.08, Yangtze Optical screens as expensive versus peers and its own fair ratio.

The price-to-earnings, or P E, compares what investors pay for each unit of current earnings. For a fast growing communications equipment name with forecast earnings growth above the wider Hong Kong market, a richer P E can signal that investors are already factoring in a strong profit recovery and future expansion.

Here, the market is paying meaningfully more for each dollar of earnings than both the estimated fair P E of 34.6x and the peer average of 15.2x. At the same time, the stock still trades about 19.8% below the HK$43.76 fair value from our DCF model. That combination suggests sentiment is skewed toward optimistic profit and revenue trajectories rather than current margins and return on equity.

Against the Asian communications industry average P E of 34.7x, Yangtze Optical's 41.8x multiple stands out as a clear premium that assumes it can outperform the sector on growth and quality over time, even after a year of weaker reported earnings.

Explore the SWS fair ratio for Yangtze Optical Fibre And Cable Limited

Result: Price-to-Earnings of 41.8x (OVERVALUED)

However, investors should watch for a sharper slowdown in demand or margin pressure from rising competition, as this could challenge the bullish growth assumptions embedded in the valuation.

Find out about the key risks to this Yangtze Optical Fibre And Cable Limited narrative.

Another View: DCF Points to Upside

While the current P E of 41.8x looks stretched, our DCF model tells a different story and suggests fair value closer to HK$43.76, around 19.8% above today’s HK$35.08 price. If cash flows are right, is the market still underestimating the recovery?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Yangtze Optical Fibre And Cable Limited for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 906 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Yangtze Optical Fibre And Cable Limited Narrative

If you see the numbers differently or want to stress test your own assumptions, you can build a personalised view in just a few minutes: Do it your way.

A great starting point for your Yangtze Optical Fibre And Cable Limited research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Ready for more high conviction ideas?

Do not stop at a single stock; use Simply Wall Street’s powerful screener to uncover focused opportunities that fit your strategy and keep your portfolio evolving intelligently.

- Target growth potential with these 26 AI penny stocks that could reshape entire industries and reward early, patient shareholders.

- Secure stronger income streams by hunting for these 15 dividend stocks with yields > 3% that can support long term returns and cushion market volatility.

- Lean into mispriced opportunities with these 906 undervalued stocks based on cash flows that may offer solid upside before the wider market catches on.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:6869

Yangtze Optical Fibre And Cable Limited

Engages in the production and sale of optical fiber preforms rods, optical fiber, and optical fiber cables in China and internationally.

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

50 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

MO

mo7md on ADNOC Gas ·

ADNOC Gas future shines with a 21.4% revenue surge

Fair Value:د.إ3.728.9% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IN

IncomeAssets on Pulse Seismic ·

Watch Pulse Seismic Outperform with 13.6% Revenue Growth in the Coming Years

Fair Value:CA$4.4727.3% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$481.5% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

957 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

50 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative