Advertisement

- Hong Kong

- /

- Real Estate

- /

- SEHK:1209

SEHK Value Stock Picks Including China Resources Mixc Lifestyle Services And 2 Others Estimated Below Intrinsic Value

Simply Wall St

Reviewed by Simply Wall St

As global markets experience fluctuations, the Hong Kong market has seen its benchmark Hang Seng Index decline significantly, reflecting waning optimism about economic stimulus measures from Beijing. In this environment of uncertainty, identifying undervalued stocks can be crucial for investors seeking opportunities that may offer potential value relative to their intrinsic worth.

Top 10 Undervalued Stocks Based On Cash Flows In Hong Kong

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| BYD Electronic (International) (SEHK:285) | HK$32.40 | HK$63.19 | 48.7% |

| Giant Biogene Holding (SEHK:2367) | HK$51.70 | HK$96.49 | 46.4% |

| Laopu Gold (SEHK:6181) | HK$160.10 | HK$308.52 | 48.1% |

| Kuaishou Technology (SEHK:1024) | HK$47.45 | HK$88.46 | 46.4% |

| Yadea Group Holdings (SEHK:1585) | HK$12.28 | HK$23.20 | 47.1% |

| Shanghai INT Medical Instruments (SEHK:1501) | HK$28.30 | HK$55.81 | 49.3% |

| CSC Financial (SEHK:6066) | HK$8.95 | HK$17.58 | 49.1% |

| Hangzhou SF Intra-city Industrial (SEHK:9699) | HK$10.48 | HK$19.50 | 46.3% |

| Innovent Biologics (SEHK:1801) | HK$44.60 | HK$80.73 | 44.8% |

| AK Medical Holdings (SEHK:1789) | HK$4.43 | HK$8.32 | 46.7% |

We're going to check out a few of the best picks from our screener tool.

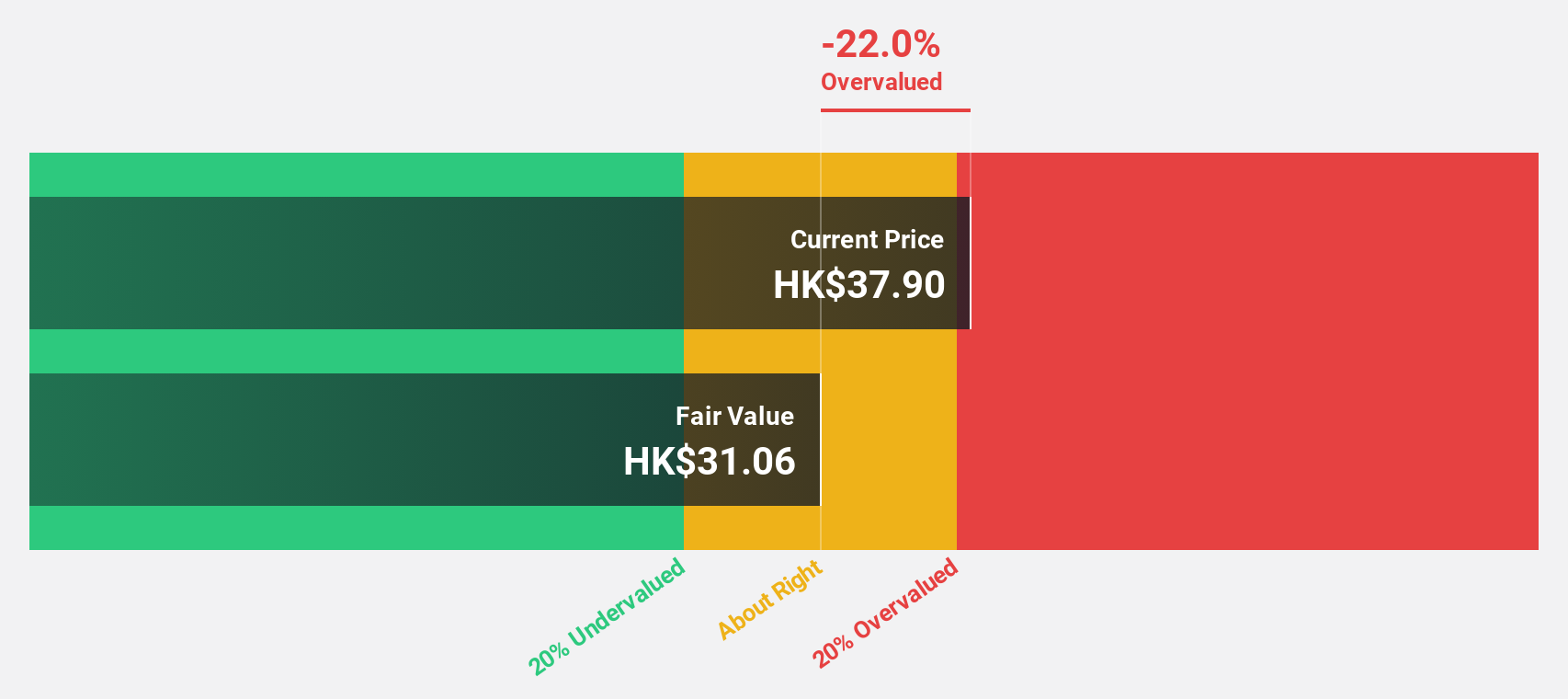

China Resources Mixc Lifestyle Services (SEHK:1209)

Overview: China Resources Mixc Lifestyle Services Limited is an investment holding company that offers property management and commercial operational services in the People's Republic of China, with a market capitalization of approximately HK$72.93 billion.

Operations: The company generates revenue through its property management business, which accounts for CN¥10.22 billion, and its commercial management business, contributing CN¥5.71 billion.

Estimated Discount To Fair Value: 41%

China Resources Mixc Lifestyle Services is trading at HK$31.95, significantly below its estimated fair value of HK$54.13, suggesting it may be undervalued based on cash flows. The company reported robust earnings growth of 33.1% over the past year and forecasts a 14.6% annual increase in earnings, outpacing the Hong Kong market average of 12.1%. Recent interim results showed improved sales and net income, enhancing its financial position amidst dividend increases and special payouts.

- Our comprehensive growth report raises the possibility that China Resources Mixc Lifestyle Services is poised for substantial financial growth.

- Click here to discover the nuances of China Resources Mixc Lifestyle Services with our detailed financial health report.

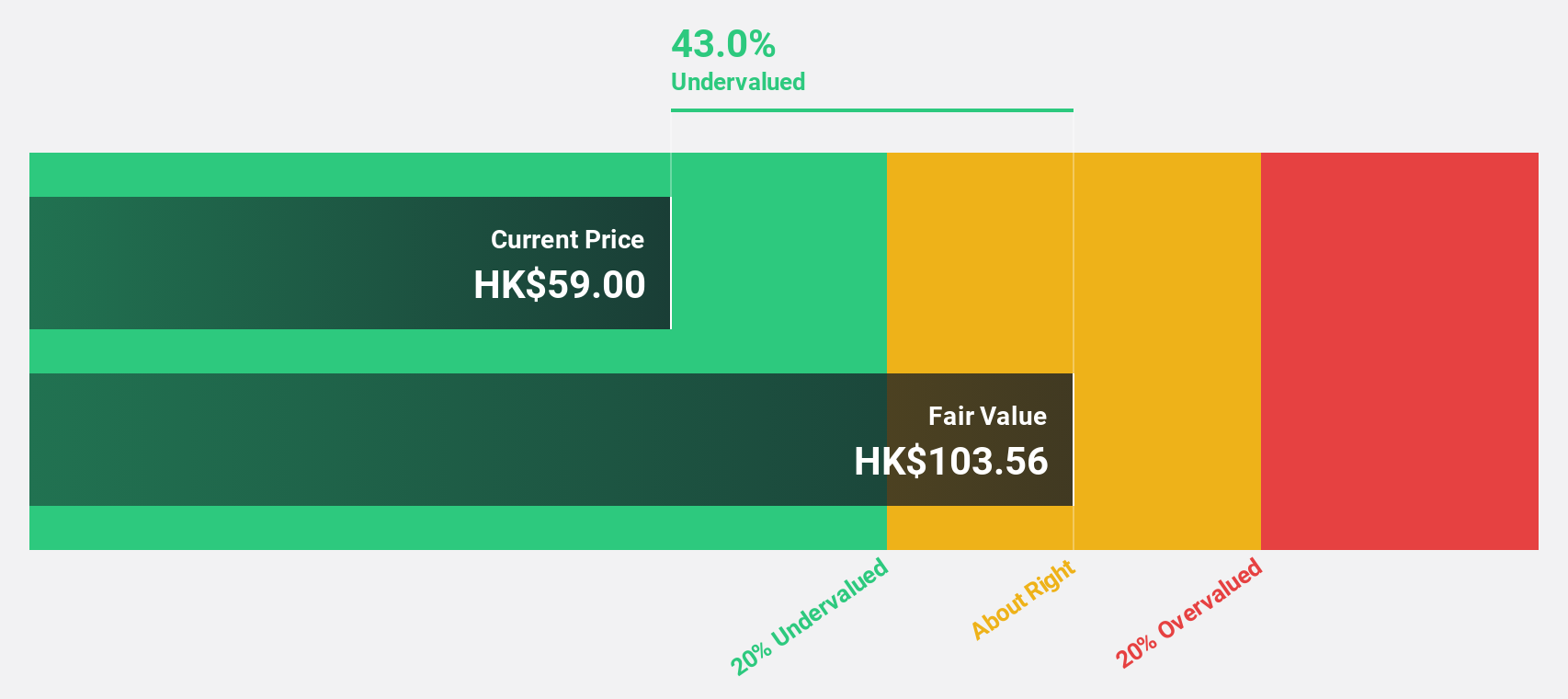

Giant Biogene Holding (SEHK:2367)

Overview: Giant Biogene Holding Co., Ltd. is an investment holding company involved in the research, development, manufacture, and sale of bioactive material-based beauty and health products in China, with a market cap of HK$52.18 billion.

Operations: The company generates revenue from its biotechnology segment, amounting to CN¥4.46 billion.

Estimated Discount To Fair Value: 46.4%

Giant Biogene Holding is trading at HK$51.7, significantly below its estimated fair value of HK$96.49, highlighting potential undervaluation based on cash flows. Recent earnings for the first half of 2024 showed substantial growth with sales reaching CNY 2.54 billion and net income rising to CNY 983.16 million. Earnings are projected to grow at a robust annual rate of over 23%, surpassing the Hong Kong market average, despite past shareholder dilution concerns.

- Upon reviewing our latest growth report, Giant Biogene Holding's projected financial performance appears quite optimistic.

- Unlock comprehensive insights into our analysis of Giant Biogene Holding stock in this financial health report.

BYD Electronic (International) (SEHK:285)

Overview: BYD Electronic (International) Company Limited is an investment holding company involved in the design, manufacture, assembly, and sale of mobile handset components and modules both in China and internationally, with a market cap of approximately HK$73 billion.

Operations: The company generates revenue of CN¥152.36 billion from its operations in the manufacture, assembly, and sale of mobile handset components and modules.

Estimated Discount To Fair Value: 48.7%

BYD Electronic (International) is trading at HK$32.4, well below its estimated fair value of HK$63.19, suggesting significant undervaluation based on cash flows. The company's recent earnings report for the first half of 2024 showed stable net income at CNY 1,517.8 million despite a sales increase to CNY 78.58 billion from the previous year. Earnings are expected to grow annually by over 24%, outpacing the Hong Kong market average growth rate.

- Insights from our recent growth report point to a promising forecast for BYD Electronic (International)'s business outlook.

- Navigate through the intricacies of BYD Electronic (International) with our comprehensive financial health report here.

Next Steps

- Reveal the 37 hidden gems among our Undervalued SEHK Stocks Based On Cash Flows screener with a single click here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:1209

China Resources Mixc Lifestyle Services

An investment holding company, engages in the provision of property management and commercial operational services in the People’s Republic of China.

Flawless balance sheet with solid track record.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor