- Hong Kong

- /

- Semiconductors

- /

- SEHK:1347

Hua Hong Semiconductor's (HKG:1347) earnings have declined over three years, contributing to shareholders 57% loss

While it may not be enough for some shareholders, we think it is good to see the Hua Hong Semiconductor Limited (HKG:1347) share price up 23% in a single quarter. Meanwhile over the last three years the stock has dropped hard. In that time, the share price dropped 57%. So it is really good to see an improvement. After all, could be that the fall was overdone.

While the stock has risen 3.6% in the past week but long term shareholders are still in the red, let's see what the fundamentals can tell us.

Check out our latest analysis for Hua Hong Semiconductor

To paraphrase Benjamin Graham: Over the short term the market is a voting machine, but over the long term it's a weighing machine. One flawed but reasonable way to assess how sentiment around a company has changed is to compare the earnings per share (EPS) with the share price.

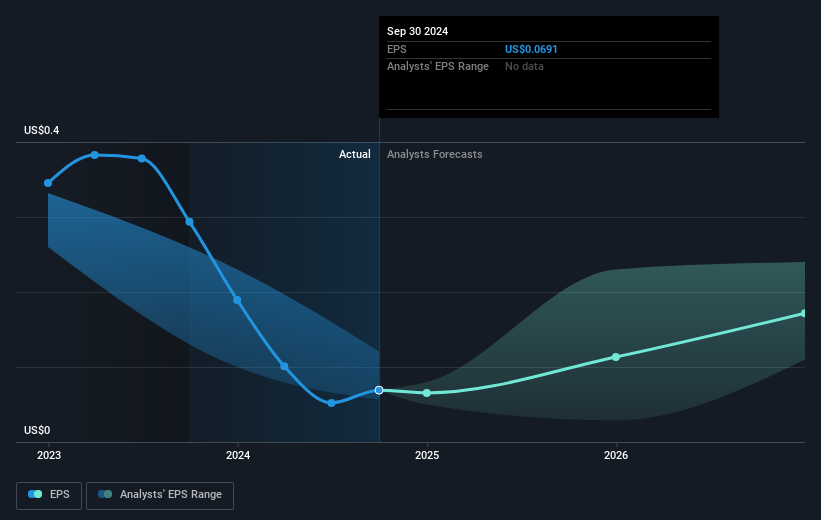

During the three years that the share price fell, Hua Hong Semiconductor's earnings per share (EPS) dropped by 19% each year. The share price decline of 25% is actually steeper than the EPS slippage. So it seems the market was too confident about the business, in the past.

You can see below how EPS has changed over time (discover the exact values by clicking on the image).

We're pleased to report that the CEO is remunerated more modestly than most CEOs at similarly capitalized companies. But while CEO remuneration is always worth checking, the really important question is whether the company can grow earnings going forward. Dive deeper into the earnings by checking this interactive graph of Hua Hong Semiconductor's earnings, revenue and cash flow.

A Different Perspective

Hua Hong Semiconductor's TSR for the year was broadly in line with the market average, at 20%. That gain looks pretty satisfying, and it is even better than the five-year TSR of 4% per year. Even if the share price growth slows down from here, there's a good chance that this is business worth watching in the long term. While it is well worth considering the different impacts that market conditions can have on the share price, there are other factors that are even more important. Consider for instance, the ever-present spectre of investment risk. We've identified 3 warning signs with Hua Hong Semiconductor (at least 1 which is a bit concerning) , and understanding them should be part of your investment process.

But note: Hua Hong Semiconductor may not be the best stock to buy. So take a peek at this free list of interesting companies with past earnings growth (and further growth forecast).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Hong Kong exchanges.

Valuation is complex, but we're here to simplify it.

Discover if Hua Hong Semiconductor might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1347

Hua Hong Semiconductor

An investment holding company, manufactures and sells semiconductor products.

Reasonable growth potential with mediocre balance sheet.