Advertisement

- Hong Kong

- /

- Retail Distributors

- /

- SEHK:8451

We Think Shareholders Are Less Likely To Approve A Pay Rise For Sunlight (1977) Holdings Limited's (HKG:8451) CEO For Now

The underwhelming share price performance of Sunlight (1977) Holdings Limited (HKG:8451) in the past three years would have disappointed many shareholders. What is concerning is that despite positive EPS growth, the share price has not tracked the trend in fundamentals. The AGM coming up on the 08 February 2022 could be an opportunity for shareholders to bring these concerns to the board's attention. They could also influence management through voting on resolutions such as executive remuneration. Here's our take on why we think shareholders may want to be cautious of approving a raise for the CEO at the moment.

View our latest analysis for Sunlight (1977) Holdings

Comparing Sunlight (1977) Holdings Limited's CEO Compensation With the industry

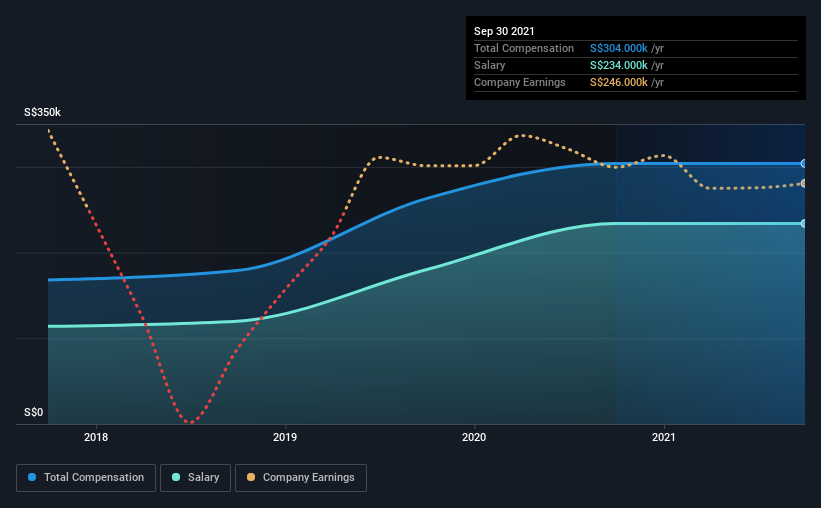

Our data indicates that Sunlight (1977) Holdings Limited has a market capitalization of HK$62m, and total annual CEO compensation was reported as S$304k for the year to September 2021. This was the same as last year. Notably, the salary which is S$234.0k, represents most of the total compensation being paid.

In comparison with other companies in the industry with market capitalizations under HK$1.6b, the reported median total CEO compensation was S$303k. This suggests that Sunlight (1977) Holdings remunerates its CEO largely in line with the industry average.

| Component | 2021 | 2020 | Proportion (2021) |

| Salary | S$234k | S$234k | 77% |

| Other | S$70k | S$70k | 23% |

| Total Compensation | S$304k | S$304k | 100% |

On an industry level, around 92% of total compensation represents salary and 8% is other remuneration. It's interesting to note that Sunlight (1977) Holdings allocates a smaller portion of compensation to salary in comparison to the broader industry. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

Sunlight (1977) Holdings Limited's Growth

Sunlight (1977) Holdings Limited's earnings per share (EPS) grew 71% per year over the last three years. In the last year, its revenue is down 11%.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. The lack of revenue growth isn't ideal, but it is the bottom line that counts most in business. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has Sunlight (1977) Holdings Limited Been A Good Investment?

Since shareholders would have lost about 27% over three years, some Sunlight (1977) Holdings Limited investors would surely be feeling negative emotions. So shareholders would probably want the company to be less generous with CEO compensation.

To Conclude...

Despite the growth in its earnings, the share price decline in the past three years is certainly concerning. A huge lag in share price growth when earnings have grown may indicate there could be other issues that are affecting the company at the moment that the market is focused on. Shareholders would be keen to know what's holding the stock back when earnings have grown. These concerns should be addressed at the upcoming AGM, where shareholders can question the board and evaluate if their judgement and decision making is still in line with their expectations.

CEO pay is simply one of the many factors that need to be considered while examining business performance. In our study, we found 3 warning signs for Sunlight (1977) Holdings you should be aware of, and 1 of them shouldn't be ignored.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:8451

Sunlight (1977) Holdings

An investment holding company, supplies tissue products and hygiene related products for corporate customers in Singapore.

Flawless balance sheet with questionable track record.

Market Insights

Advertisement

Community Narratives

Quality at a Premium. A time to watch, not to buy?

Fair Value US$154.56|29.3% undervalued

DA

Community Contributor

GRAB: The Super-App at the Heart of Southeast Asia’s Digital Boom

Fair Value US$6.60|7.0% undervalued

BL

Community Contributor

Verve Group to Surge with 51.61% Revenue Growth

Fair Value €6.00|65.0% undervalued

ME

Community Contributor