- Hong Kong

- /

- Specialty Stores

- /

- SEHK:590

Luk Fook Holdings (International) Limited Just Missed Revenue By 19%: Here's What Analysts Think Will Happen Next

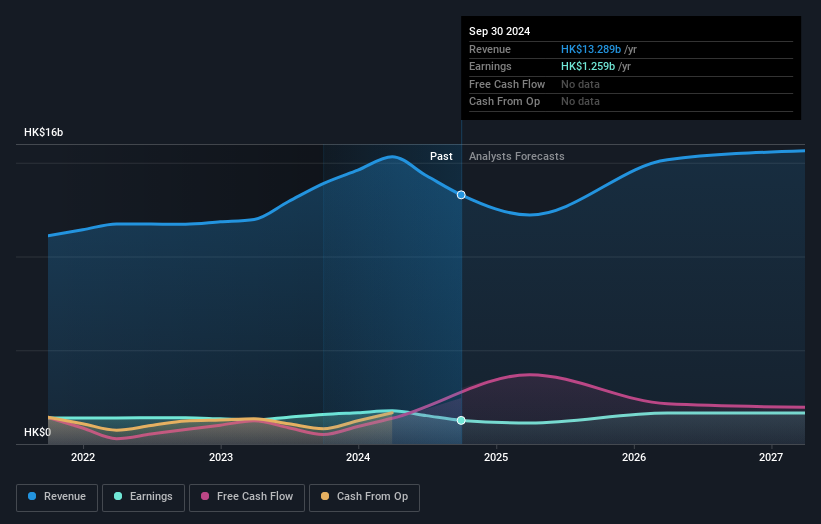

The half-yearly results for Luk Fook Holdings (International) Limited (HKG:590) were released last week, making it a good time to revisit its performance. Revenues were HK$5.4b, 19% below analyst expectations, although losses didn't appear to worsen significantly, with a statutory per-share loss of HK$3.01 being in line with what the analysts anticipated. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

See our latest analysis for Luk Fook Holdings (International)

Following the recent earnings report, the consensus from nine analysts covering Luk Fook Holdings (International) is for revenues of HK$12.2b in 2025. This implies a considerable 8.1% decline in revenue compared to the last 12 months. Statutory earnings per share are expected to fall 11% to HK$1.90 in the same period. In the lead-up to this report, the analysts had been modelling revenues of HK$14.6b and earnings per share (EPS) of HK$2.68 in 2025. Indeed, we can see that the analysts are a lot more bearish about Luk Fook Holdings (International)'s prospects following the latest results, administering a substantial drop in revenue estimates and slashing their EPS estimates to boot.

The consensus price target fell 10% to HK$17.91, with the weaker earnings outlook clearly leading valuation estimates. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. There are some variant perceptions on Luk Fook Holdings (International), with the most bullish analyst valuing it at HK$22.08 and the most bearish at HK$14.70 per share. These price targets show that analysts do have some differing views on the business, but the estimates do not vary enough to suggest to us that some are betting on wild success or utter failure.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. These estimates imply that revenue is expected to slow, with a forecast annualised decline of 16% by the end of 2025. This indicates a significant reduction from annual growth of 6.4% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 15% per year. It's pretty clear that Luk Fook Holdings (International)'s revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The most important thing to take away is that the analysts downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. Unfortunately, they also downgraded their revenue estimates, and our data indicates underperformance compared to the wider industry. Even so, earnings per share are more important to the intrinsic value of the business. The consensus price target fell measurably, with the analysts seemingly not reassured by the latest results, leading to a lower estimate of Luk Fook Holdings (International)'s future valuation.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have forecasts for Luk Fook Holdings (International) going out to 2027, and you can see them free on our platform here.

We don't want to rain on the parade too much, but we did also find 1 warning sign for Luk Fook Holdings (International) that you need to be mindful of.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:590

Luk Fook Holdings (International)

An investment holding company, engages in sourcing, designing, wholesaling, trademark licensing, and retailing various gold and platinum jewelry, and gem-set jewelry products.

Very undervalued with flawless balance sheet and pays a dividend.