- Hong Kong

- /

- Retail Distributors

- /

- SEHK:39

Does China Beidahuang Industry Group Holdings (HKG:39) Have A Healthy Balance Sheet?

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, China Beidahuang Industry Group Holdings Limited (HKG:39) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for China Beidahuang Industry Group Holdings

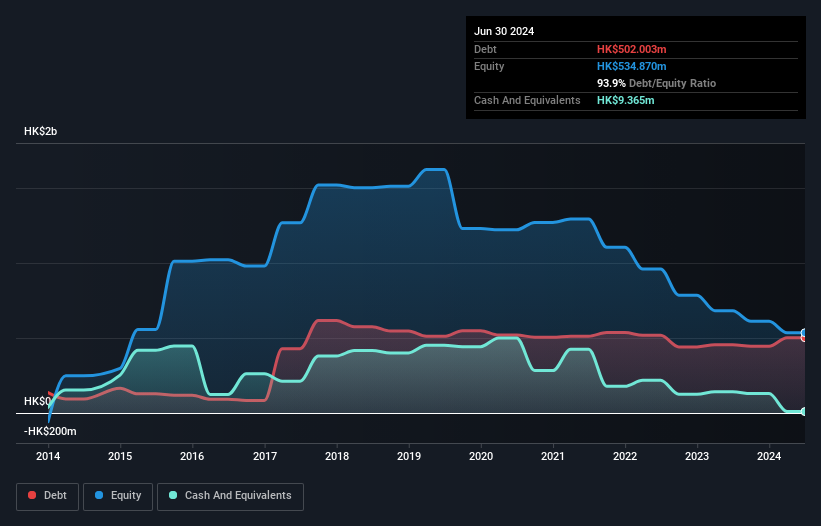

What Is China Beidahuang Industry Group Holdings's Net Debt?

As you can see below, at the end of June 2024, China Beidahuang Industry Group Holdings had HK$502.0m of debt, up from HK$454.9m a year ago. Click the image for more detail. And it doesn't have much cash, so its net debt is about the same.

How Strong Is China Beidahuang Industry Group Holdings' Balance Sheet?

We can see from the most recent balance sheet that China Beidahuang Industry Group Holdings had liabilities of HK$1.22b falling due within a year, and liabilities of HK$95.3m due beyond that. Offsetting this, it had HK$9.37m in cash and HK$337.4m in receivables that were due within 12 months. So its liabilities total HK$968.3m more than the combination of its cash and short-term receivables.

This deficit casts a shadow over the HK$506.6m company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt. At the end of the day, China Beidahuang Industry Group Holdings would probably need a major re-capitalization if its creditors were to demand repayment. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since China Beidahuang Industry Group Holdings will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year China Beidahuang Industry Group Holdings had a loss before interest and tax, and actually shrunk its revenue by 5.7%, to HK$864m. We would much prefer see growth.

Caveat Emptor

Importantly, China Beidahuang Industry Group Holdings had an earnings before interest and tax (EBIT) loss over the last year. Indeed, it lost HK$39m at the EBIT level. Considering that alongside the liabilities mentioned above make us nervous about the company. It would need to improve its operations quickly for us to be interested in it. It's fair to say the loss of HK$172m didn't encourage us either; we'd like to see a profit. In the meantime, we consider the stock to be risky. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 2 warning signs for China Beidahuang Industry Group Holdings (1 is concerning!) that you should be aware of before investing here.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

If you're looking to trade China Beidahuang Industry Group Holdings, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:39

China Beidahuang Industry Group Holdings

An investment holding company, engages in the wine and liquor, food products trading, construction and development, rental, financial leasing, and mineral products businesses in the People’s Republic of China and Hong Kong.

Mediocre balance sheet very low.

Market Insights

Community Narratives