- Hong Kong

- /

- Specialty Stores

- /

- SEHK:3813

Is Pou Sheng International (Holdings) (HKG:3813) A Risky Investment?

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Pou Sheng International (Holdings) Limited (HKG:3813) does have debt on its balance sheet. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Pou Sheng International (Holdings)

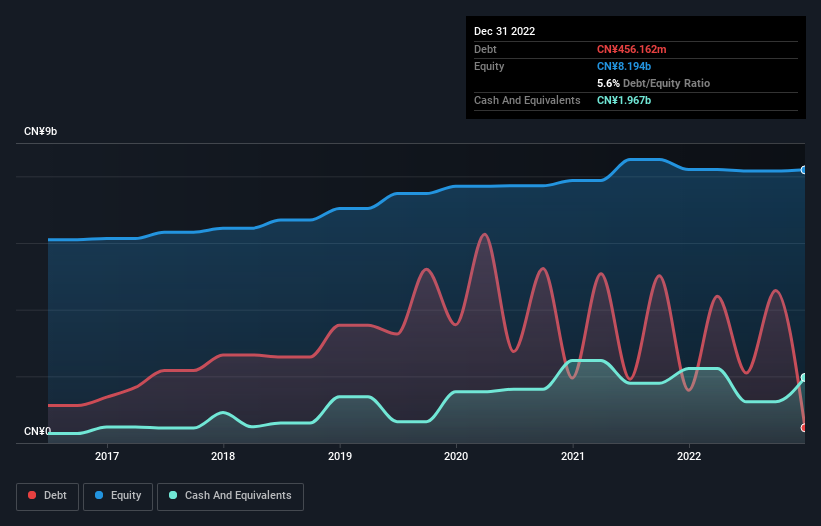

What Is Pou Sheng International (Holdings)'s Debt?

The image below, which you can click on for greater detail, shows that Pou Sheng International (Holdings) had debt of CN¥456.2m at the end of December 2022, a reduction from CN¥4.40b over a year. But it also has CN¥1.97b in cash to offset that, meaning it has CN¥1.51b net cash.

How Healthy Is Pou Sheng International (Holdings)'s Balance Sheet?

According to the last reported balance sheet, Pou Sheng International (Holdings) had liabilities of CN¥3.94b due within 12 months, and liabilities of CN¥1.46b due beyond 12 months. On the other hand, it had cash of CN¥1.97b and CN¥1.13b worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by CN¥2.31b.

This deficit is considerable relative to its market capitalization of CN¥3.72b, so it does suggest shareholders should keep an eye on Pou Sheng International (Holdings)'s use of debt. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry. Despite its noteworthy liabilities, Pou Sheng International (Holdings) boasts net cash, so it's fair to say it does not have a heavy debt load!

Unfortunately, Pou Sheng International (Holdings)'s EBIT flopped 10% over the last four quarters. If that sort of decline is not arrested, then the managing its debt will be harder than selling broccoli flavoured ice-cream for a premium. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Pou Sheng International (Holdings)'s ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. Pou Sheng International (Holdings) may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the last three years, Pou Sheng International (Holdings) actually produced more free cash flow than EBIT. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Summing Up

While Pou Sheng International (Holdings) does have more liabilities than liquid assets, it also has net cash of CN¥1.51b. And it impressed us with free cash flow of CN¥2.4b, being 284% of its EBIT. So we are not troubled with Pou Sheng International (Holdings)'s debt use. We'd be motivated to research the stock further if we found out that Pou Sheng International (Holdings) insiders have bought shares recently. If you would too, then you're in luck, since today we're sharing our list of reported insider transactions for free.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:3813

Pou Sheng International (Holdings)

An investment holding company, engages in distributing and retailing sportswear and footwear in the People’s Republic of China and internationally.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Community Narratives