- Hong Kong

- /

- Specialty Stores

- /

- SEHK:330

Shareholders in Esprit Holdings (HKG:330) have lost 88%, as stock drops 15% this past week

Some stocks are best avoided. We really hate to see fellow investors lose their hard-earned money. Imagine if you held Esprit Holdings Limited (HKG:330) for half a decade as the share price tanked 89%. And some of the more recent buyers are probably worried, too, with the stock falling 74% in the last year. More recently, the share price has dropped a further 29% in a month. We really feel for shareholders in this scenario. It's a good reminder of the importance of diversification, and it's worth keeping in mind there's more to life than money, anyway.

After losing 15% this past week, it's worth investigating the company's fundamentals to see what we can infer from past performance.

Check out our latest analysis for Esprit Holdings

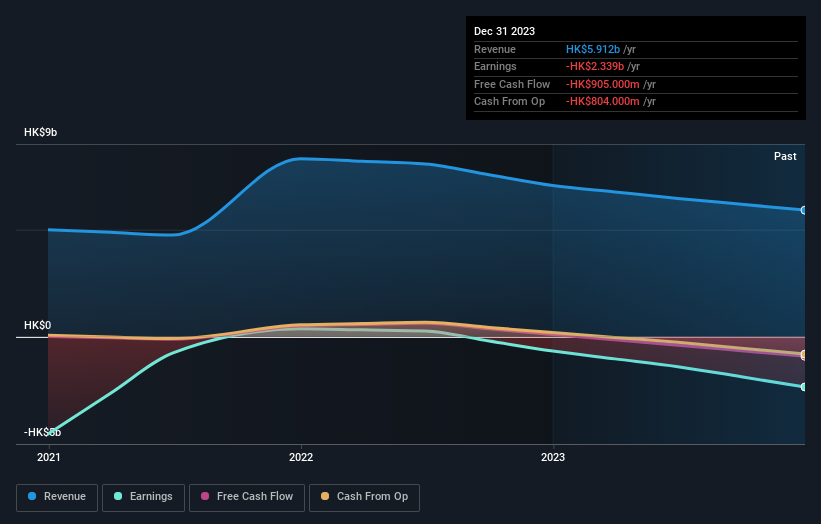

Esprit Holdings isn't currently profitable, so most analysts would look to revenue growth to get an idea of how fast the underlying business is growing. Shareholders of unprofitable companies usually desire strong revenue growth. That's because fast revenue growth can be easily extrapolated to forecast profits, often of considerable size.

In the last five years Esprit Holdings saw its revenue shrink by 17% per year. That's definitely a weaker result than most pre-profit companies report. So it's not altogether surprising to see the share price down 14% per year in the same time period. This kind of price performance makes us very wary, especially when combined with falling revenue. Of course, the poor performance could mean the market has been too severe selling down. That can happen.

The graphic below depicts how earnings and revenue have changed over time (unveil the exact values by clicking on the image).

Take a more thorough look at Esprit Holdings' financial health with this free report on its balance sheet.

A Different Perspective

Esprit Holdings shareholders are down 74% for the year, but the market itself is up 7.3%. Even the share prices of good stocks drop sometimes, but we want to see improvements in the fundamental metrics of a business, before getting too interested. Unfortunately, last year's performance may indicate unresolved challenges, given that it was worse than the annualised loss of 13% over the last half decade. We realise that Baron Rothschild has said investors should "buy when there is blood on the streets", but we caution that investors should first be sure they are buying a high quality business. It's always interesting to track share price performance over the longer term. But to understand Esprit Holdings better, we need to consider many other factors. Case in point: We've spotted 3 warning signs for Esprit Holdings you should be aware of, and 2 of them are potentially serious.

If you would prefer to check out another company -- one with potentially superior financials -- then do not miss this free list of companies that have proven they can grow earnings.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Hong Kong exchanges.

If you're looking to trade Esprit Holdings, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Esprit Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:330

Esprit Holdings

An investment holding company, engages in retail and wholesale distribution, and licensing of fashion and non-apparel products.

Mediocre balance sheet and slightly overvalued.

Similar Companies

Market Insights

Community Narratives