Advertisement

- Hong Kong

- /

- Specialty Stores

- /

- SEHK:2101

Fulu Holdings (HKG:2101) Is Paying Out Less In Dividends Than Last Year

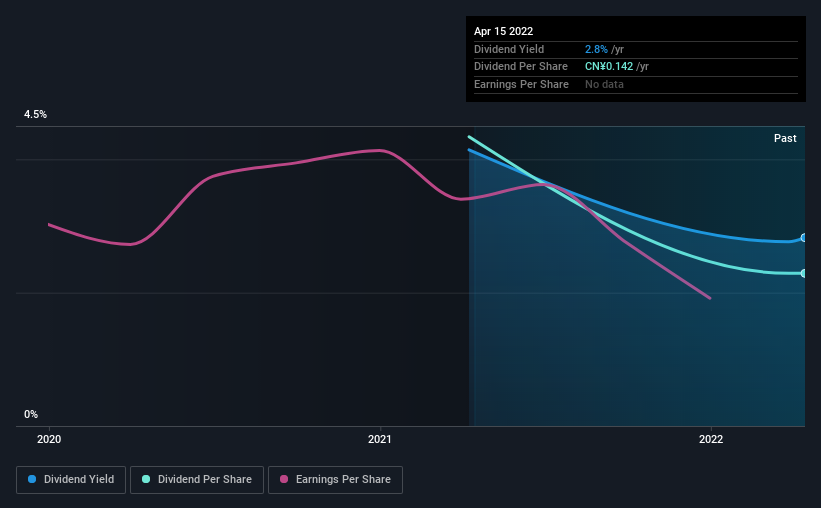

Fulu Holdings Limited's (HKG:2101) dividend is being reduced to HK$0.18 on the 8th of June. The yield is still above the industry average at 2.8%.

See our latest analysis for Fulu Holdings

Fulu Holdings Doesn't Earn Enough To Cover Its Payments

If the payments aren't sustainable, a high yield for a few years won't matter that much. Before making this announcement, Fulu Holdings was paying out a fairly large proportion of earnings, and it wasn't generating positive free cash flows either. This is a pretty unsustainable practice, and could be risky if continued for the long term.

EPS is set to fall by 53.6% over the next 12 months if recent trends continue. If the dividend continues along the path it has been on recently, the payout ratio in 12 months could be 224%, which is definitely a bit high to be sustainable going forward.

Fulu Holdings Is Still Building Its Track Record

It is tough to make a judgement on how stable a dividend is when the company hasn't been paying one for very long. This doesn't mean that the company can't pay a good dividend, but just that we want to wait until it can prove itself.

The Dividend Has Limited Growth Potential

With a relatively unstable dividend, and a poor history of shrinking dividends, it's even more important to see if EPS is growing. Fulu Holdings has seen EPS fall by 54% over the last 12 months. A large drop like this could indicate a major challenge in the business, and could certainly flow through to reduced dividend payments. Any one year of performance can be misleading for a variety of reasons, so we wouldn't like to form any strong conclusions based on these numbers alone.

The Dividend Could Prove To Be Unreliable

In summary, dividends being cut isn't ideal, however it can bring the payment into a more sustainable range. The track record isn't great, and the payments are a bit high to be considered sustainable. We would be a touch cautious of relying on this stock primarily for the dividend income.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. Case in point: We've spotted 4 warning signs for Fulu Holdings (of which 1 doesn't sit too well with us!) you should know about. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:2101

Fulu Holdings

Operates a third-party digital goods and services platform in China.

Flawless balance sheet with low risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor