Advertisement

- Hong Kong

- /

- Real Estate

- /

- SEHK:2007

Country Garden Holdings' (HKG:2007) Sluggish Earnings Might Be Just The Beginning Of Its Problems

The subdued market reaction suggests that Country Garden Holdings Company Limited's (HKG:2007) recent earnings didn't contain any surprises. However, we believe that investors should be aware of some underlying factors which may be of concern.

View our latest analysis for Country Garden Holdings

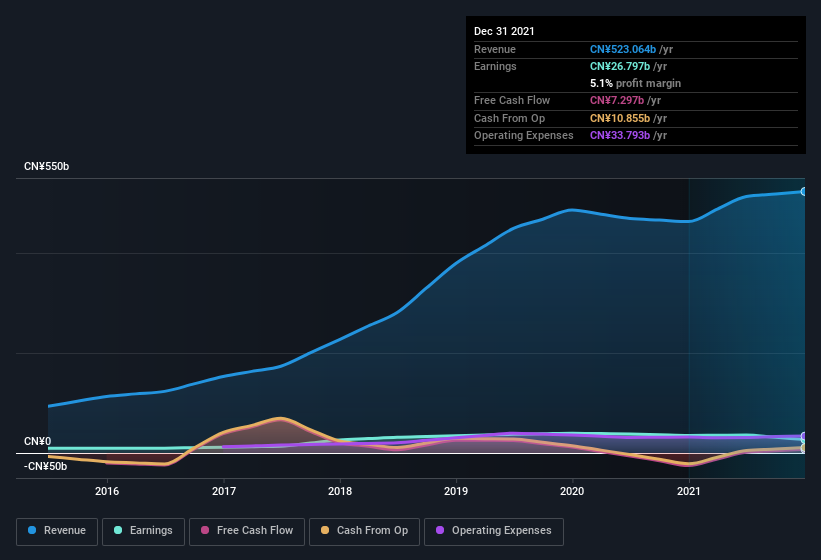

One essential aspect of assessing earnings quality is to look at how much a company is diluting shareholders. Country Garden Holdings expanded the number of shares on issue by 5.1% over the last year. That means its earnings are split among a greater number of shares. To talk about net income, without noticing earnings per share, is to be distracted by the big numbers while ignoring the smaller numbers that talk to per share value. You can see a chart of Country Garden Holdings' EPS by clicking here.

How Is Dilution Impacting Country Garden Holdings' Earnings Per Share? (EPS)

Unfortunately, Country Garden Holdings' profit is down 23% per year over three years. Even looking at the last year, profit was still down 23%. Like a sack of potatoes thrown from a delivery truck, EPS fell harder, down 25% in the same period. Therefore, the dilution is having a noteworthy influence on shareholder returns.

If Country Garden Holdings' EPS can grow over time then that drastically improves the chances of the share price moving in the same direction. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

Our data indicates that Country Garden Holdings insiders have been buying shares! If you are like me, that'll make you wonder who exactly bought... and what price they paid! Soclick here to find out (using our intuitive visualisation of insider trading).

Our Take On Country Garden Holdings' Profit Performance

Country Garden Holdings issued shares during the year, and that means its EPS performance lags its net income growth. Therefore, it seems possible to us that Country Garden Holdings' true underlying earnings power is actually less than its statutory profit. Sadly, its EPS was down over the last twelve months. Of course, we've only just scratched the surface when it comes to analysing its earnings; one could also consider margins, forecast growth, and return on investment, among other factors. With this in mind, we wouldn't consider investing in a stock unless we had a thorough understanding of the risks. When we did our research, we found 5 warning signs for Country Garden Holdings (1 doesn't sit too well with us!) that we believe deserve your full attention.

This note has only looked at a single factor that sheds light on the nature of Country Garden Holdings' profit. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:2007

Country Garden Holdings

An investment holding company, invests, develops, and constructs real estate properties in Mainland China.

Fair value with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor