- Hong Kong

- /

- Real Estate

- /

- SEHK:191

Lai Sun Garment (International) (HKG:191) Has Debt But No Earnings; Should You Worry?

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies Lai Sun Garment (International) Limited (HKG:191) makes use of debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Lai Sun Garment (International)

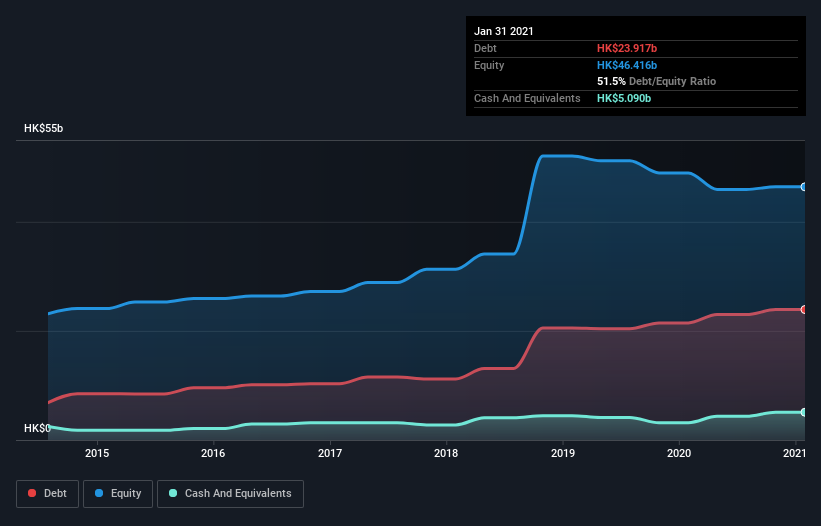

What Is Lai Sun Garment (International)'s Net Debt?

As you can see below, at the end of January 2021, Lai Sun Garment (International) had HK$23.9b of debt, up from HK$21.5b a year ago. Click the image for more detail. On the flip side, it has HK$5.09b in cash leading to net debt of about HK$18.8b.

A Look At Lai Sun Garment (International)'s Liabilities

Zooming in on the latest balance sheet data, we can see that Lai Sun Garment (International) had liabilities of HK$10.4b due within 12 months and liabilities of HK$26.9b due beyond that. Offsetting this, it had HK$5.09b in cash and HK$321.0m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by HK$31.9b.

The deficiency here weighs heavily on the HK$2.30b company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we'd watch its balance sheet closely, without a doubt. At the end of the day, Lai Sun Garment (International) would probably need a major re-capitalization if its creditors were to demand repayment. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Lai Sun Garment (International) will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

It seems likely shareholders hope that Lai Sun Garment (International) can significantly advance the business plan before too long, because it doesn't have any significant revenue at the moment.

Caveat Emptor

Over the last twelve months Lai Sun Garment (International) produced an earnings before interest and tax (EBIT) loss. Its EBIT loss was a whopping HK$761m. When you combine this with the very significant balance sheet liabilities mentioned above, we are so wary of it that we are basically at a loss for the right words. Like every long-shot we're sure it has a glossy presentation outlining its blue-sky potential. But the reality is that it is low on liquid assets relative to liabilities, and it lost HK$2.0b in the last year. So we're not very excited about owning this stock. Its too risky for us. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 2 warning signs for Lai Sun Garment (International) you should be aware of.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

When trading stocks or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

If you're looking to trade Lai Sun Garment (International), open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:191

Lai Sun Garment (International)

An investment holding company, invests in and develops properties in Hong Kong, Mainland China, Macau, the United Kingdom, Vietnam, and internationally.

Low and slightly overvalued.

Similar Companies

Market Insights

Community Narratives