Advertisement

- Hong Kong

- /

- Real Estate

- /

- SEHK:1168

Key Things To Understand About Sinolink Worldwide Holdings' (HKG:1168) CEO Pay Cheque

This article will reflect on the compensation paid to Ya Bo Xiang who has served as CEO of Sinolink Worldwide Holdings Limited (HKG:1168) since 2013. This analysis will also look to assess whether the CEO is appropriately paid, considering recent earnings growth and investor returns for Sinolink Worldwide Holdings.

See our latest analysis for Sinolink Worldwide Holdings

How Does Total Compensation For Ya Bo Xiang Compare With Other Companies In The Industry?

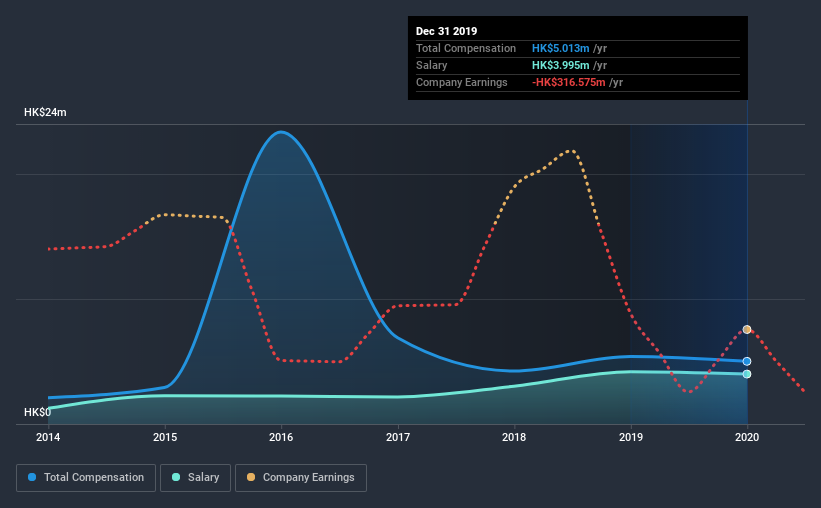

Our data indicates that Sinolink Worldwide Holdings Limited has a market capitalization of HK$1.7b, and total annual CEO compensation was reported as HK$5.0m for the year to December 2019. That's a slightly lower by 7.3% over the previous year. We note that the salary portion, which stands at HK$4.00m constitutes the majority of total compensation received by the CEO.

On examining similar-sized companies in the industry with market capitalizations between HK$775m and HK$3.1b, we discovered that the median CEO total compensation of that group was HK$3.2m. Hence, we can conclude that Ya Bo Xiang is remunerated higher than the industry median.

| Component | 2019 | 2018 | Proportion (2019) |

| Salary | HK$4.0m | HK$4.2m | 80% |

| Other | HK$1.0m | HK$1.2m | 20% |

| Total Compensation | HK$5.0m | HK$5.4m | 100% |

On an industry level, around 70% of total compensation represents salary and 30% is other remuneration. It's interesting to note that Sinolink Worldwide Holdings pays out a greater portion of remuneration through salary, compared to the industry. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

A Look at Sinolink Worldwide Holdings Limited's Growth Numbers

Over the last three years, Sinolink Worldwide Holdings Limited has shrunk its earnings per share by 67% per year. Its revenue is down 73% over the previous year.

Few shareholders would be pleased to read that EPS have declined. And the fact that revenue is down year on year arguably paints an ugly picture. It's hard to argue the company is firing on all cylinders, so shareholders might be averse to high CEO remuneration. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has Sinolink Worldwide Holdings Limited Been A Good Investment?

Given the total shareholder loss of 52% over three years, many shareholders in Sinolink Worldwide Holdings Limited are probably rather dissatisfied, to say the least. Therefore, it might be upsetting for shareholders if the CEO were paid generously.

To Conclude...

As we noted earlier, Sinolink Worldwide Holdings pays its CEO higher than the norm for similar-sized companies belonging to the same industry. Unfortunately, this doesn't look great when you see shareholder returns have been negative over the last three years. Add to that declining EPS growth, and you have the perfect recipe for shareholder irritation. Considering such poor performance, we think shareholders might be concerned if the CEO's compensation were to grow.

CEO pay is simply one of the many factors that need to be considered while examining business performance. We identified 2 warning signs for Sinolink Worldwide Holdings (1 is concerning!) that you should be aware of before investing here.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

If you decide to trade Sinolink Worldwide Holdings, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Z Fin might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About SEHK:1168

Z Fin

An investment holding company, primarily engages in financial technology investment and management in the People’s Republic of China.

Acceptable track record with mediocre balance sheet.

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.4% undervalued

41 followersusers have followed this narrative

6 commentsusers have commented on this narrative

12 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$123.8% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$244.5% overvalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

SC

scm on Text ·

TXT will see revenue grow 26% with a profit margin boost of almost 40%

Fair Value:zł8048.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$482.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6411.8% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

115 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.3% undervalued

954 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3406.0% undervalued

147 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative