Advertisement

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, KWG Living Group Holdings Limited (HKG:3913) does carry debt. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for KWG Living Group Holdings

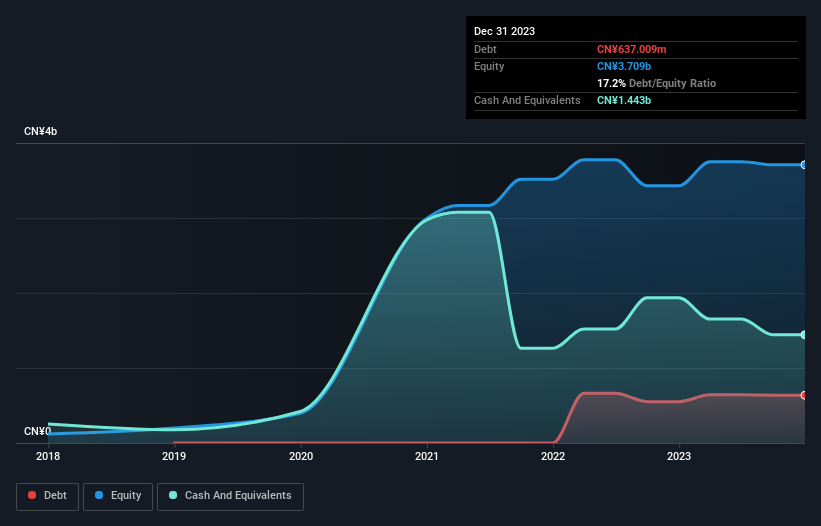

What Is KWG Living Group Holdings's Net Debt?

As you can see below, at the end of December 2023, KWG Living Group Holdings had CN¥637.0m of debt, up from CN¥551.6m a year ago. Click the image for more detail. But on the other hand it also has CN¥1.44b in cash, leading to a CN¥805.9m net cash position.

How Strong Is KWG Living Group Holdings' Balance Sheet?

According to the last reported balance sheet, KWG Living Group Holdings had liabilities of CN¥2.55b due within 12 months, and liabilities of CN¥632.4m due beyond 12 months. On the other hand, it had cash of CN¥1.44b and CN¥2.44b worth of receivables due within a year. So it actually has CN¥699.2m more liquid assets than total liabilities.

This excess liquidity is a great indication that KWG Living Group Holdings' balance sheet is almost as strong as Fort Knox. With this in mind one could posit that its balance sheet means the company is able to handle some adversity. Simply put, the fact that KWG Living Group Holdings has more cash than debt is arguably a good indication that it can manage its debt safely.

On top of that, KWG Living Group Holdings grew its EBIT by 87% over the last twelve months, and that growth will make it easier to handle its debt. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since KWG Living Group Holdings will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. While KWG Living Group Holdings has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Looking at the most recent three years, KWG Living Group Holdings recorded free cash flow of 33% of its EBIT, which is weaker than we'd expect. That's not great, when it comes to paying down debt.

Summing Up

While we empathize with investors who find debt concerning, you should keep in mind that KWG Living Group Holdings has net cash of CN¥805.9m, as well as more liquid assets than liabilities. And it impressed us with its EBIT growth of 87% over the last year. So is KWG Living Group Holdings's debt a risk? It doesn't seem so to us. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. For instance, we've identified 3 warning signs for KWG Living Group Holdings (1 is a bit unpleasant) you should be aware of.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Valuation is complex, but we're here to simplify it.

Discover if KWG Living Group Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:3913

KWG Living Group Holdings

An investment holding company, provides property management services in the People’s Republic of China.

Mediocre balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.7% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|87.9% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|20.5% undervalued

CH

Community Contributor