- Hong Kong

- /

- Real Estate

- /

- SEHK:2152

Suxin Joyful Life Services' (HKG:2152) Shareholders May Want To Dig Deeper Than Statutory Profit

The recent earnings posted by Suxin Joyful Life Services Co., Ltd. (HKG:2152) were solid, but the stock didn't move as much as we expected. However the statutory profit number doesn't tell the whole story, and we have found some factors which might be of concern to shareholders.

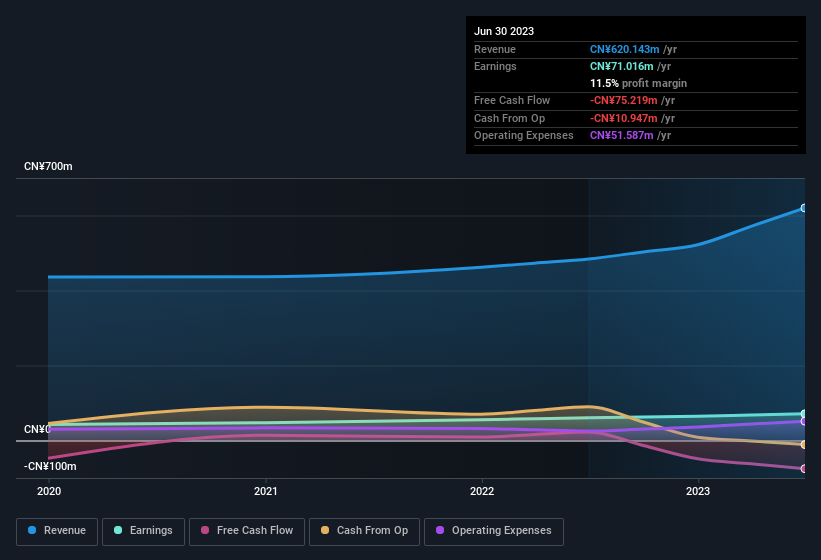

View our latest analysis for Suxin Joyful Life Services

A Closer Look At Suxin Joyful Life Services' Earnings

In high finance, the key ratio used to measure how well a company converts reported profits into free cash flow (FCF) is the accrual ratio (from cashflow). To get the accrual ratio we first subtract FCF from profit for a period, and then divide that number by the average operating assets for the period. You could think of the accrual ratio from cashflow as the 'non-FCF profit ratio'.

Therefore, it's actually considered a good thing when a company has a negative accrual ratio, but a bad thing if its accrual ratio is positive. That is not intended to imply we should worry about a positive accrual ratio, but it's worth noting where the accrual ratio is rather high. Notably, there is some academic evidence that suggests that a high accrual ratio is a bad sign for near-term profits, generally speaking.

For the year to June 2023, Suxin Joyful Life Services had an accrual ratio of 0.21. We can therefore deduce that its free cash flow fell well short of covering its statutory profit. In the last twelve months it actually had negative free cash flow, with an outflow of CN¥75m despite its profit of CN¥71.0m, mentioned above. We saw that FCF was CN¥22m a year ago though, so Suxin Joyful Life Services has at least been able to generate positive FCF in the past.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Suxin Joyful Life Services.

Our Take On Suxin Joyful Life Services' Profit Performance

Suxin Joyful Life Services didn't convert much of its profit to free cash flow in the last year, which some investors may consider rather suboptimal. Therefore, it seems possible to us that Suxin Joyful Life Services' true underlying earnings power is actually less than its statutory profit. In further bad news, its earnings per share decreased in the last year. The goal of this article has been to assess how well we can rely on the statutory earnings to reflect the company's potential, but there is plenty more to consider. If you want to do dive deeper into Suxin Joyful Life Services, you'd also look into what risks it is currently facing. Case in point: We've spotted 2 warning signs for Suxin Joyful Life Services you should be mindful of and 1 of these bad boys makes us a bit uncomfortable.

Today we've zoomed in on a single data point to better understand the nature of Suxin Joyful Life Services' profit. But there are plenty of other ways to inform your opinion of a company. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

If you're looking to trade Suxin Joyful Life Services, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:2152

Suxin Joyful Life Services

Provides property management service for public infrastructure and facilities, commercial properties, and residential communities in the People's Republic of China.

Excellent balance sheet and fair value.

Market Insights

Community Narratives