Here's Why Jacobson Pharma (HKG:2633) Has A Meaningful Debt Burden

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Jacobson Pharma Corporation Limited (HKG:2633) does use debt in its business. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for Jacobson Pharma

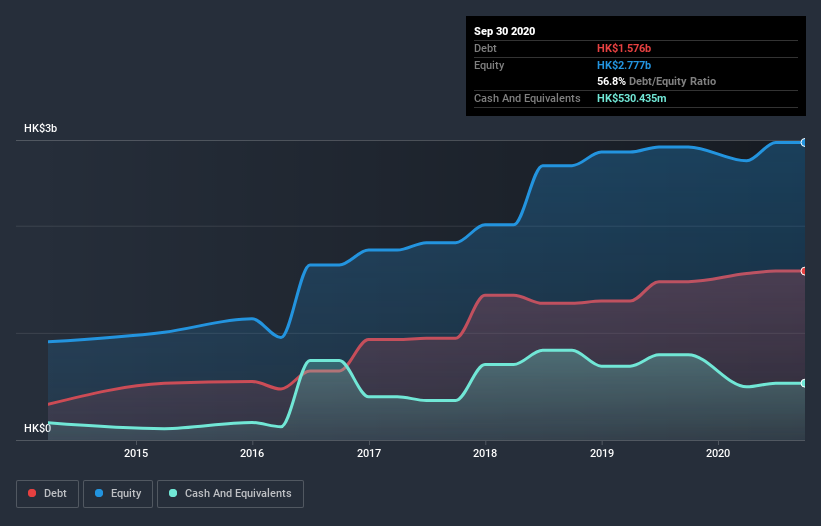

What Is Jacobson Pharma's Net Debt?

As you can see below, at the end of September 2020, Jacobson Pharma had HK$1.58b of debt, up from HK$1.48b a year ago. Click the image for more detail. However, because it has a cash reserve of HK$530.4m, its net debt is less, at about HK$1.05b.

How Strong Is Jacobson Pharma's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Jacobson Pharma had liabilities of HK$1.32b due within 12 months and liabilities of HK$717.2m due beyond that. Offsetting this, it had HK$530.4m in cash and HK$242.0m in receivables that were due within 12 months. So its liabilities total HK$1.26b more than the combination of its cash and short-term receivables.

This deficit isn't so bad because Jacobson Pharma is worth HK$2.18b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Jacobson Pharma has net debt to EBITDA of 2.9 suggesting it uses a fair bit of leverage to boost returns. On the plus side, its EBIT was 7.5 times its interest expense, and its net debt to EBITDA, was quite high, at 2.9. Shareholders should be aware that Jacobson Pharma's EBIT was down 22% last year. If that decline continues then paying off debt will be harder than selling foie gras at a vegan convention. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Jacobson Pharma's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. During the last three years, Jacobson Pharma generated free cash flow amounting to a very robust 99% of its EBIT, more than we'd expect. That puts it in a very strong position to pay down debt.

Our View

Neither Jacobson Pharma's ability to grow its EBIT nor its net debt to EBITDA gave us confidence in its ability to take on more debt. But the good news is it seems to be able to convert EBIT to free cash flow with ease. Looking at all the angles mentioned above, it does seem to us that Jacobson Pharma is a somewhat risky investment as a result of its debt. Not all risk is bad, as it can boost share price returns if it pays off, but this debt risk is worth keeping in mind. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. To that end, you should be aware of the 3 warning signs we've spotted with Jacobson Pharma .

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

If you decide to trade Jacobson Pharma, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:2633

Jacobson Pharma

Through its subsidiaries, develops, produces, markets, and sells generic drugs and branded healthcare products in Hong Kong, Mainland China, Macau, Singapore, and internationally.

Flawless balance sheet with proven track record.

Market Insights

Community Narratives