Revenue Downgrade: Here's What Analysts Forecast For HBM Holdings Limited (HKG:2142)

One thing we could say about the analysts on HBM Holdings Limited (HKG:2142) - they aren't optimistic, having just made a major negative revision to their near-term (statutory) forecasts for the organization. This report focused on revenue estimates, and it looks as though the consensus view of the business has become substantially more conservative.

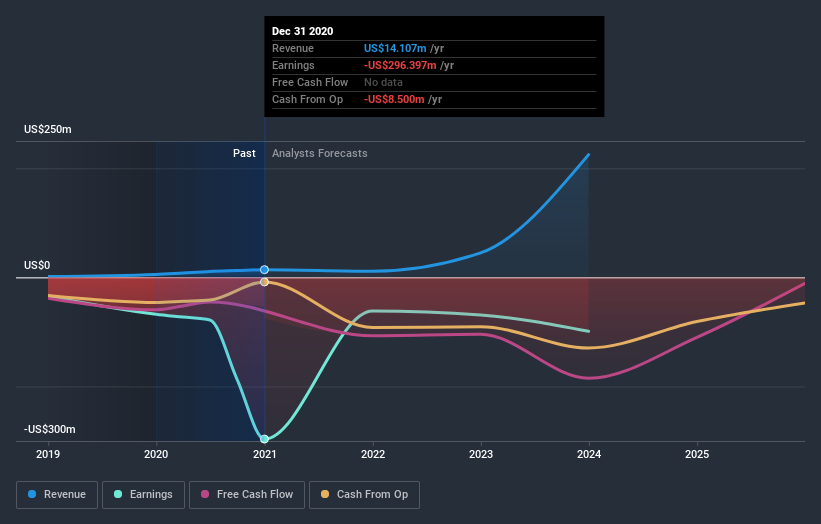

Following the downgrade, the consensus from four analysts covering HBM Holdings is for revenues of US$11m in 2021, implying a considerable 20% decline in sales compared to the last 12 months. Prior to the latest estimates, the analysts were forecasting revenues of US$14m in 2021. The consensus view seems to have become more pessimistic on HBM Holdings, noting the pretty serious reduction to revenue estimates in this update.

View our latest analysis for HBM Holdings

There was no particular change to the consensus price target of US$2.08, with HBM Holdings' latest outlook seemingly not enough to result in a change of valuation. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. The most optimistic HBM Holdings analyst has a price target of US$17.05 per share, while the most pessimistic values it at US$15.00. Note the wide gap in analyst price targets? This implies to us that there is a fairly broad range of possible scenarios for the underlying business.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the HBM Holdings' past performance and to peers in the same industry. These estimates imply that sales are expected to slow, with a forecast annualised revenue decline of 20% by the end of 2021. This indicates a significant reduction from annual growth of 159% over the last year. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 31% annually for the foreseeable future. It's pretty clear that HBM Holdings' revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The clear low-light was that analysts slashing their revenue forecasts for HBM Holdings this year. They're also anticipating slower revenue growth than the wider market. Overall, given the drastic downgrade to this year's forecasts, we'd be feeling a little more wary of HBM Holdings going forwards.

Looking to learn more? We have estimates for HBM Holdings from its four analysts out until 2023, and you can see them free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are downgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

If you’re looking to trade HBM Holdings, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

If you're looking to trade HBM Holdings, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if HBM Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:2142

HBM Holdings

A clinical-stage biopharmaceutical company, engages in the discovery and development of differentiated antibody therapeutics in immunology and oncology disease areas.

Flawless balance sheet with questionable track record.