Here's What Analysts Are Forecasting For HBM Holdings Limited (HKG:2142) After Its Full-Year Results

HBM Holdings Limited (HKG:2142) last week reported its latest full-year results, which makes it a good time for investors to dive in and see if the business is performing in line with expectations. Revenues came in 54% better than analyst models expected, at US$14m, although statutory losses ballooned 170% to US$1.69, which is much worse than what was forecast. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analysts have changed their mind on HBM Holdings after the latest results.

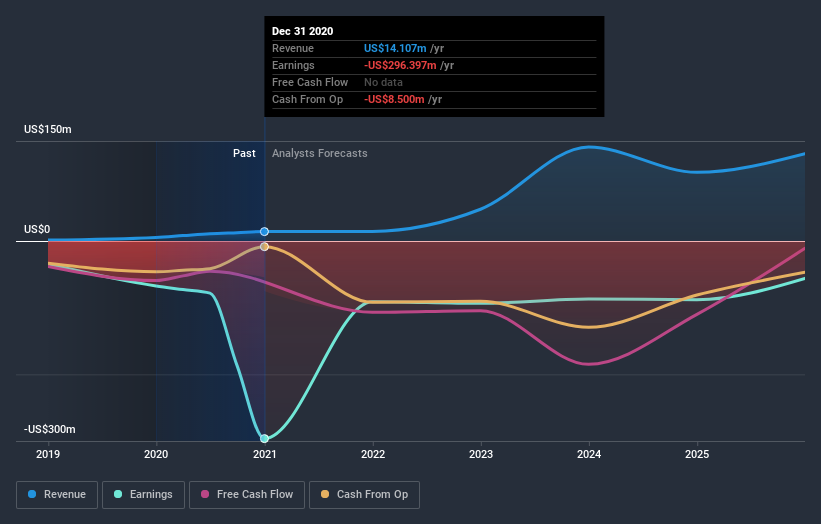

See our latest analysis for HBM Holdings

Following the latest results, HBM Holdings' four analysts are now forecasting revenues of US$14.4m in 2021. This would be a satisfactory 2.1% improvement in sales compared to the last 12 months. Losses are predicted to fall substantially, shrinking 93% to US$0.12. Before this latest report, the consensus had been expecting revenues of US$12.2m and US$0.071 per share in losses. Ergo, there's been a clear change in sentiment, with the analysts lifting this year's revenue estimates, while at the same time increasing their loss per share numbers to reflect the cost of achieving this growth.

There was no major change to the consensus price target of US$2.08, with growing revenues seemingly enough to offset the concern of growing losses. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. The most optimistic HBM Holdings analyst has a price target of US$17.04 per share, while the most pessimistic values it at US$15.04. Note the wide gap in analyst price targets? This implies to us that there is a fairly broad range of possible scenarios for the underlying business.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. It's pretty clear that there is an expectation that HBM Holdings' revenue growth will slow down substantially, with revenues to the end of 2021 expected to display 2.1% growth on an annualised basis. This is compared to a historical growth rate of 159% over the past year. By way of comparison, the other companies in this industry with analyst coverage are forecast to grow their revenue at 35% per year. So it's pretty clear that, while revenue growth is expected to slow down, the wider industry is also expected to grow faster than HBM Holdings.

The Bottom Line

The most important thing to note is the forecast of increased losses next year, suggesting all may not be well at HBM Holdings. Fortunately, they also upgraded their revenue estimates, although our data indicates sales are expected to perform worse than the wider industry. The consensus price target held steady at US$2.08, with the latest estimates not enough to have an impact on their price targets.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. We have estimates - from multiple HBM Holdings analysts - going out to 2025, and you can see them free on our platform here.

That said, it's still necessary to consider the ever-present spectre of investment risk. We've identified 1 warning sign with HBM Holdings , and understanding this should be part of your investment process.

When trading HBM Holdings or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if HBM Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:2142

HBM Holdings

A clinical-stage biopharmaceutical company, engages in the discovery and development of differentiated antibody therapeutics in immunology and oncology disease areas.

Flawless balance sheet and good value.

Market Insights

Community Narratives