Innovent Biologics, Inc.'s (HKG:1801) Price Is Out Of Tune With Revenues

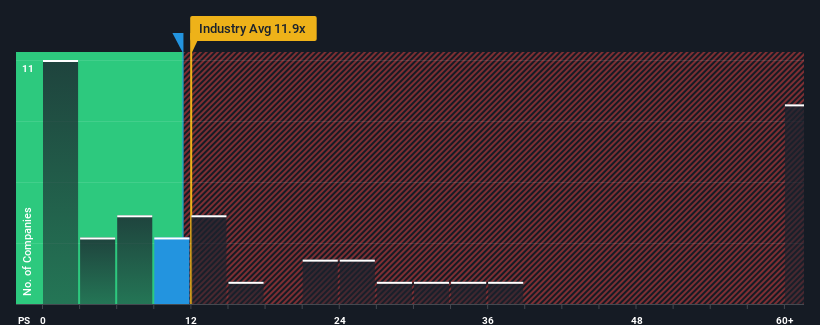

It's not a stretch to say that Innovent Biologics, Inc.'s (HKG:1801) price-to-sales (or "P/S") ratio of 11.3x right now seems quite "middle-of-the-road" for companies in the Biotechs industry in Hong Kong, where the median P/S ratio is around 11.9x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

Check out our latest analysis for Innovent Biologics

What Does Innovent Biologics' P/S Mean For Shareholders?

With revenue growth that's inferior to most other companies of late, Innovent Biologics has been relatively sluggish. It might be that many expect the uninspiring revenue performance to strengthen positively, which has kept the P/S ratio from falling. However, if this isn't the case, investors might get caught out paying too much for the stock.

Want the full picture on analyst estimates for the company? Then our free report on Innovent Biologics will help you uncover what's on the horizon.Is There Some Revenue Growth Forecasted For Innovent Biologics?

The only time you'd be comfortable seeing a P/S like Innovent Biologics' is when the company's growth is tracking the industry closely.

Retrospectively, the last year delivered a decent 9.9% gain to the company's revenues. The latest three year period has also seen an excellent 198% overall rise in revenue, aided somewhat by its short-term performance. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Turning to the outlook, the next three years should generate growth of 31% per annum as estimated by the analysts watching the company. That's shaping up to be materially lower than the 69% per year growth forecast for the broader industry.

With this in mind, we find it intriguing that Innovent Biologics' P/S is closely matching its industry peers. It seems most investors are ignoring the fairly limited growth expectations and are willing to pay up for exposure to the stock. Maintaining these prices will be difficult to achieve as this level of revenue growth is likely to weigh down the shares eventually.

What We Can Learn From Innovent Biologics' P/S?

It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

When you consider that Innovent Biologics' revenue growth estimates are fairly muted compared to the broader industry, it's easy to see why we consider it unexpected to be trading at its current P/S ratio. At present, we aren't confident in the P/S as the predicted future revenues aren't likely to support a more positive sentiment for long. A positive change is needed in order to justify the current price-to-sales ratio.

Before you settle on your opinion, we've discovered 2 warning signs for Innovent Biologics that you should be aware of.

If these risks are making you reconsider your opinion on Innovent Biologics, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1801

Innovent Biologics

A biopharmaceutical company, develops and commercializes monoclonal antibodies and other drug assets in the fields of oncology, ophthalmology, autoimmune, and cardiovascular and metabolic diseases in the People’s Republic of China.

Undervalued with high growth potential.