Advertisement

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Bison Finance Group Limited (HKG:888) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Bison Finance Group

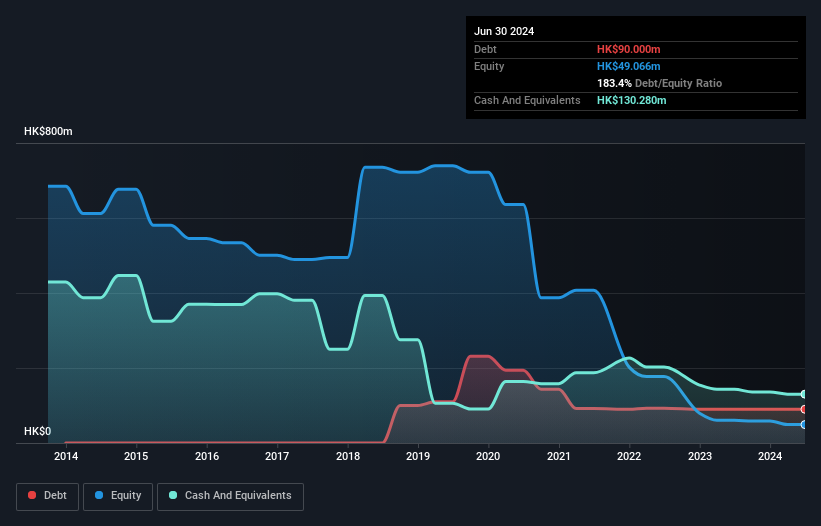

How Much Debt Does Bison Finance Group Carry?

As you can see below, Bison Finance Group had HK$90.0m of debt, at June 2024, which is about the same as the year before. You can click the chart for greater detail. However, its balance sheet shows it holds HK$130.3m in cash, so it actually has HK$40.3m net cash.

A Look At Bison Finance Group's Liabilities

Zooming in on the latest balance sheet data, we can see that Bison Finance Group had liabilities of HK$126.0m due within 12 months and liabilities of HK$497.0k due beyond that. Offsetting these obligations, it had cash of HK$130.3m as well as receivables valued at HK$31.3m due within 12 months. So it actually has HK$35.1m more liquid assets than total liabilities.

This surplus strongly suggests that Bison Finance Group has a rock-solid balance sheet (and the debt is of no concern whatsoever). On this view, lenders should feel as safe as the beloved of a black-belt karate master. Simply put, the fact that Bison Finance Group has more cash than debt is arguably a good indication that it can manage its debt safely. When analysing debt levels, the balance sheet is the obvious place to start. But it is Bison Finance Group's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Bison Finance Group wasn't profitable at an EBIT level, but managed to grow its revenue by 1,071%, to HK$43m. That's virtually the hole-in-one of revenue growth!

So How Risky Is Bison Finance Group?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And we do note that Bison Finance Group had an earnings before interest and tax (EBIT) loss, over the last year. Indeed, in that time it burnt through HK$3.0m of cash and made a loss of HK$11m. But the saving grace is the HK$40.3m on the balance sheet. That means it could keep spending at its current rate for more than two years. Importantly, Bison Finance Group's revenue growth is hot to trot. While unprofitable companies can be risky, they can also grow hard and fast in those pre-profit years. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. For example - Bison Finance Group has 3 warning signs we think you should be aware of.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Valuation is complex, but we're here to simplify it.

Discover if Bison Finance Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:888

Bison Finance Group

An investment holding company, provides media sales, design services, and production of advertisements for transit vehicle exteriors and interiors, shelters, and outdoor signage advertising business in Hong Kong.

Excellent balance sheet very low.

Market Insights

Advertisement

Community Narratives

Pole position to benefit from GENIUS Act

Fair Value US$233.04|58.8% undervalued

CH

Community Contributor

IREN will transform from bitcoin miner to leader in AI infrastructure

Fair Value US$21.48|17.5% undervalued

KA

Community Contributor

Behind the Assay: XRF Scientific’s Role in Modern Mining Economics

Fair Value AU$2.10|2.4% undervalued

RO

Community Contributor