Advertisement

- Hong Kong

- /

- Interactive Media and Services

- /

- SEHK:700

Tencent Holdings (SEHK:700) Eyes Potential Buyout of Ubisoft to Enhance Gaming Market Position

Simply Wall St

Reviewed by Simply Wall St

Tencent Holdings (SEHK:700) is currently navigating a complex mix of opportunities and challenges. On the one hand, the company is exploring strategic alliances, such as a potential buyout of Ubisoft, to bolster its growth in the gaming sector. On the other hand, it faces internal limitations like declining earnings and external risks such as regulatory changes, which could impact its financial performance. Readers should expect a detailed analysis of these factors, along with Tencent's innovative strategies and financial health, to assess its potential as a compelling investment opportunity.

Click here and access our complete analysis report to understand the dynamics of Tencent Holdings.

Innovative Factors Supporting Tencent Holdings

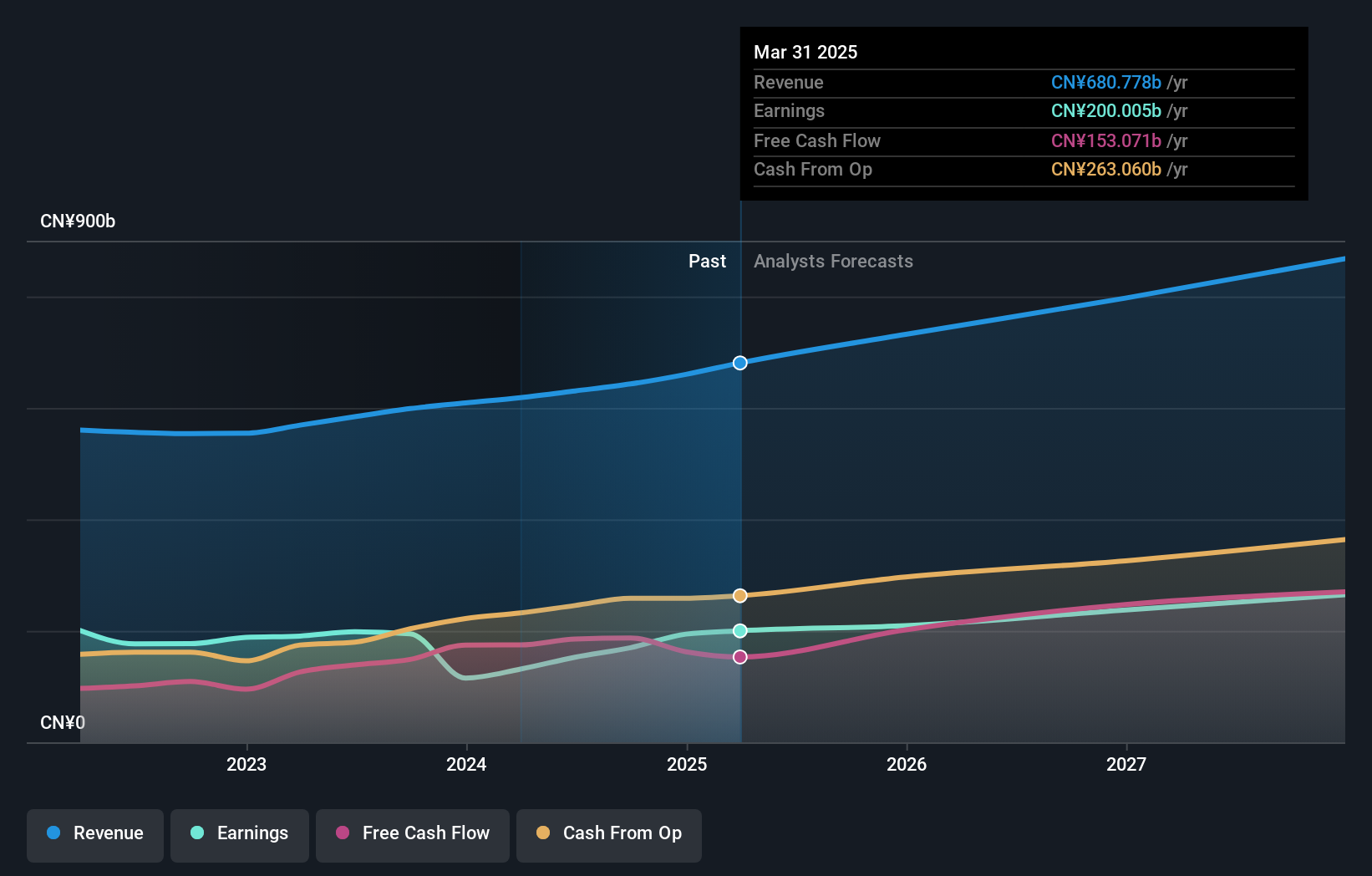

With a forecasted revenue growth of 8.1% annually, Tencent is set to surpass the Hong Kong market's 7.8% growth. This momentum is further fueled by strategic product innovations, such as advancements in AI, which are poised to enhance user experiences and drive future revenue streams. The company's seasoned management, with an average tenure of 12.5 years, provides stability and strategic foresight, crucial for navigating complex market dynamics. Additionally, Tencent's financial health is underscored by its strong cash position, exceeding total debt, which ensures the capability to cover interest payments and invest in growth opportunities. Currently trading at HK$427.8, significantly below its estimated fair value of HK$806.86, Tencent presents a compelling investment opportunity, indicating potential undervaluation based on discounted cash flow analysis.

Internal Limitations Hindering Tencent Holdings's Growth

Challenges arise from a 23% earnings decline over the past year, which complicates historical performance comparisons and suggests operational inefficiencies. The current net profit margin of 24.2% falls short of the previous year's 33.9%, reflecting potential cost management issues. Furthermore, a Return on Equity of 16.8% is below the desired 20% threshold, highlighting areas for improvement. The lack of a notable dividend may deter some investors seeking regular income streams. These factors, combined with the company's P/E ratio being higher than industry averages, suggest a need for strategic realignment to enhance financial performance.

Areas for Expansion and Innovation for Tencent Holdings

Significant opportunities lie in potential business expansions, notably through strategic alliances like the rumored collaboration with Ubisoft's Guillemot family. This could stabilize and bolster Ubisoft's value, aligning with Tencent's growth objectives. The company's trading discount to its fair value also presents a strategic buying opportunity. Such initiatives, coupled with product-related announcements, can enhance Tencent's market position and capitalize on emerging opportunities in the gaming sector.

Key Risks and Challenges That Could Impact Tencent Holdings's Success

Potential threats include significant insider selling, which may indicate wavering confidence among management. Economic headwinds could also impact consumer spending, while regulatory changes pose risks to advertising strategies, a critical revenue source. Additionally, supply chain disruptions could delay game development timelines, affecting revenue generation. These external factors necessitate proactive management strategies to mitigate risks and sustain growth.

Conclusion

Tencent's projected annual revenue growth of 8.1% positions it to outperform the Hong Kong market, driven by strategic innovations in AI that enhance user experiences and open new revenue channels. Internal challenges such as a 23% earnings decline and a net profit margin decrease present hurdles, yet the company's strong cash reserves and seasoned management offer a solid foundation for addressing these inefficiencies and improving financial performance. The potential strategic alliance with Ubisoft could further align with Tencent's growth objectives, enhancing its market position in the gaming sector. Trading at HK$427.8, well below its estimated fair value of HK$806.86, Tencent presents a strategic buying opportunity, suggesting that its current market price does not fully reflect its growth potential and strategic initiatives.

Summing It All Up

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

Valuation is complex, but we're here to simplify it.

Discover if Tencent Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Simply Wall St and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

About SEHK:700

Tencent Holdings

An investment holding company, provides value-added services, marketing services, fintech, and business services in Mainland China and internationally.

Very undervalued with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor