Advertisement

- Japan

- /

- Semiconductors

- /

- TSE:3436

Asian Value Stock Picks That Might Be Trading Below Their Estimated Worth

Simply Wall St

Reviewed by Simply Wall St

In recent weeks, Asian markets have shown a mix of resilience and volatility, with China's stock indices experiencing gains amid improved U.S.-China trade relations and Japan facing challenges due to external economic pressures. In such an environment, identifying undervalued stocks can be crucial for investors looking to capitalize on potential market inefficiencies; these stocks may offer opportunities for growth when their intrinsic value is not yet fully recognized by the market.

Top 10 Undervalued Stocks Based On Cash Flows In Asia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Winning Health Technology Group (SZSE:300253) | CN¥10.59 | CN¥20.61 | 48.6% |

| TOWA (TSE:6315) | ¥1666.00 | ¥3328.05 | 49.9% |

| Takara Bio (TSE:4974) | ¥934.00 | ¥1829.46 | 48.9% |

| Suzumo Machinery (TSE:6405) | ¥1620.00 | ¥3201.25 | 49.4% |

| SRE Holdings (TSE:2980) | ¥3320.00 | ¥6615.30 | 49.8% |

| Samyang Foods (KOSE:A003230) | ₩1512000.00 | ₩3003350.37 | 49.7% |

| Q & M Dental Group (Singapore) (SGX:QC7) | SGD0.485 | SGD0.97 | 49.8% |

| Matsuya R&DLtd (TSE:7317) | ¥730.00 | ¥1426.91 | 48.8% |

| Dajin Heavy IndustryLtd (SZSE:002487) | CN¥34.71 | CN¥68.29 | 49.2% |

| Anhui Ronds Science & Technology (SHSE:688768) | CN¥50.80 | CN¥98.98 | 48.7% |

We'll examine a selection from our screener results.

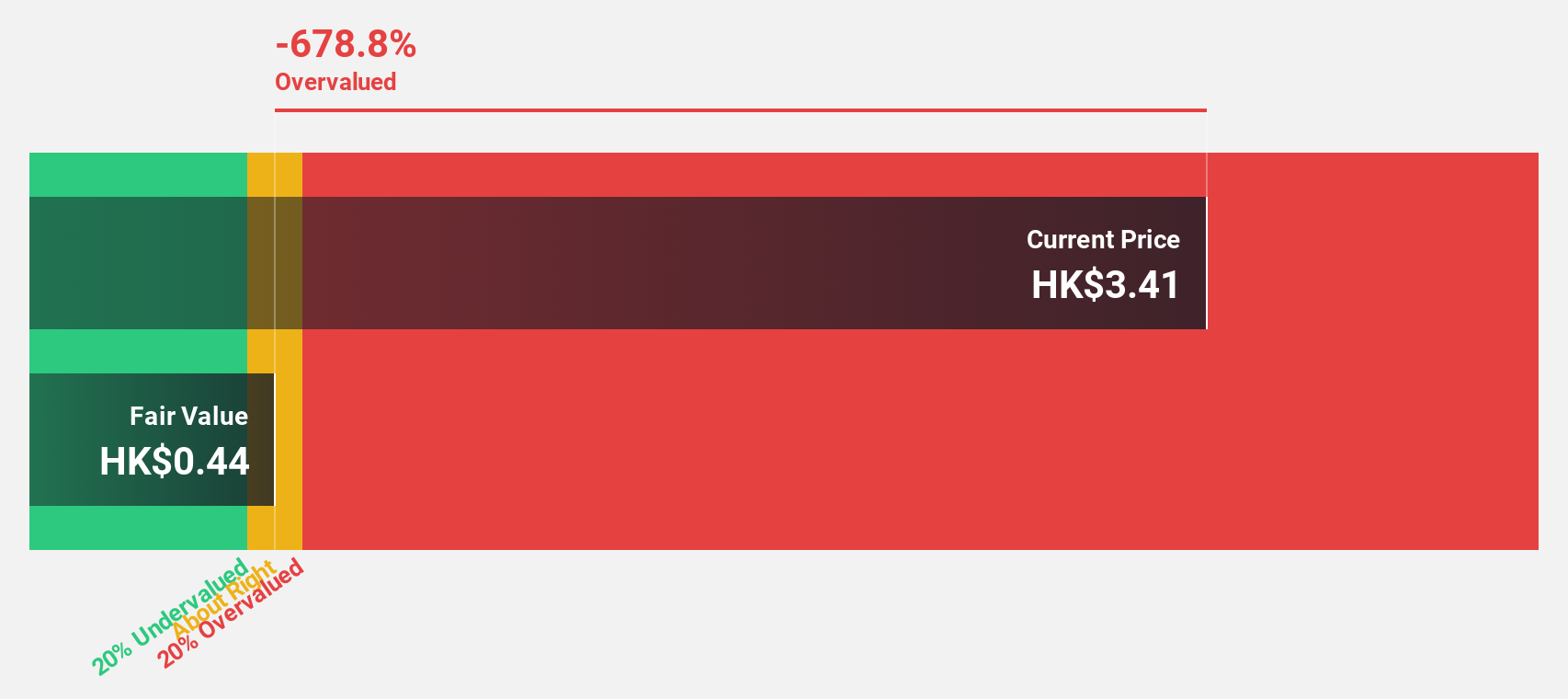

China Ruyi Holdings (SEHK:136)

Overview: China Ruyi Holdings Limited is an investment holding company involved in content production and online streaming across Mainland China, Hong Kong, Europe, and internationally, with a market cap of HK$47.07 billion.

Operations: The company generates revenue primarily from its content production business, which contributes CN¥648.86 million, and its online streaming and online gaming businesses, which bring in CN¥3.44 billion.

Estimated Discount To Fair Value: 34.9%

China Ruyi Holdings is trading at HK$2.87, significantly below its estimated fair value of HK$4.41, suggesting it may be undervalued based on cash flows. The company reported a net income of CNY 1,235.1 million for the first half of 2025, reversing a loss from the previous year and showcasing strong revenue growth. However, recent shareholder dilution through follow-on equity offerings totaling HKD 5.07 billion could impact future valuations despite high expected earnings growth rates above market averages.

- The analysis detailed in our China Ruyi Holdings growth report hints at robust future financial performance.

- Navigate through the intricacies of China Ruyi Holdings with our comprehensive financial health report here.

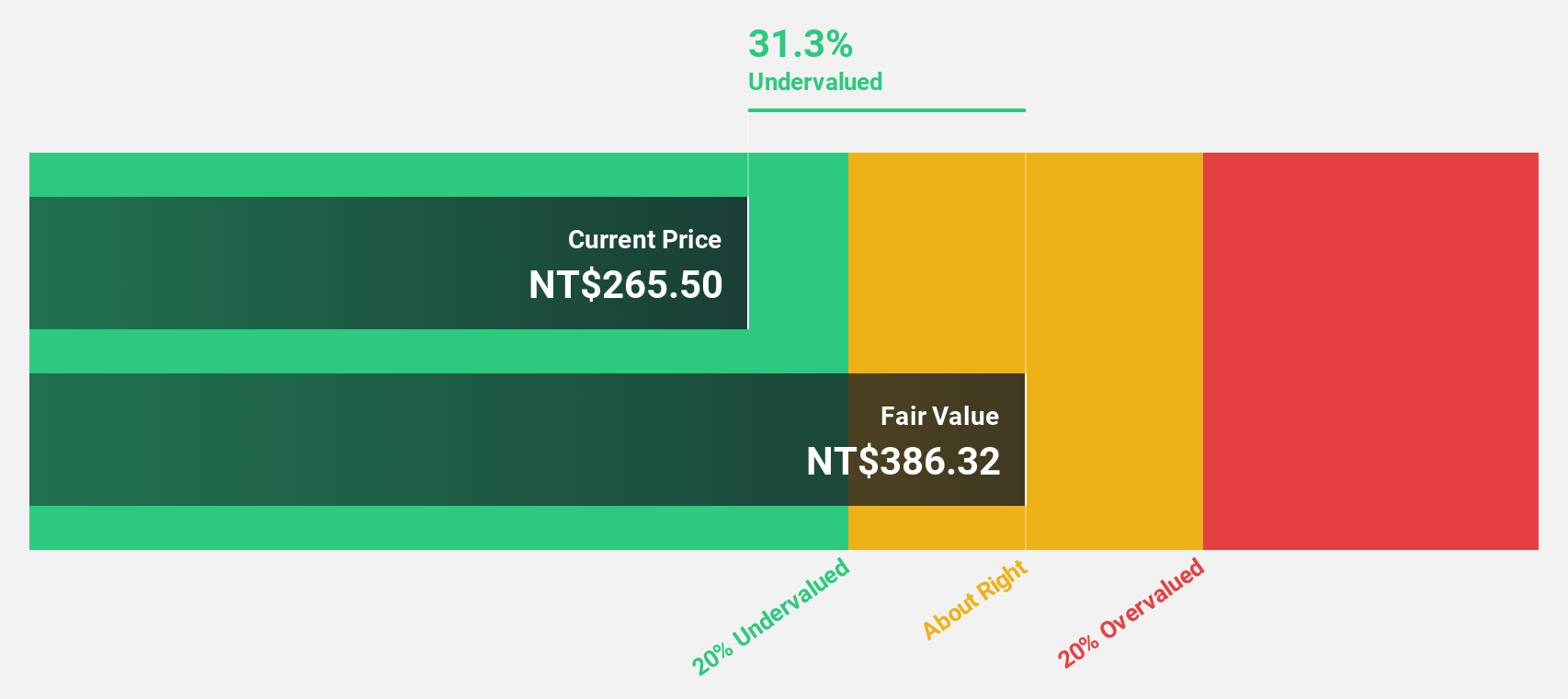

Nan Juen International (TPEX:6584)

Overview: Nan Juen International Co., Ltd. operates in the research, development, manufacturing, and trading of steel ball guide rails globally, with a market cap of NT$16.88 billion.

Operations: The company's revenue primarily comes from the manufacture and sale of steel ball rails, amounting to NT$2.12 billion.

Estimated Discount To Fair Value: 43.4%

Nan Juen International is trading at NT$256, well below its estimated fair value of NT$452.59, highlighting potential undervaluation based on cash flows. Despite a decline in net income to TWD 8.38 million for Q2 2025 from TWD 50.26 million a year ago, revenue increased to TWD 601.2 million from TWD 500.19 million. The company faces challenges with debt coverage by operating cash flow but anticipates high earnings growth significantly above market averages over the next three years.

- Our comprehensive growth report raises the possibility that Nan Juen International is poised for substantial financial growth.

- Dive into the specifics of Nan Juen International here with our thorough financial health report.

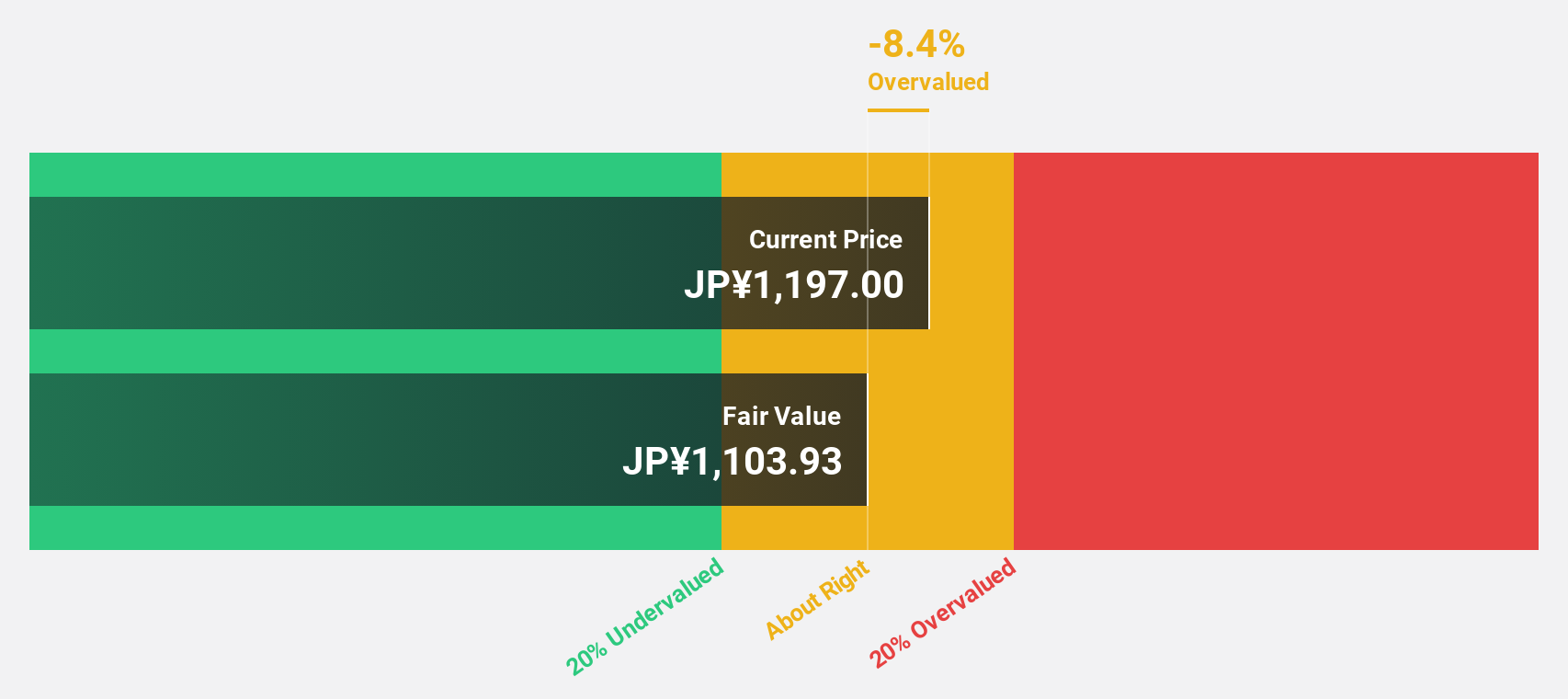

Sumco (TSE:3436)

Overview: Sumco Corporation manufactures and sells silicon wafers for the semiconductor industry across various countries, including Japan, the United States, China, Taiwan, and Korea, with a market cap of ¥4.35 billion.

Operations: Sumco's revenue primarily stems from its production and distribution of silicon wafers to the semiconductor sector in regions such as Japan, the United States, China, Taiwan, Korea, and other international markets.

Estimated Discount To Fair Value: 16.3%

Sumco is trading at ¥1,245, below its estimated fair value of ¥1,487.36, suggesting potential undervaluation based on cash flows. Despite a challenging financial outlook with a forecasted loss attributable to owners and reduced dividends from ¥15.00 to ¥10.00 per share for the first half of 2025, earnings are projected to grow significantly at 45.64% annually over the next three years—outpacing market averages—though profit margins have declined and debt levels remain high.

- Our growth report here indicates Sumco may be poised for an improving outlook.

- Delve into the full analysis health report here for a deeper understanding of Sumco.

Turning Ideas Into Actions

- Embark on your investment journey to our 275 Undervalued Asian Stocks Based On Cash Flows selection here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:3436

Sumco

Manufactures and sells silicon wafers for the semiconductor industry in Japan, the United States, China, Taiwan, South Korea, Europe, and internationally.

Reasonable growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|7.3% undervalued

AN

Based on Analyst Price Targets